With news of a possible bailout in Spain, bank bailouts are in the news again. I’m a big believer that banks are key to this recovery, but I’m skeptical that bailouts are actually helpful. That is, the best way to add a lack of focus to a bank is to make it even more beholden to ‘the public’. A restructuring or default would be preferred, because then the pain is allocated to investors, and so new owners can start over without any baggage from prior favors from politicians and just maximize profits (there’s a good reason to think this is what banks should be doing, but I understand many find that argument incomprehensible).

Anyway, I think one of my better ideas was in a post I wrote last year on Barrier Options and Business Cycles. The basic idea there was that if you looked at banks as not an option on a firm like in a Merton model, but as a barrier option on a firm, the vega actually becomes negative when the firm value is sufficiently low. This would mean banks go from taking on new projects to maximize equity value, to shedding projects.

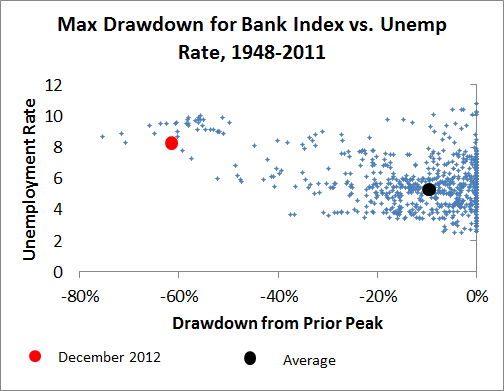

Bank stocks are still well off their historical highs, and I think this has some relevance to our rather unusually soft recovery.

Monthly bank index data from Ken French’s website.

Leave a Reply