Germany’s fiscal response to the crisis was timid compared with those of China and the US. This column uses business-cycle connectedness indices to show that Germany should follow in the footsteps of China and increase its domestic spending so that it will generate net positive connectedness to others. Germany was able to increase its exports thanks to the fact that countries like the US, China and Japan stimulated domestic spending significantly.

After the bankruptcy of Lehman Brothers in September 2008, leading governments around the world announced fiscal packages to provide stimulus to their respected economies. The Chinese government was one of the first. As early as November 2008, it announced a stimulus package that was planned to go into effect immediately in early 2009. The Chinese government also stood out in terms of the size of the package. Its stimulus package contained an additional fiscal spending of $586 billion over a two-year period (each year’s spending was equivalent to 6.9% of 2008 GDP). This spending package was larger than the combined stimulus packages of Japan and the EU, but smaller than the one announced by the US1.

China was able to increase government spending very quickly because its fiscal and external balances were in good shape before the crisis. In 2007, its general government budget was in surplus of 1.1% of GDP and its current-account surplus was equal to 10.1% of its GDP. Even though, both decreased slightly in 2008, China’s fiscal and external balances provided ample room for fiscal-policy manoeuvre in response to the crisis.

Among the 10 leading economies we analyse (including six industrial economies along with the BRICs), Germany was the only other country that had a relatively strong fiscal position before the crisis along with a sizeable current-account surplus. Germany’s budget deficit relative to its GDP was 1.1% in 2007 and 0.9% in 2008. Its current-account surplus relative to GDP was 7.5% in 2007, but declined slightly to 6.2% in 2008.

The similarity between the two countries’ current-account and fiscal balances, however, did not generate similar responses from the two countries to the financial crisis. While the Chinese government shifted gears towards an expansionary fiscal policy, the German government did very little to fight the recessionary fears. The fiscal stimulus packages announced by the German government in the last quarter of 2008 and the first quarter of 2009 amounted to a total of $103.3 billion to be spent over a two-year period. The German fiscal-stimulus spending per year was a mere 1.6% of its 2008 GDP and a small fraction of the Chinese package. Germany was ranked 23rd in a group of 43 countries in terms of the size of the fiscal-stimulus package relative to GDP, while China and the US were ranked the first and the third. It is also important to note that 68% of the German stimulus took the form of tax cuts rather than a direct increase in fiscal spending (Ortiz 2009).

Despite the fact it had implemented a smaller fiscal stimulus than comparable countries, Germany recovered quickly from the crisis to attain the pre-crisis growth rates. Following the 5.1% contraction in 2009, the economy grew by 3.6% and 3.1% in 2010 and 2011, respectively. A close look at the data reveals that Germany was able to grow faster in 2010 and 2011 thanks to the quick recovery in its exports. This happens during a period when the EZ crisis started in periphery countries.

While the rest of the Eurozone countries were not able to recover from the crisis, Germany was able to increase its exports thanks to the fact that countries like the US, China and Japan stimulated domestic spending significantly. In addition, following the sovereign-debt problems in the Eurozone’s periphery the euro depreciated against the dollar by 20% from October 2009 to July 20102.

The current-account balances of China and Germany followed similar paths in the period prior to the global financial crisis. From 2000 to 2007 they both increased significantly. After the crisis, however, the behaviour of the two differs substantially. China’s current-account surplus relative to GDP declined from the peak of 10.1% in 2007 to 2.8% in 2011. Germany’s surplus relative to GDP, on the other hand, declined from 7.4% in 2008 to 5.7% in 2011. In the meantime, Germany’s exports to China increased from $40 billion in 2007 to $71 billion in 2010, an increase of 76%. Its imports from China increased from $75 billion in 2007 to $101 billion in 2010, an increase of 35%.

Business-cycle connectedness

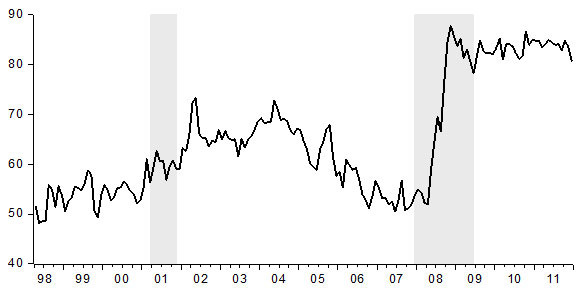

The total connectedness index in Figure 1, which measures how much of the shocks to industrial production in one country spill over to other countries, shows the extraordinary increase in business cycle connectedness of the leading economies in 2008 and after3. The index increased gradually from 50% in 1998 to 70% in 2002 and stayed around 70% until late 2004. The upward move in the index shows that the connectedness of the business cycles increased over the period. From 2005 through 2007 the connectedness index dropped gradually to 50%. Once the US economy went into recession the connectedness of the index shot up from 50% to 86% within two quarters in 2008. Since then the index stayed above 80%, indicating highly connected business cycles since 2008.

Figure 1. Total business cycle connectedness

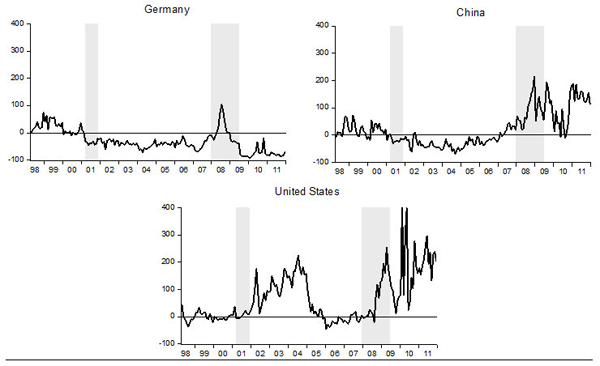

The directional connectedness plots in Figure 2 are quite revealing about the net connectedness of the US, Germany and China to others. Over 2002-2004 and 2008-2009, the net connectedness of the US to others increased above 200%. The high net directional connectedness of the US to others in 2002 through 2004 was due to the rapid recovery in US industrial production following the short recession of 2001. After a brief respite in the second half of 2009, the US started to generate significant connectedness in 2010 again, with its net connectedness reaching to more than 300%. This is when the US economy started to shift gear towards a slower growth performance. In the first half of 2010, the Eurozone leaders watched the Greek debt crisis burst and took any counteracting policy measure. The Eurozone’s mishandling of the Greek debt crisis led to a rapid depreciation of the euro, which led to dampening of the hopes of a quick recovery of the US economy through export growth, effectively making the QE2 mostly impotent.

Figure 2. Net directional connectedness to others

The most striking result in Figure 2 is the high level of net connectedness that China attained since the second half of 2008. The 1.7% contraction that the Chinese industrial production suffered in the second half of 2008 led to substantial connectedness to others. As a result, China’s net directional connectedness to others increased from -11% in August 2008 to 198% in November 2008.

The stimulus package was effective in raising Chinese industrial production. In the first half of 2009, the industrial production increased by 11.4% and in the second half by 5.7%. It was also effective in generating connectedness to other countries. Over the next twelve months, China’s net connectedness to others stayed high, fluctuating between 110 and 200%. Given that domestic demand in the US and the EU has stalled, the robust growth of Chinese domestic demand in 2009 was an important source of growth in other major economies of the world4. After fluctuating between 0% and 100% in 2010, the net business cycle connectedness of the Chinese economy jumped to 190% in January 2011 again and declined to around 120% in the second half of 2011.

Prior to the global financial crisis and the ensuing global recession, both China and Germany had both negative net spillovers. In the aftermath of the crisis, Germany continued to have negative net spillovers, while China’s net spillovers shut up in late 2008 and stayed high all the way to present. In the first half of 2008, Germany’s net spillovers temporarily moved to the positive territory, but went down to negative territory in the second half of 2008.

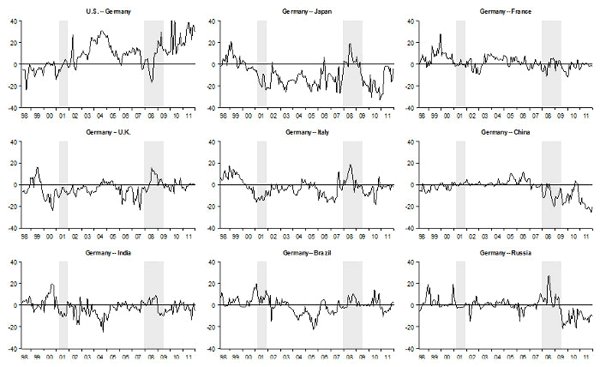

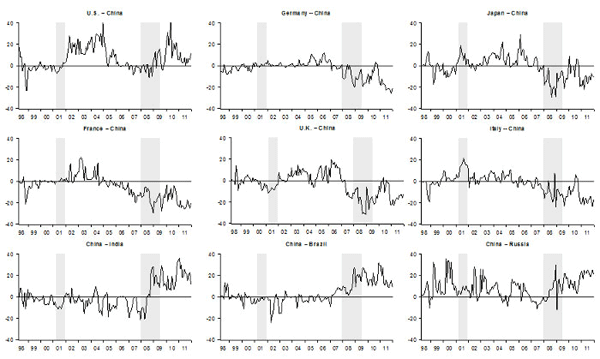

The fact that German net connectedness continued to stay in the negative territory shows that Germany’s industrial production has been influenced by business-cycle shocks to other countries. Had Germany followed the path China chose, it could have generated significant net-connectedness to its trade partners and countries in the Eurozone. However, as we can see from Figure 3, net business-cycle connectedness from Germany to other EU members, France, Italy and the UK, in the post-crisis era were either negative or close to zero. Instead, German industrial production was driven by the business-cycle connectedness from the US, Japan, China and Russia. In contrast, Chinese industrial production shocks led to net-connectedness to other major market economies (see Figure 4). It only receives net-connectedness from the US in the pre- and post-crisis periods.

Figure 3. Pairwise net directional connectedness – Germany

Figure 4. Pairwise net directional connectedness – China

The increasingly influential role of China

To summarise, directional connectedness measures show the increasingly influential role of China after the global financial crisis in generating business cycle connectedness to other economies. In contrast, Germany continues to be a net receiver of business cycle shocks from other countries. The stark difference between the net connectedness of the two countries with others is consistent with the differences in their fiscal-policy responses to the global financial crisis.

Our results, therefore, clearly show that while preaching austerity for its troubled Eurozone partners, Germany should follow in the footsteps of China and increase its domestic spending that will generate net positive connectedness to its major partner economies. Austerity in the troubled Eurozone members can make sense only if they are accompanied by expansionary fiscal policies in those countries whose fiscal accounts are in much better shape. Perhaps, what Eurozone needs is Growth-in-the-North combined with Austerity-in-the-South.

References

•Barabas, G. and Döhrn, R., 2009, “Fiscal Stimulus in Germany During the Current Recession, Assessment with the RWI-business cycle model,” Paper presented at the Project LINK meeting, October 26-28, 2009, Bangkok, Thailand.

•Diebold, F. X. and K. Yilmaz, 2011, “On the Network Topology of Variance Decompositions: Measuring the Connectedness of Financial Firms,” NBER Working Paper 17490, October.

•Morrison, W. M., 2009, “China and the Global Financial Crisis: Implications for the United States,” CRS Report for Congress, RS22984.

•Ortiz, I., 2009. “Fiscal Stimulus Plans: The Need for a Global New Deal”. IDEAs.

•Yilmaz, K., 2009a, “This time it is really different: Major industrialised economies are pulling each other into the abyss“, VoxEU.org, 28 March

•Yilmaz, K., 2009b, “International Business Cycle Spillovers,” TUSIAD-Koc University Economic Research Forum, Working Paper 0903, March.

________________

1In addition, numerous local governments also announced their own stimulus packages. As a conclusion, it is safe to conclude that the overall Chinese stimulus could be much higher than the official four trillion yuan ($586 billion) figure. (See Morrison 2009)

2In January 2009, IMF staff warned that Germany’s fiscal stimulus fell short of expectations, which they recommended to be around 2% of GDP in 2009 and 2010. According to some early estimates, the main German fiscal stimulus package favours the GDP in 2009 by ½ and in 2010 by ¼ percentage points. (See Barabas and Döhrn 2009.)

3Yilmaz (2009a) introduced the international business cycle connectedness analysis. For the methodology, see Yilmaz (2009b) and Diebold and Yilmaz (2011).

4There is widespread consensus among the practitioners about the effectiveness of the Chinese stimulus spending in late 2008 and in 2009: “The last time in late 2008 that economic peril was stalking the US and Europe, China marshaled the might of its state-directed economy and engineered a muscular rebound that led the subsequent global recovery.” (James Kynge, “Cracks in Beijing’s Financial Edifice,” Financial Times, October 9, 2011).

![]()

Leave a Reply