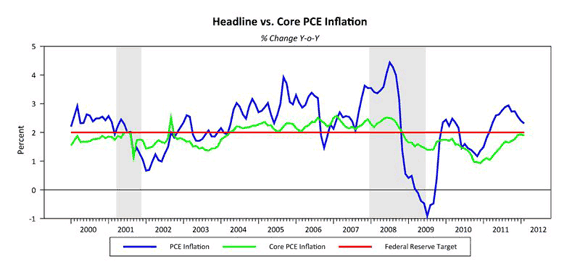

The Februrary Personal Income and Outlays report came out this morning, and with it a fresh read on the Federal Reserve’s preferred inflation measure, the PCE price index. On a year-over-year basis, headline inflation is trending down to the 2% target, while core is settling in just below that target.

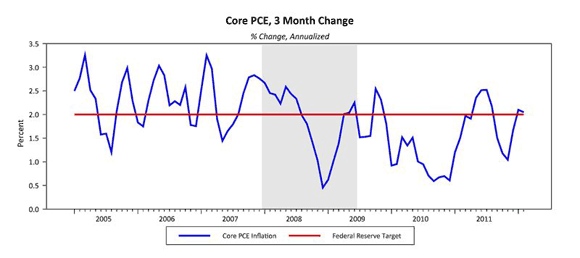

As a reminder, the Fed targets headline over the longer run, but watches core as a signal to where headline is headed. Headline is trending down to core, as expected. The Fed was right to dismiss last year’s energy-induced headline increase as a temporary phenomenon. Is there any near term trends to be concerned about? The three-month core trend edged down a notch to just above 2%:

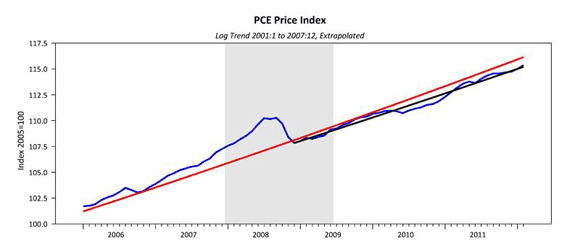

Still less than the rise experienced in the first part of 2011. What about the path of prices? Still tracking along a trend below that of prior to the recession:

Opportunistic disinflation at work.

Bottom Line: Inflation remains contained – by itself, price trends provide no reason for the Fed to turn hawkish. Moreover, there is nothing here to stop Federal Reserve Chairman Ben Bernanke from easing policy should the US receovery falter.

Leave a Reply