Morgan Stanley, the uber Bull of Apple (NASDAQ:AAPL) is raising their Bull case PT to $960 this morning:

They see further upside to AAPL shares on meaningful EPS revisions as their new CY13 base / bull case EPS estimates of $60 / $80 are 24% / 65% above consensus. Firm new official $720 PT (prior $515) conservatively assumes no multiple expansion. AAPL has been added to Morgan Stanley’s Best Ideas list.

Investors still underestimate the potential earnings upside at Apple. Apple trades at 9.5x firm’s base case and 7.1x their bull case CY13e EPS and Morgan Stanley’s What’s in the Price analyzer suggests AAPL shares discount just 2% growth longer-term. They see several potential EPS upside drivers based on their proprietary work which they incorporate in their new bull case: 1) enterprise tablet adoption combined with demand upside from lower priced iPad; 2) strong upgrade cycle to LTE (Long Term Evolution) capable iPhone starting later this year; 3) emerging market iPhone (plus iPad, Mac) growth driven by new carriers. China Mobile alone could add more incremental iPhone shipments than the Street models in total for CY13; 4) margin upside from lower ASP declines, increased mix of mobile devices and recent capital investments.

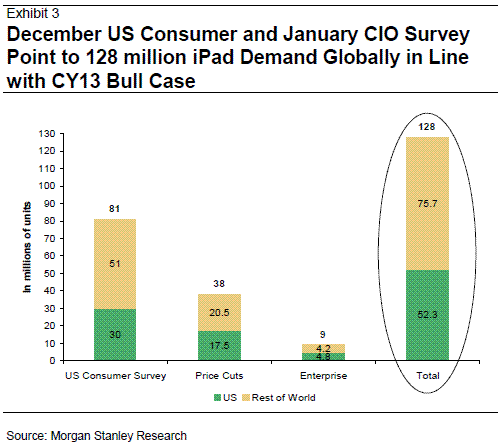

1) Enterprise tablet adoption combined with demand upside from lower-priced iPad. The pace of enterprise tablet adoption is exceeding expectations, according to Morgan Stanely’s January 2012 CIO survey. Fifty-six percent of US companies already purchase tablets for corporate use, compared to a 51% expected penetration a year ago. Assuming Apple maintains its 80% share of the enterprise tablet market, iPad purchases by enterprises could account for 9 million units and $5 billion in iPad revenue in CY12. This is in addition to consumer purchases of iPads, some of which will also be used in the enterprise.

2) iPhone estimates don’t credit Apple for the potential share gains when it launches an LTE-capable device in 2H12. MSCO supply chain checks suggest Apple’s sixth generation iPhone could include several changes that, in their view, will increase the upgrade rate relative to past product cycles. In particular, iPhone 5 is likely to include a higher-resolution and potentially thinner screen, new casing material, faster processor, and quad-mode baseband chip that works on multiple flavors of 3G and LTE. Their December US survey indicated that 62% of iPhone owners planned to upgrade to the new version, iPhone 4S. Assuming a similar upgrade rate for the LTE iPhone due out later this year, this implies 148M and 160M upgrade purchases in their base and bull case. The remaining 38M and 86M shipments would come from new users, roughly split between emerging markets and mature markets. For perspective, the same math implies Apple added roughly 48M new users in CY11.

3) China and other emerging markets, like Brazil, remain huge untapped markets. The emerging markets remain a huge opportunity for upside long term due to attractive demographics. Smartphone penetration is highest among cell phone users 25 to 34 years old, according to Nielsen. The emerging markets have nearly 14x the population in this age range than Western Europe and North America.

Despite being well above investor expectations Morgan Stanley views their CY13e bull case $80 EPS / $960 valuation as reasonable given: 1) Apple’s CapEx forecast predictsva similar revenue trajectory; 2) they don’t include new product categories like TV and low-price iPhone; 3) Firm’s CY13 bull case iPad forecast of 129M units is in-line with what our AlphaWise surveys imply for CY12; 4) iPhone growth ex-China only assumes an average upgrade rate and a new subscriber number similar to CY11; 5) they assume no multiple expansion despite a possible dividend.

Notablecalls: So there you go, we’re almost at $1000 price target. Good thing it’s coming from MSCO and not some boutique trying to make a name for themselves.

Needless to say, expect new highs for the stock today. A sentiment call.

I think it’s pretty obvious to everyone that with the high unemployment/underemployment environment that we’re in right now, it’s amazing Apple is doing so well. Holding the stock for a few years when unemployment returns to normal levels is a good idea. Can you imagine the revenue/profits they’ll make when we are back to full employment and the economy is firing on all four cylinders?