The Federal Reserve still would like to do more, but not right now.

The Federal Open Market Committee yesterday released the following economic assessment:

The Committee continues to expect a moderate pace of economic growth over coming quarters and consequently anticipates that the unemployment rate will decline only gradually toward levels that the Committee judges to be consistent with its dual mandate. Strains in global financial markets continue to pose significant downside risks to the economic outlook. The Committee also anticipates that inflation will settle, over coming quarters, at levels at or below those consistent with the Committee’s dual mandate.

In almost identical language that it used November 2, the Fed is saying that it expects unemployment will remain higher than it wants, inflation will likely be lower than it wants, and that it has significant concerns about where events in Europe might lead. In normal times, that trio would surely signal that policy would become more expansionary.

But the Fed opted instead to keep things more or less on hold, again using almost identical language as in its previous statement:

the Committee decided today to continue its program to extend the average maturity of its holdings of securities as announced in September. The Committee is maintaining its existing policies of reinvesting principal payments from its holdings of agency debt and agency mortgage-backed securities in agency mortgage-backed securities and of rolling over maturing Treasury securities at auction.

Why nothing more? I think one issue may be that, while the Fed says it has been anticipating that future inflation will come in at a rate below its target, it is much harder to make the case that the realized headline inflation rates over the last 12 months have been substantially too low.

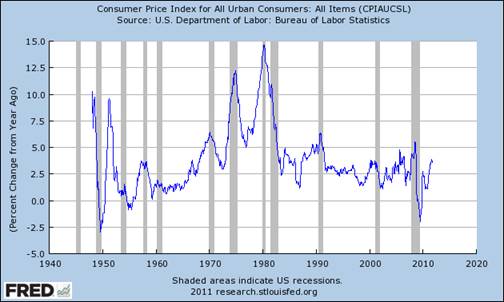

Year-over-year percent change in CPI. Source: FRED

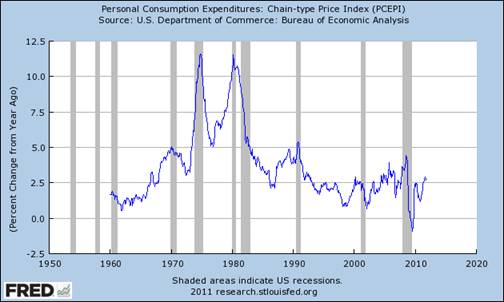

Year-over-year percent change in PCE deflator. Source: FRED

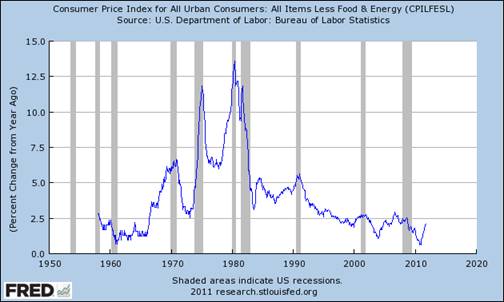

Excluding food and energy, the rate of increase of the CPI has been around 2%. But this measure has been heading up, not down. Although the Fed may regard core CPI or core PCE as a better measure, it is harder to persuade the public that this is the number that should matter, particularly given concerns that food and energy could be among the key prices that would adjust if the Fed were to adopt further easing.

Year-over-year percent change in CPI excluding food and energy. Source: FRED

My advice for the Fed is to be clear in their minds, and clear in communicating to the public as well, what kind of problems monetary policy can solve and what kind of problems it can’t. In the former category, the Fed can and should prevent a financial panic, and it can and should keep inflation from falling below 2%. I would use the latter as a standard for deciding on any aggressive new quantitative easing initiatives.

But it’s hard to bring out the bazookas to take aim at deflation when the CPI registered 3.6% inflation over the last 12 months and the PCE deflator 2.7%.

Fisher, Plosser, and Kocherlakota– the three members most likely to oppose further Fed easing– are all rotating off of the FOMC for 2012. And the FOMC statement suggests that the Fed is still expecting those inflation numbers to drop. When and if they do, perhaps then the Fed will act. And of course the Fed stands ready to respond to a potential European financial crisis. But for the time being, it appears that not much has changed.

Leave a Reply