At the end of last year I made predictions (a total of 44) of what might come. So far I’ve got (at least) one right and other dead wrong. I’m worried about the one I’m wrong on.

Right

-Volatility is going up across the board. If you have the stomach for the swings that are coming across all markets there is a ton of money to be made; balls and timing are all that are necessary. The markets will create dozens of opportunities to make and lose.

Wrong

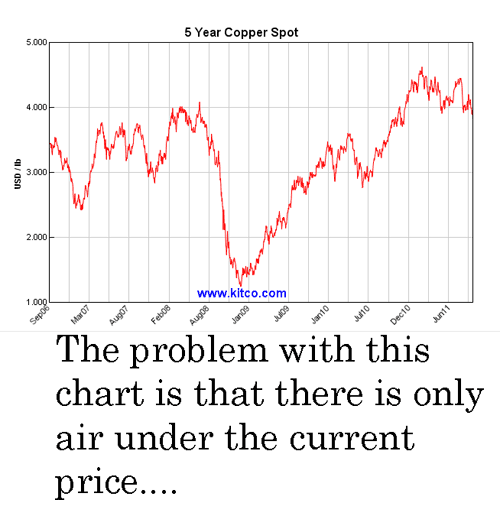

-Copper will continue to rise. This metal will benefit as the poor man’s gold. Why buy an ounce of something for $1,600 when you can have a whole pound of something else for only $5? The logic is compelling only because there is no logic.

Copper is looking very stinky on the charts.

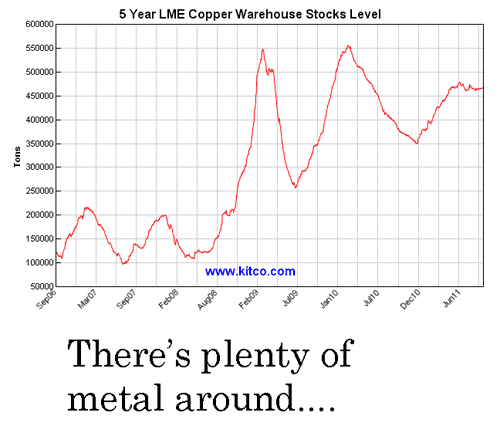

Does it matter if copper breaks down? In the normal course of things I would say no. The demand side is slipping on a global basis; there’s plenty of metal around, so lower prices are not much of a surprise. But there is a wild card on copper this time around. I’m wondering if the crap out in copper is going to bring indigestion to China.

Entities in China have been using copper warehouse stocks as collateral for financing all manner of things for the past two years (L/C backed financing). The estimates for how much has been done of this are not clear. The range is from $7-10 billion.

That China Inc. has been borrowing using copper collateralized debt is an old story. The following links discuss this in depth.

- FTAlphaville – Why the Chinese copper financing scheme is a big deal

- WSJ – China’s Doctored Copper Demand

- FTAlphaville – Simply amazing commodity collateral shenanigans in China

- Credit Writedowns – The debt-financed investments of Chinese state-owned enterprises

- The Telegraph – A ‘Copper Standard’ for the world’s currency system?

- Business Insider – Credit-Mad Chinese Companies Are Hoarding Copper In A Ponzi Scheme For New Loans

- Zero Hedge – Copper: More Than China’s Property Market

This FTA story ended with this observation:

But, if prices fall seriously beyond the face value of their loan exposure — the risk of LCs being thrown into sudden and immediate ‘non-payment danger’ rises exponentially.

I think we have to be pretty close to where the rubber meets this road. One thing for sure, those lenders (and borrowers) who have relied on this scheme in the past will find the door closed for new financings today. There is a growing risk that some of the underlying debt will not be money good, and the copper inventory will have to get sold.

Should this get rolling we will see it in the print. The (so far) orderly retreat in copper will accelerate. Don’t read this and conclude that I’m recommending a short in copper. What I’m suggesting is that one watch the copper price as a leading indicator of a funding problem in China. One breakdown may lead to another.

China Inc. could solve the problem in an hour or two. They could offer to buy all the excess metal at $4.50 a pound. But that would be a bailout of state owned lenders. That would be a slippery slope that would lead to more bailouts of an already over levered system. Either way, the availability of credit would dry up under these conditions.

What the world economy (and the equity markets) doesn’t want to hear about right now is a hiccup in China that ratchets growth down another notch. We might just get that.

Leave a Reply