There is a ray of hope in the otherwise dismal housing market. This morning, REIS Inc., a real estate data firm, announced that the apartment vacancy rate had fallen to 6.2% in the first quarter of 2011, down from 6.6% in the fourth quarter and 8.0% in the first quarter of 2010.

That is the lowest apartment vacancy rate since the second quarter of 2008. Over 44,000 net apartments found tenants in the quarter, almost double the number of a year ago.

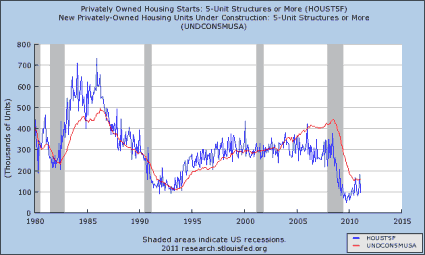

Meanwhile, there were only 6,000 new units coming on line in the quarter, the lowest number since REIS started keeping track. The number of new apartments being started has been very low over the last two years. Recently they seemed to have picked up (blue line), but have been extremely erratic, as is shown in the graph below.

It takes about a year for an apartment project to move from the start of digging until people start to move in. The pipeline of projects under construction is very empty (red line). This means it is likely that the vacancy rate will continue to fall.

That is very good news for the Apartment REITs like Apartment Investment (AIV), Avalon Bay (AVB) and Equity Residential (EQR). An apartment unit is mostly a fixed cost, and so one sitting empty is a big drag on the profitability of an apartment complex.

Not only that, but rents are starting to creep up. The average effective rent rose in 75 of the 82 markets that REIS tracks. Nationwide the average rose to $991 per month from $986 in the fourth quarter and $967 a year ago. That’s not exactly a return to 1970’s style inflation — the year-over-year increase is just 2.5%, and the annualized increase in the first quarter is just 2.0%. Some of that has come in the form of lower concessions, such as a month of free rent when you sign a lease.

Average stated rents rose to $1,047 from $1,043 in the fourth quarter and $1,027 a year ago, or annualized increases of 1.5% for the quarter and 1.9% year over year. Still, housing has a very large weighting in the CPI, particularly Owner’s Equivalent Rent (OER). Regular rent makes up 5.93% while OER is 24.91%.

Over time, OER tracks regular rent pretty closely. The rents, with a combined weighting of 30.84% of the total CPI, and over 40% of the core CPI have been a major factor in keeping the overall rate of inflation down.

Excess Housing Being Absorbed

It looks like this is the first stage of the absorption of the excess housing supply. That is desperately needed if the housing market is ever going to return to health. If there is a large inventory of existing homes sitting empty, then it makes very little sense to be building a lot of new homes.

Each new home built generates a huge amount of economic activity. Because housing is such a long-lived and big-ticket asset, it is normally exquisitely sensitive to interest rates. As such, it has historically reacted quickly when interest rates have fallen into a recession, and as it picked up, it has helped pull the economy out of recessions.

This time around, though, the housing market was so messed up going in to the recession that even mortgages rates below 5%, a generational low, have not stimulated the housing market. Indeed, things have only gotten worse.

The ten lowest months in history for new home sales have all been in the last ten month, including the record low of just 250,000 (seasonally adjusted annual rate) in February, a drop of 16.9% from January and 28.0% from a year earlier. Housing prices have also been falling again, with the Case-Schiller composite index down 3.0% year over year in January.

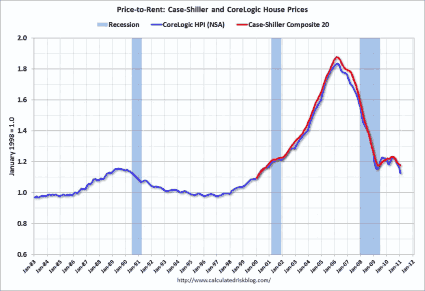

The combination of slowly rising rents and falling home prices means that the price-to-rent ratio, the history of which is shown below (from this source), is coming down. It was the huge surge in this ratio that was the most obvious sign that we had that a bubble was occurring (the ratio of median income to median home price followed a very similar path and was also an important clue that we were in a bubble).

It should be pointed out that the decline in the apartment vacancy rate is also a reflection of a lot of economic pain out there. Since in peaked in 2004, the home ownership rate has fallen from 69.2% to 66.5%. Each point represents about 1.1 million families, so that means that there are about 3 million fewer homeowners today than there were back then.

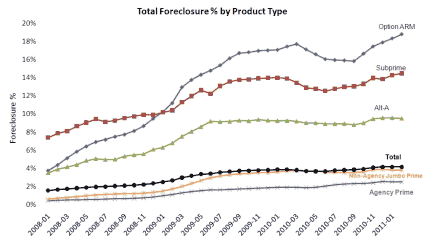

For the most part, those people have lost their homes to foreclosure. The foreclosure rate is at a record high 4.63%. The next graph (from this source) breaks down the foreclosure rates over time by type of mortgage.

It is worth noting that for all the flack Fannie and Freddie have gotten over the housing and mortgage mess, the foreclosure rates for their mortgages are — and have been consistently — below the foreclosure rates for the private-label mortgages which tended to specialize in the sub-prime and more exotic option ARM products. However, even the prime mortgages that they backed have seen a consistently rising foreclosure rate.

Homebuyers on the Way?

The declining price-to-rent ratio means that eventually more and more people are going to want to buy rather than continue to rent. After all, people have to live somewhere, and if the rent is going up and the price of houses continues to fall, people will buy, especially with low mortgage rates. The ratio is not particularly “cheap” by historical standards, but is just back to “normal.”

That is likely to limit the amount that existing home prices will fall over the next year to about 5%, rather than a repeat of the 30%+ decline we saw in the first down leg of the housing bust. I don’t want to minimize the significance of even a 5% further decline, but it is sure better than another 30% decline. It still represents a massive hit to the wealth of the middle class.

Since most people have mortgages on their homes, and usually they represent a large fraction of the total value of the house, the hit to wealth from a 5% decline in price is much larger than 5%. When the value of the mortgage gets above the value of the house, foreclosures become MUCH more likely. Theoretically, the foreclosure rate for people with positive home equity should be zero.

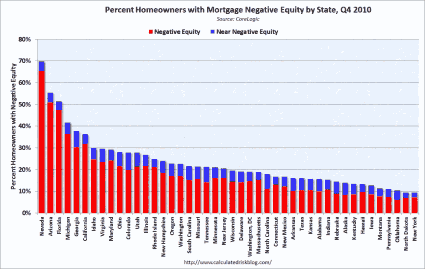

The next chart shows the percentage of homeowners with mortgages who are underwater or almost underwater, by state. The term “underwater” is somewhat ironic since the worst problems with people being underwater are happening in the Desert states Of Nevada and Arizona. If prices fall another 5%, the blue portion of the graph turns red.

It is a real mystery to me why so many people in Nevada and Arizona continue to pay their mortgages. It is one thing to continue to pay when you are just slightly below water. A house is, after all, a home, and non-economic factors can be very important. You might not want to move the kids from the school they are going to, for example. There is also still a social stigma attached to being foreclosed upon, although less so than a decade ago.

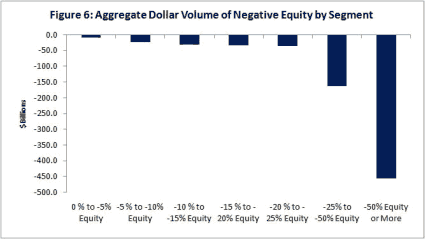

However, in the hardest-hit states, it is not like the mortgage is just 5% more than the value of the house, but often at the bottom of the Marianas Trench (the deepest spot in the ocean). As the final graph shows, by dollar volume, the vast majority of the problem is with people who are beyond the reach of scuba gear. It is extremely unlikely that the value of a house that is more than 50% underwater is going to come back to the point where the homeowner ever has positive equity.

Economically, continuing to pay on such a mortgage is just plain nuts, but people are still doing it. It is a good thing that they are not from the point of view of the banking system. If people defaulted on the $450 billion, as is clearly in their economic best interest, the capital of the banking system would be severely depleted again. That is one of the key reasons I think that the decision to allow the “too big to fail” banks like J.P. Morgan (JPM) to deplete their capital through higher dividends and share buybacks is a serious mistake.

The rapidly declining apartment vacancy rate is a very good sign that we will eventually work our way out of this mess. The recent uptick in the pace of job creation seems to have allowed the rate of household formation to go up.

In other words, people who have jobs are confident enough to move out of Mom’s basement and into a place of their own. People who have been living with three roommates might find that one of them now has enough income to get his own place. Since a kid moving out of the basement is unlikely to be in a position to buy a house, this will first show up in the apartment vacancy rate.

The unemployment rate for the people most likely to be in that position, people between the ages of 20 and 24 is still very high at 16.4%, but that is down from 18.2% a year ago. The next age group up, those between 25 and 34 years old, are the prime group for being first time home buyers. They face an unemployment rate of 9.3%, but that is down from 11.1% a year ago.

Given the severity of the downturn, it is likely that many of them were still living with Mom and Dad, or at least with several roommates. I suspect that much of the new absorption of apartments is coming from the twenty-somethings. The most obvious play on this trend is the apartment REITs.

We are not out of the woods yet on the housing front, and it remains the key reason that the economy still feels so sluggish. However, like a kidney stone, this too shall pass.

AVALON BAY (AVB): Free Stock Analysis Report

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply