Paul Krugman explains the main reason for the rising commodity prices:

[T]oday, as in 2007-2008, the primary driving force behind rising commodity prices isn’t demand from the United States. It’s demand from China and other emerging economies. As more and more people in formerly poor nations are entering the global middle class, they’re beginning to drive cars and eat meat, placing growing pressure on world oil and food supplies.

There are many observers who disagree with this interpretation. They argue it is loose U.S. monetary policy and speculation that is driving the surge in commodity prices. Krugman notes there is a way to test this alternative theory:

The last time the prices of oil and other commodities were this high, two and a half years ago, many commentators dismissed the price spike as an aberration driven by speculators. And they claimed vindication when commodity prices plunged in the second half of 2008.

But that price collapse coincided with a severe global recession, which led to a sharp fall in demand for raw materials. The big test would come when the world economy recovered. Would raw materials once again become expensive?

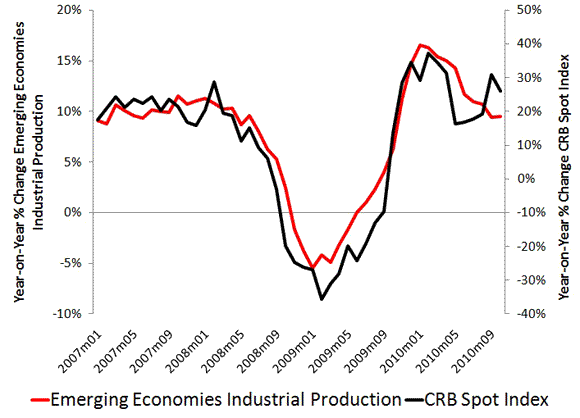

If so, then Krugman’s theory is more plausible. So what does the data show? Is there is a close relationship between the growth in emerging economies and commodity prices? Here is a figure that shows the year-on-year growth rates of industrial production in emerging economies and the CRB Commodity Spot Index:

Sources: NBEPA , Moody’s FreeLunch.com

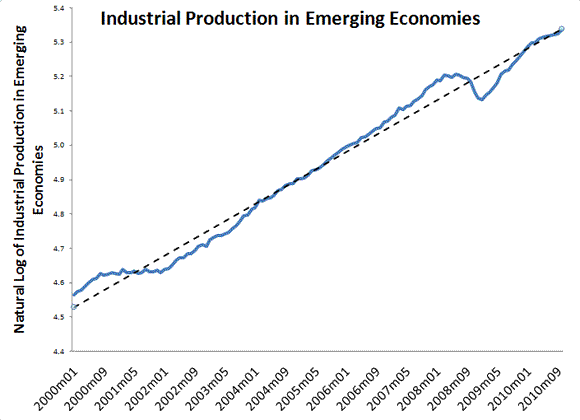

I’d say Krugman has a solid case. One could argue, though, that because the Fed’s monetary policy gets exported to much of the emerging economy its monetary policy is providing stimulus to these countries and through them is indirectly putting upward pressure on commodity prices. Even so, this still does not mean U.S. monetary policy has been too loose. It could be that the Fed’s global monetary stimulus is simply putting the emerging economies back on their trend growth path. After all, the emerging economies were growing in the double digits before the Great Recession and are only now returning to trend growth. This can be seen in the figure below:

Sources: NBEPA

At a minimum, Krugman’s argument should give pause to those observers who point to rising commodity prices as a harbinger of runaway inflation. There are many factors driving global commodity prices. U.S. monetary policy is only one of them and probably is not the most important.

Leave a Reply