Don’t fight the Santa. Markets are at sentiment extremes, at the highest levels since October 2007 just before the all-time top, and this has led the punditry to expect a reversal; but it rarely comes this time of year.

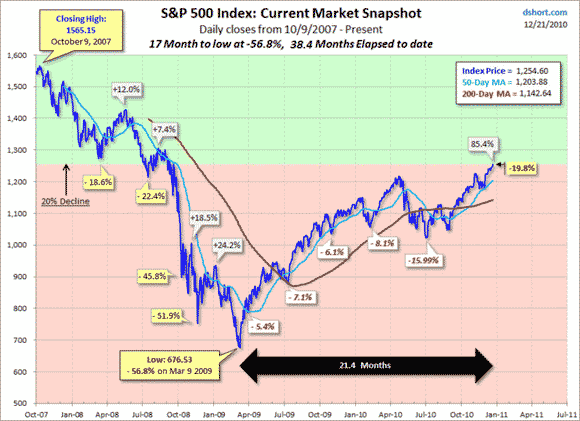

The Santa Rally comes on the soft whispers of machines turned off, as professionals close the books for the year and head home for the holidays. Markets tend to rise on light volume. More stats here. The rise often persists into the first few days of January, making January 10 the day to watch, but be cautious (chart courtesy Doug Short):

- In 2008, we started down in late Dec

- In 2009, we reversed hard on Jan 6

- In 2010, we ran until Jan 19

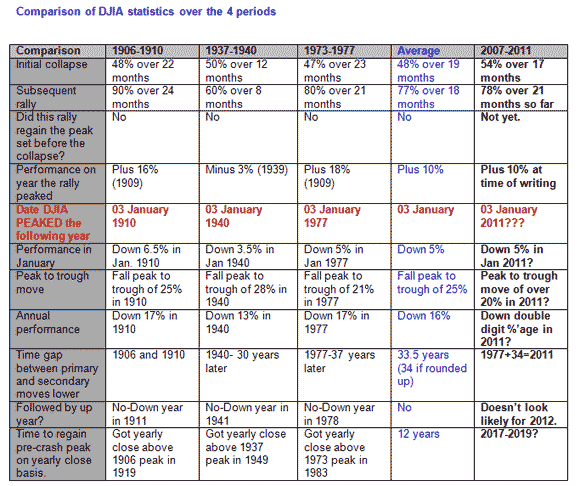

A more bearish view comes from Citigroup (C). They look at three similar prior markets (1906-10, 1937-40, 1973-77) and conclude that the market is likely to turn on January 3 and fall at least 20%. Their chart:

This outlook will be quickly dismissed by almost all market traders, given the optimism that reigns. I will provide a technical analysis in my next post, but let’s first explore the fundamental viewpoint. The sentiment extremes are driven by four core beliefs:

- QE2 will spill over into stocks and commodities (indeed already have!)

- The bond rout rotates investments into stocks

- The tax deals signals Obama will do what he can to pump into the 2012 election

- The economy is actually showing signs of life

QE and Bonds. I explored the first two in a recent post on Japan’s QE experience, which supports the view that stocks will tend to rise as the Fed continues some form of QE. One should take such analogies with a grain of salt, as many other conditions are different, especially the fact that the two US bubbles (dot-com and real estate) pulled Japan up; which large economy will pull the US up? This makes the final two beliefs of larger importance.

Tax Deal. I explored the tax deal in my prior post, concluding it is much less stimulative than it has been sold. It can be estimated at adding around 0.9% to GDP based on around $270B of stimulative effect over the next two years, with much of that in 2011. This is not very compelling, but sure beats the alternative of austerity and a real double-dip next year. Of course, this all happened in the lame duck Congress, and the Tea Party influence is not yet being felt.

In general, the Tax Deal bolsters the Four Year Cycle, which is driven by Presidential politics. The Four Year Cycle makes the two years leading into elections bullish. The third year tends to be the best for stocks as the President has taken the hits from his predecessor’s mistakes and is pumping the economy towards re-election. If the Prez waits too long to pump, as Bush Senior did in 1991, he risks not getting credit for the pump. (In that case, the economy had bottomed and was in a rebound through the 1992 election, but Bush got too little credit for it.) If he starts too soon, as Jimmy Carter did in 1977, he risks a flagging economy in the fourth year. Obama shot his arrows early, and we are now in the backside of the Stimulus where it will act more as a drag on growth than a spur. Best that can be said is we may avoid the 1937 analogy of a double-dip but are still waiting for a real recovery to start.

Signs of Recovery? So far Santa has left jobs behind. This recoveryless recovery is not showing the type of turn we have seen in prior rebounds. Q3 GDP just got revised up by a small amount (to 2.6% from 2.5%), which was below consensus (2.8%). Goldman has done a great job of parsing through the GDP revisions and concludes that they have to pull back from the prior optimistic view of 2011. Key changes:

- more inventory than before (1.6% vs 1.3%) – a bad sign if it doesn’t sell through

- less real final sales (0.9% vs 1.2%) – this is a key indicator of recovery

- lower corporate profits (0.2% vs 1%) – this may reflect a margin squeeze

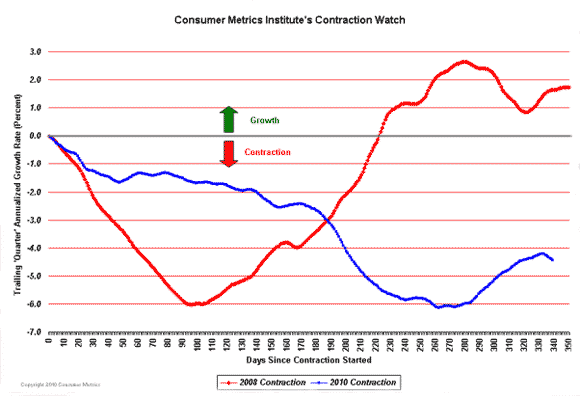

There have been signs of improvement in Q4, and I expect a higher Q4 GDP than Q3, but this report puts a damper on 2011. In particular, the consumer is not back, despite some promising holiday sales. Keeping the consumer on life support, such as the two most stimulative parts of the Tax Deal (the FICA tax reductions and the extension of unemployment benefits), is just kicking the can down the road. The Consumer Metrics Institute shows the consumer still in a funk, and starting to trend down again (the blue curve):

Leave a Reply