A plethora of reports on QE2 are coming in with low grades. It launched to a bumpy start, and many observers thought it wouldn’t have much of an impact in the real world (vs the worlds of speculation and expectations).

Global Bond Rout

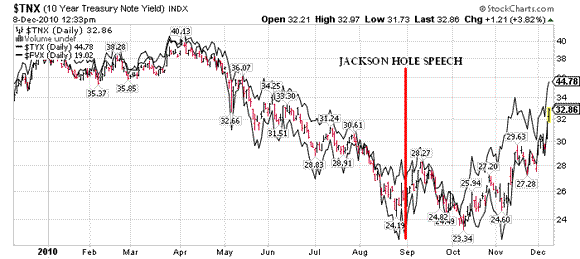

Most noteworthy is that rates have gone up rather than down, and up quite a bit – 60 bp in the ten-year – enough so it has pummeled the bond market and led to descriptions of a Global Bond Rout. PragCap shows how dramatic the reversal has been, albeit we are still below yields earlier in the year:

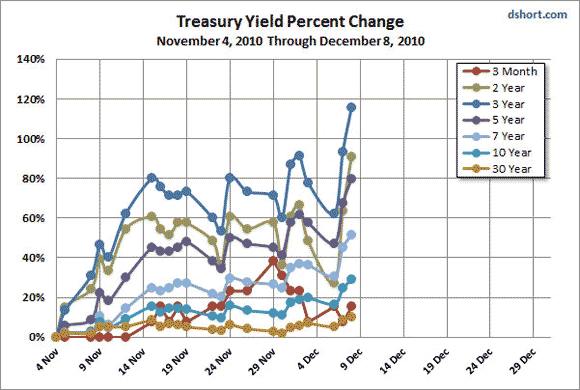

Doug Short piles on, showing how since the actual QE2 announcement in November, the rate increases have been dramatic:

Econbrowser did a careful, somewhat scholarly review, and generally concluded that whatever impact it was supposed to have had is being swamped but other events. Their primary criticism is that the Fed has executed QE2 in the mid-range of Treasuries, rather than the ten-year (or longer) bonds.

Banks Lending Again?

Another purpose of QE was to right the banks, encouraging them to lend again. Banks make money borrowing short and lending long, so a rise in long rates should encourage capital formaton.

John Mauldin adds a long, careful assessment of QE2 in his weekly newsletter, reprinted here. He sees unintended consequences to QE2: a global sell-off in sovereign debt. Why?

virtually every country in the world is grappling right now with how fast we get out of our fiscal stimulus and much do we worry about this longer term problem of debt

This may explain why rates spiked after the Obama tax deal was announced – it reflects more of the stimulus mentality, piling on more debt, than a change of approach to grapple with excess debt. The bond vigilantes disapprove.

John went on to ask whether QE2 had begin to fix the core problem of capital formation – in other words, are the banks ending again? The answer is a resounding no. Credit continues to contract, and now with the long bond over 4%, mortgages have gone up, further hammering the housing recovery. Indeed, housing has started a double-dip.

Inflation Increasing?

A third goal was to reflate the Dollar, with the view that rising prices would also encourage capital formation. I have always found this goal an odd one, perhaps a post hoc, ergo propter hoc fallacy looking back at the Great Depression. When FDR broke with gold, the USD fell and we had inflation. Did the recovery come for other reasons, brining inflation, or did inflation drive the recovery? In any event, in coming the financial blogs I have seen sophisticated arguments for increased inflation expectations, but no signs of inflation (other than asset speculation). Indeed, the inflation-adjusted Treasuries, TIPS, have not signaled higher inflation, rising with the ten-year not ahead of it. Instead, bonds are weak because of QE, not inflationary expectations:

The market sees the deflationary forces mixed with the inflationary signs and trades it to a draw. The market is shooting bonds because it is afraid and confused about the distortions that QE is causing.

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply