For the past three years, it has paid to bet on the pessimistic side of the outlook. For the past few months, I have privately fretted that this bet would soon wear thin. And it sure looks like it has. The flow of data in recent weeks has been, on net, very positive, offering a vision of a sustainable recovery.

The Fed, however, has not yet gotten that memo. From yesterday’s FOMC statement:

Information received since the Federal Open Market Committee met in November confirms that the economic recovery is continuing, though at a rate that has been insufficient to bring down unemployment. Household spending is increasing at a moderate pace, but remains constrained by high unemployment, modest income growth, lower housing wealth, and tight credit. Business spending on equipment and software is rising, though less rapidly than earlier in the year, while investment in nonresidential structures continues to be weak. Employers remain reluctant to add to payrolls. The housing sector continues to be depressed. Longer-term inflation expectations have remained stable, but measures of underlying inflation have continued to trend downward.

The Fed remains locked into a forecast that anticipates output growth hovering near potential. Contrast this with rising expectations for, at a minimum, solid near term growth:

In the most recent Wall Street Journal forecasting survey, conducted last week, the 55 economists on average expected GDP to grow 2.6% at a seasonally adjusted annual rate in the fourth quarter from the third. But on the back of today’s retail report and a strong increase in October exports reported Friday, many are revising their estimates to more than 3%. Of seven revised forecasts, the average expected fourth-quarter growth forecast is now 3.3%, compared to 2.6% before the retail release.

Despite all the weights on the consumer – the FOMC statement reiterates that list – consumer spending is accelerating, pulling the post-recession trend rate close to that pre-recession:

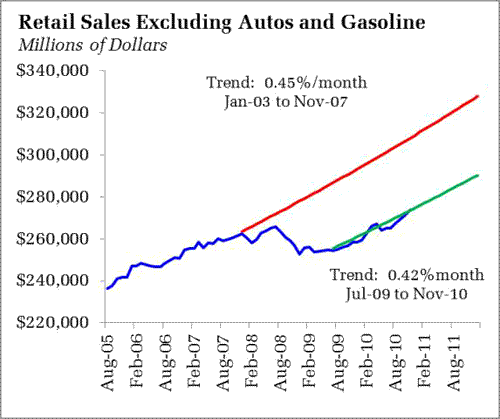

Over the last four months, the rate for nonauto retail sales less gas has accelerated to an monthly average gain of 0.8%. That is nothing to sneeze at, and easily explains rising forecasts.

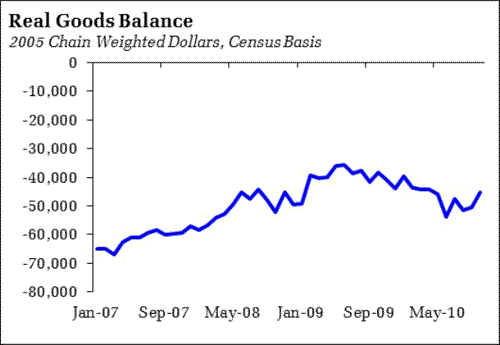

Still, the gap between the old trend and the new remains. Moreover, earlier this year, I would have tended to dismiss higher consumer spending on the grounds that it would simply be offshored in the form of higher import spending, a reemergence of the global imbalance that plagued output growth in the second and third quarters of this year. The most recent trade report indicates the opposite – that maybe, just maybe, the external sector will behave as it should in the wake of a financial crisis and provide a sustained boost to growth. To be sure, we would prefer not to see imports collapse, as this would signal a rather nasty demand shock. Instead, we are looking for import growth to stall as import competing firms become more competitive while export growth continues unabated. That has been the general trend of the last few months, giving rise to a more supportive trend in the trade balance:

This year, the external drag was an important factor in limiting the US recovery. Ending that drag would provide a significant boost – note that trade contributed a negative 2.63 percentage points to GDP growth, on average, in the second and third quarters. Thus, just going flat means a large gain to output. It’s simply a big deal – it’s enough to put output growth solidly in the sustainable region, not to mention solidly above trend.

And if an improving consumer and external outlook themselves would have been sufficient to generate above trend growth, the tax cut deal is icing on the cake. On net, it is more than anti-contractionary. It offers some real stimulus – for example, the payroll tax holiday will be less easily saved than a lump sum check in the mail. To be sure, we can debate the political wisdom of the move from the Democrat’s perspective, not to mention the long-term consequences of no real baseline for the US tax code, but in the short run, it is another shot in the arm.

And a shot in the arm is desperately needed. I do not intend to dismiss the real challenges the economy still faces. The plight of the 99er’s in an economy of near double-digit unemployment rates is an obvious reminder. And, for that matter, so is the most recent employment report. Of course monthly changes in nonfarm payrolls are notoriously volatile, and the average of the last two months revealed that payrolls are growing just above 100k a month. The right direction, but not fast enough. More demand is clearly needed – and a solid consumer sector bolstered by external support and fresh stimulus would clearly help in that regard.

In this environment, it is not really much of a surprise that long term interest rates are headed higher. I tend to agree with those analysts echoed by Jim Hamilton and Brad DeLong – rising rates are a signal that the economy is strengthening. And strengthening enough that, despite the pessimistic tone of today’s FOMC statement, it seems likely that the Fed will not feel compelled to extend large scale asset purchases beyond the existing plans. Without the Fed to serve as an excuse to keep buying Treasuries, traders are sending rates exactly where they should be going.

But won’t rising rates slow the housing recovery, thereby putting the recovery in jeopardy? Seriously, what housing recovery is there left to protect? Should we really care at this point? Housing is SOOO 2005. The consumer is getting over it – the retail sales numbers tell that tale. Consumer spending is growing solidly in the absence of easy credit. I think we are finally in the acceptance phase when it comes to the housing market. Just like we eventually got to the acceptance phase in the wake of the tech collapse. We use even more technology, but that still doesn’t justify the valuations we saw in the late 1990s. Same for housing – it is reverting back to an asset that provides primarily a service for the household rather than an investment. And that reversion will leave the economy healthier in the long run.

Will the Fed shift course, even in a rosier environment? Doubtful, at least near term. They will likely see the current plan through to its fruition, while holding rates at rock bottom levels until it is quite evident that the output gap is closing, which will take a few years even if growth accelerates sustainably to 4%. Will more be forthcoming? Also doubtful, especially as the composition of the FOMC turns more hawkish. Moreover, enough risks remain to keep Fed officials from sleeping too soundly at night. The European debt crisis runs hot and cold. The trade story could turn against us. Again. And uncertainty over the economic direction of China will be an ongoing challenge. I suspect the Fed will adopt the widely accepted view that a China slowdown would be a net negative to the global economy. Michael Pettis makes a convincing argument to the contrary.

In short: In general, the data flow of the last eight weeks is clearly encouraging. To be sure, not every release, like the employment report, is perfect. But enough are perfect that forecasters are quickly reversing the downgrades made just a few months ago during the mid-year slowdown. Will the data suddenly turn on us again? Always possible, always something to watch for, but I don’t think that should be the expected path. Right now, the data suggest the US economy might start firing on more than just a few of its eight cylinders. A little optimism is justified. Don’t expect the Fed to reverse course soon – they have yet to embrace the possibility that the economy is set to grow at something above trend. But a data flow like this cannot be ignored forever. Look for more glimmers of hope creeping into Fedspeak in the weeks ahead.

Leave a Reply