American Superconductor (AMSC) analysts continue to raise estimates, even as the company nears its next quarterly report. The growth rates and long-term outlook are fantastic for this Zacks #1 Rank (Strong Buy).

Company Description

American Superconductor provides technologies and solutions throughout electric power infrastructure, from generation to delivery. The company also offers wind turbine designs and other electrical control systems for renewable energy.

Estimates Up Ahead of Earnings

The Zacks Consensus Estimate for fiscal 2011 is up 2 cents in the past week, to $1.03. Next week’s consensus for American Superconductor is up a penny to $1.42. Given the 40 cents earned in fiscal 2010, the growth rates are 157% and 39%, respectively. The next quarterly update is expected in late October.

While the P/E ratios are still a bit lofty, the growth is worth the price. The PEG ratio is just 0.5 times.

One of the most import factors when it comes to estimate revisions is the timing. Analysts are very cautious, given the steep penalty for a stock that misses estimates. So, to see forecasts rising just ahead of an earning release is very bullish.

Good Earnings History

The last quarterly report was a great one and came on Jul 29. Revenues for the period were up 33%, to $97 million. Additionally, the gross margin improved dramatically, from 30.9% to 40.1%. These factors lead to exponential net income growth, from $1.8 million to $9.2 million.

Earnings per shares came in at 28 cents, 13 cents better than expected. American Superconductor has topped Wall Street’s expectations in 7 of the past 8 quarters, included the past 4.

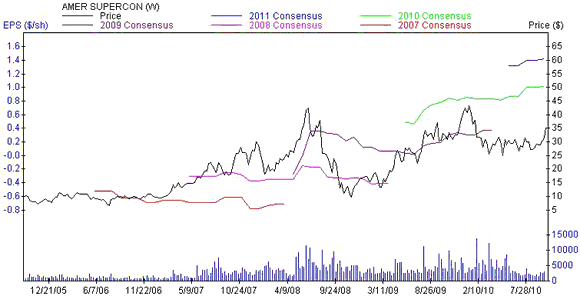

The Chart

Looking at the long-term earnings trend for American Superconductor, it is hard not to get excited about the prospects for the stock. Each colored line below represents the Zacks Consensus Estimate for an individual year. Over the past 5 year there has been a sizable improvement, from deep in the red, to well into the black.

Leave a Reply