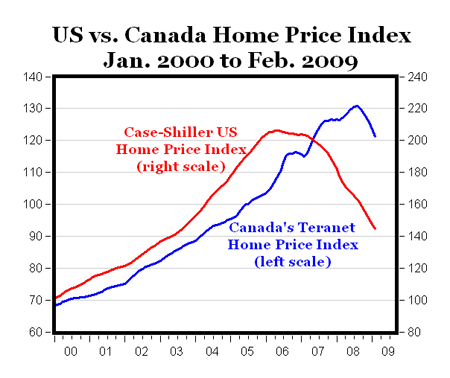

From the mid-2006 housing price peak in the U.S. (Case-Shiller Composite-20 Index, data here), home prices have fallen by about 30% (see chart above) through February 2009. From the mid-2008 peak in Canada (Teranet/National Bank of Canada National Composite Index, data here), prices have fallen by only 7.4% through February. Although Canada home prices may continue downward (along with U.S. home prices), it would appear so far that there was a much bigger housing bubble problem in the U.S. than in Canada.

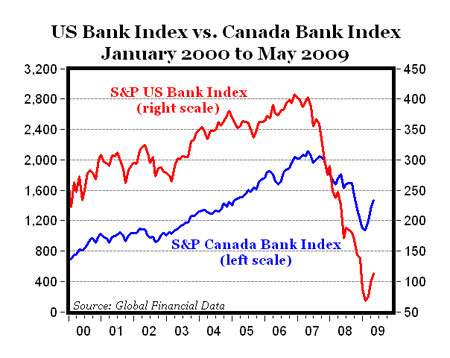

Likewise, there was a much more significant banking crisis in the U.S. than in Canada, see bottom chart above of the S&P US Bank Index and the S&P Canada Bank Index, from January 2000 to May 2009 (data from Global Financial Data, paid subscription required). Both bank indexes peaked about the same time in early 2007, but the U.S. bank index crashed by 80% through early 2009, compared to the 40% drop in Canada’s bank index over the same period. Year-to-date, both bank indexes are up about 30%.

From Nick Rowe, via Marginal Revolution, comes this list of why Canada’s banks are special, or at least different enough from US banks to explain the differences above in the recent housing market and banking problems:

1. Canada has never had restrictions on interstate banking, so Canadian banks spread their assets and liabilities across Canada, and it doesn’t matter if a local housing market goes bust. (This was also a major difference during the Great Depression when about 10,000 banks failed in the U.S. vs. almost no bank failures in Canada.)

2. Canada never had Glass-Steagall restrictions separating commercial banking from investment banking, and the investment banks in Canada joined the retail banks some years ago.

3. Canada doesn’t have mortgage interest deductibility for income taxes. So paying down your mortgage in Canada is a tax-free investment, and most people want to pay down their mortgages.

4. Except in Alberta, mortgages in Canada are fully recourse. You can’t just walk away from a negative equity home and hand the keys to the bank; the bank will come after you for the difference.

5. If a Canadian investor wishes to take some risk, the New York-based banks may be the most efficient means of doing that (added by Tyler Cowen).

Leave a Reply