Back in February and March on this blog I spelled out and provided supporting evidence why we would see very bad housing numbers by the time the July data came out… and here we are.

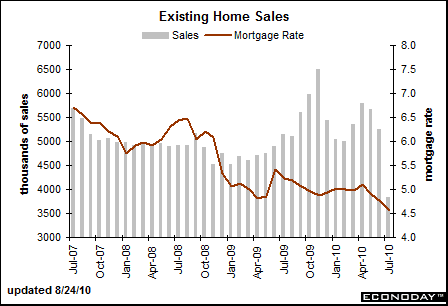

June was bad enough with Existing Home Sales of only 5.37 million (now revised down to 5.26m), and that set a negative tone and consensus expectations of 4.6 million for July. But reality just struck as July’s actual number came in at only 3.83 million, the lowest amount in modern history!

That was a 28.6% plunge from the original June report – in just one month, and it was a 25.5% year over year plunge from July of 2009.

Here’s Econoday’s report, hard to spin those numbers:

Highlights

It doesn’t get worse than this. Existing home sales fell 27.2 percent in July to a 3.83 million annual rate for the lowest level in 15 years. The 3.83 million rate compares with expectations for 4.65 million. Supply at the current sales rate ballooned from June’s already swollen 8.9 months to 12.5 months for the worst reading in 11 years.Yet prices showed little effect, down only 0.2 percent to a median $182,600 and reflecting relative strength for higher priced homes. The year-on-year median price edged lower but was still positive at 0.7 percent. Yet “was” is the word to note as extremely heavy supply, together with heavy foreclosures and distressed sales, point squarely at price pressures ahead.

There’s nothing to explain away July’s collapse. Single-family and condo sales show nearly the same deterioration. Regional data show no substantial variation. Stocks are moving lower and money is moving to safety in immediate reaction to this report, one that marks a new bottom for the run of disappointing economic data. The street was looking for an improvement in tomorrow’s new home sales report but that’s definitely now an outdated consensus.

Take a look at that chart and how the last vertical bar compares to the rest, which were already terrible… and to have historic low sales occur in the month of July is a disaster as we have yet to reach the end of the traditional sales season.

So, what does the future hold?

First, let’s acknowledge that this is NOT a bottom. This is because nothing has really been fixed, prices will remain under pressure, and that in turn will pressure all financials and the economy at large. The forces occurring now are attempting to cleanse. Much rests on actions yet to be taken. If we allow the cleansing process to continue unabated, we will be through it much more quickly as true investment opportunities arise. Should we continue to fight it with more crazy government schemes, then the process will be drawn out (is that the sound of an empty can I hear bouncing down the road?).

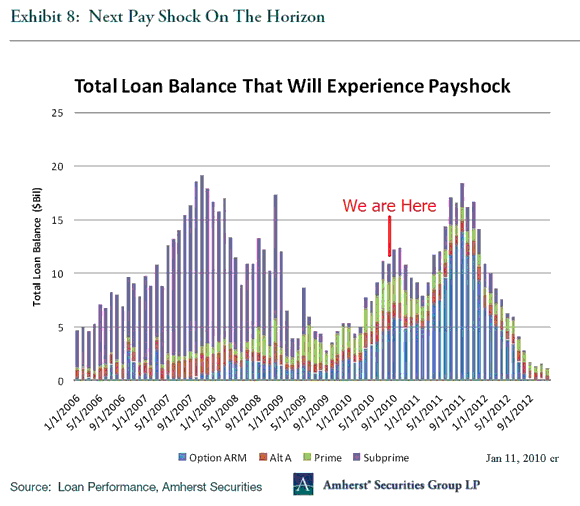

I have shown the mortgage reset chart many times, it has been a good predictor of when the data would turn down. We are now in a time where Option-Arm mortgages are resetting in large numbers, but this has only a short respite in a couple of months, and then zooms to a 2012 peak:

While Subprime loans affected the lower end of the housing market, Option-Arms affect the more expensive end. This will continue to pressure the Boomer’s large and expensive McMansions, producing a trend for smaller yet higher quality homes that are more conducive to low maintenance and lower costs later in life for those who can still afford it. Those who fail to recognize these trends will continue to sail along with the S.S. Titanic.

These numbers are a call to action. The Administration is going to have their Arms full with this one (pun intended).

Will heads roll? Will it help?

The answer is, no, it won’t help as no correct answer can be developed inside of the central banker box. However, there are crazy schemes and ideas floating around that may make it enticing to buy real estate sooner than later – but any such scheme will punish the dollar and step us further away from a true free market, thus being very negative in the long run should such schemes be attempted.

In the mean time, wave C down continues to unfold and the social mood is being impacted accordingly. This should be the wave that eventually brings about a true and sustainable bottom, but that bottom is still out in the distance.

We saw the dollar plunge in reaction to these numbers, particularly against the Yen. Yen strength is a symptom of deleveraging, it is mechanical as those who borrowed Yen at low rates to invest in America are forced to unwind that trade with the prospects of very lows rates here in the U.S. as well. It is NOT indicative of strength in Japan. The relative game of floating currencies is just that – all relative, but relative as we all shoot ourselves in the collective foot. This is a systemic problem, not a cyclical one, and thus it will continue until systemic change occurs.

Note on my prior post this morning, BEFORE this data was released, that some piece of data or news would justify the wave 3 movement that had already begun… this would be it.

Leave a Reply