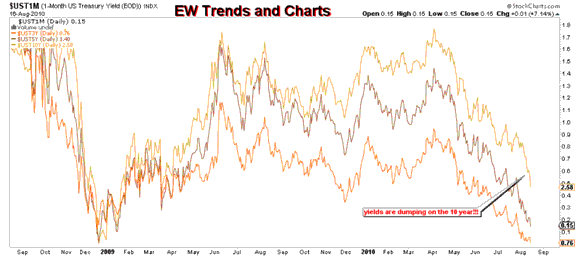

Bond yields are approaching the historic lows of 2009 during the flight to quality. The rapid drop in the 10 yr in the absence of the 2008 banking crisis is truly historic. Since the April high in stocks all the mid-term Treasuries have raced down in yields (chart from EWTrends):

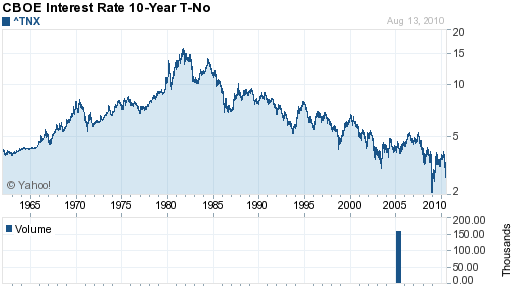

We may be approaching the end of a 30 year bond bull market, from the highs of 1980s to the potential lows of 2010. This chart from SeekingAlpha shows the trend:

The author raises the caution flag that a protectionist movement may be near. Seems a bit alarmist, but the Chinese currency, which began its float again to great fanfare, has now dropped for five straight days and is lower than it was then! Congress is now, once again, raising the spectre of retaliation.

A more prosaic explanation for the rush to bonds is a rise in fear, fear not of another banking crisis but of an economy rolling over again, this time (the fear story goes) with no weapons left to restart it.

A more prosaic explanation for the rush to bonds is a rise in fear, fear not of another banking crisis but of an economy rolling over again, this time (the fear story goes) with no weapons left to restart it.

GDP forecasts are being slashed. Goldman joins JP Morgan and Deutsche bank in lowering the coming Q2 revision to the low 1% range, and increasing double-dip odds to 25-30%. Looking forward, ZH reports that a “Philly Fed” forecaster sees Q3 dropping from expected 3.3% to 2.3%, and slower growth in 2011 and 2012. Chances of a negative Q4 are rising. Please refer to the charts in the ZH link for details.

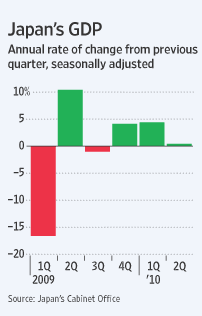

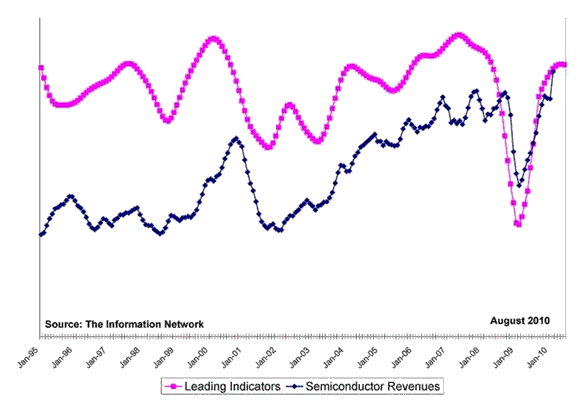

Japan’s GDP came in worse than expected, and led to a plethora of stories of how China has now overtaken it to become the world’s second largest economy. Well, not quite, but perhaps by the end of the year. Europe’s leading indicators have also rolled over, signaling a coming slowdown.

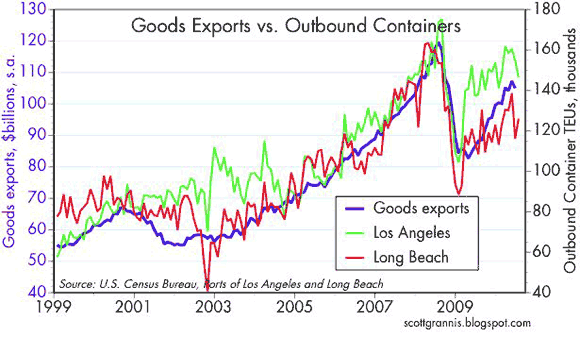

The normally bullish Califia Beach Pundit reports that container traffic out of LA is showing signs of a slowdown even as imports are surging. (See first chart below.) While they see that import surge as positive, it may be due to elevated expectations of holiday shopping, expectations that are not being met. There have been a flurry of news stories of how retail is slowing and the dismal back-to-school sales are (they hope) merely delayed. The govt report can be downloaded here.

Another poor sign is the rolling over of semiconductor sales based on a leading indicator. Since gadgets have been doing well, this is an ominous sign.

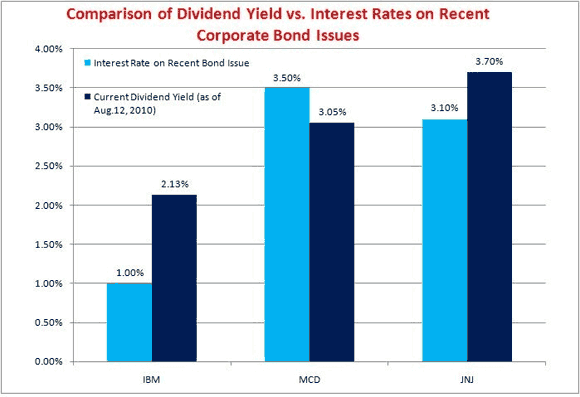

Given the low rates, corporations are jumping into the bond market. Even junk bonds issuances are increasing as investors scramble for yield. This suggests that all is not fear. Corporations are said to sit on record cash, giving junk bonds a allure of relative safety.

The question for investors is why buy at these low rates? There is less reason for a flight to quality today than two years ago.

The wave pattern strongly points to a bottom coming in bonds, and then a bounce (in yields). The Monday STU notes that the gap up in the morning may be an exhaustion gap. Bullish sentiment towards Treasuries is now 98%, approaching the incredible 99% on Dec 16, 2008, right before the all-time high.

One play is to buy the 30-yr. The recent Fed “QN” announcement targets the 2-10 yr Treasuries, which have dropped the most. The 30-yr may follow. The argument that inflationary expectations are keeping the 30-yr high are likely missing the dynamic that the Fed’s intervention is driving the mid-term rates lower. Right now being long the 10 and short the 30 is a likely arb play that may be keeping the 30 yr lower (higher yields). On the other hand, the intervention of the Fed has paradoxically made the 30 yr less sensitive to interest rate changes than the shorter term instruments. Hence the 30 yr may not move if inflation kicks in, while the 10 yr will move more if deflation kicks in.

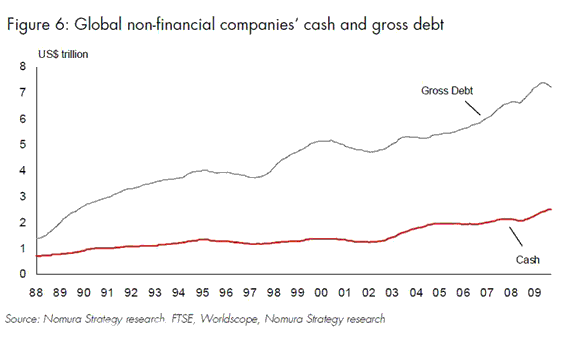

Corporate bonds should also be looked at cautiously. The widely held belief that corporations are sitting on hoards of cash needs to be tempered by the even larger hordes of debt they hold. Just as corporate cash is at an all time high, so is corporate debt: $2.6T of cash but $7T of debt.

Leave a Reply