The Fed released today its Stress-Test methodology – allowing some of the nation’s largest banks to have several days to challenge the findings before regulators makes results public the week of May 4.

From The Fed: A white paper describing the process and methodologies employed by the federal banking supervisory agencies in their forward-looking capital assessment of large U.S. bank holding companies was published on Friday.

The white paper is intended to assist analysts and other interested members of the public in understanding the results of the Supervisory Capital Assessment Program, expected to be released in early May. All U.S. bank holding companies with year-end 2008 assets exceeding $100 billion were required to participate in the assessment, which began February 25….

From this analysis, supervisors determined the capital buffer needed to ensure that the firms would remain appropriately capitalized at the end of 2010 if the economy proves weaker than expected.

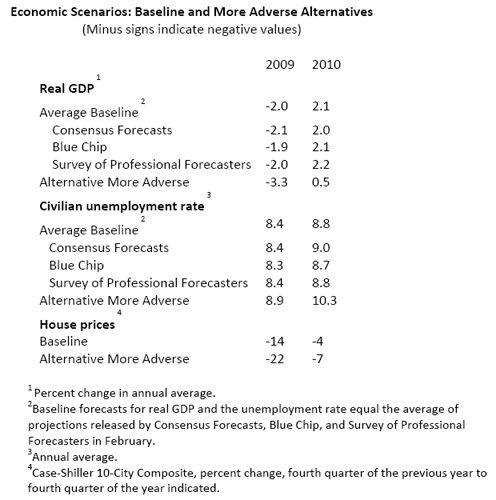

The baseline assumptions based on this table for real GDP 2010 and the unemployment rate 2010 don’t seem that stressful. GDP scenario for example is still positive while unemployment worst case is under -11%.

The Supervisory Capital Assessment Program: Design and Implementation available here »

Leave a Reply