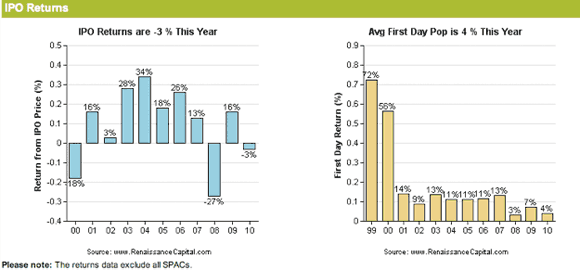

As we await the seminal Tesla IPO (TSLA), the IPO market continues to disappoint. Last week’s two tech IPOs, Motricity (MOTR) and Broadsoft (BSFT), both lowered their trading ranges then priced at the low end, and are currently 6-7% below even that. Solyndra, the solar startup that was visited by President Obama last month, canceled its IPO. Nat Goldhaber, a cleantech venture capitalist, remains bullish on cleantech IPOs but not on the solar sector, noting that Europe as been a center for solar and its austerity plans have dampened the solar industry.

TechCrunch ran an assessment of IPOs and how the poor IPO market has impacted the leading companies. Their chart shows how meager the first day pop has been, and how the companies have tended to do poorly in the after-market. As a consequence, the leaders of this generation of new ventures – Facebook, Zynga, LinkedIn, Twitter, Skype – have so far eschewed the IPO and relied on generating cash flow and private investment to grow. Many of the later round investors are allowing the early founders and employees to partially cash out.

It may be that we need a signature IPO – like Netscape in 1995 or Apple in 1980 – to spur the return of the IPO market. Many of the tech IPOs so far are not in that league, and instead fall into two categories:

- late 1990s vintage startups whose investors are seeking liquidity after a long slog, and

- dashing cleantech ventures who need oil-tanker-loads of capital to build out at scale

Maybe Tesla can restart the IPO market, at least for cleantech deals. Even green-industry stock analysts are skeptical. It is a bit daunting to imagine a new company taking on the huge scale players in autos, many of which are already into electric vehicles, especially Honda and Toyota. Yet it is conceivable. Here is why:

- The last successful auto startup in the US was Chrysler in 1925. Chrysler got out when it was possible to launch against the scale of the leaders – it marked the transition away from innovation to scale economics

- There have been a number of other car startups between Chrysler and Tesla, but none with the game-changing potential of Tesla

- It seems inevitable that we transition the fleet to electrics. It will take several decades. Tesla marks the first startup of this transition

- Tesla may also mark the beginnings of a restructuring of the auto value chain, to become less vertically integrated and more like the consumer electronics industry, and to iterate models more quickly. If so, the scale advantage of the leaders will be turned into a cost disadvantage

Tesla is the bet on the future of cars, not the past. Electrics represent a generational disruption to the auto industry, and usually out of these periods new winners emerge. A discussion of their pitch is here, and you can see the roadshow presentation here. Key slide: building a platform, not just a car:

Disclosure: I have a small indirect interest in Tesla

Thank you,Mr. Davidson for the honest and real story on what's REALLY going on with the ipo market today. Hopefully,your story will allow readers to make intelligent choices in regards to the upcoming Tesla Motors ipo.

Personally,I think that Tesla Motors will have a great opening day,"pop";then,over time,will go down in price until it can show a profit,then swing back in an upwards motion. I know this because I own shares of Quantum Fuel Systems Technologies(QTWW ticker symbol). I chose to put my money where my mouth is,and buy shares in this company,over the years(through cost dollar averaging), because it owns a large stake in Tesla Motors direct competitor: Fisker Automotive (www.karma.fiskerautomotive.com). Why? Because I'm more of a believer of hybrid technology,even though both companies have almost the same business model,pipeline,financial backing,price,location,etc.

I have already made peace that Quantum will mirror the direction of Tesla Motors(a big spike upward in price and come down, in price,over time)because the day traders/stock flippers will buy Quantum's stock to ride on the upward motion of Tesla Motors' stock price since Quantum Technologies is like Tesla;but,cheaper;or,buy Quantum's stock because they(for whatever reasons)couldn't get Tesla Motors at the ipo price.

Again,thanks Mr. Davidson for your honest reporting.

Rats! Typing fast again. here is the following correction: "Fisker Automotive (www.karma.fiskerautomotive.com)" should state," Fisker Automotive. http://karma.fiskerautomotive.com/ ".