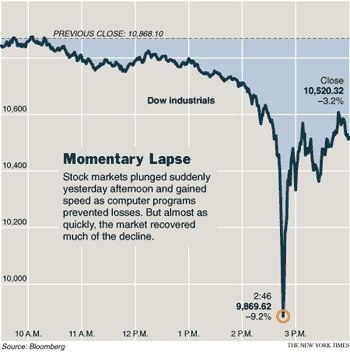

While the punditry still searches for a “glitch”, ZH got it right: we are seeing the consequence of a market driven primarily by ‘bots. Read the WSJ take on this in The Dark Side of Algorithms, followed up by Computer Trading is Eyed, summarized:

When the NYSE went into a circuit-breaker slowdown, called by the human specialists, trades spilled over into other exchanges. The specialists only manage 25% of trades anymore.

The ‘bots take advantage of inter-exchange divergences and found them, as the NYSE fell behind.

Two major ‘bots had also shut down from trading. The buyers had left the market.

You can listen to the voice in the pits: there were simply no buyers, no bids.

This is how Accenture got to 1c: the ‘bots ran down price points in microseconds looking for a bid, and seeing none, went to the bottom. No buyers, no bids.

The mindless machine did what a human market maker would never do. A person would have realized something odd was up and stopped. The human market-makers did react, but their time scale is measured in seconds – an eternity to a ‘bot.

When the ‘bots hit the bottom, literally, at 1c, they stopped, as any idiot-savant machine would do. When a real (human) bid came in, it was way above the fake HFT attempt to suck all the margin between bid/ask.

When the NYSE went into a circuit-breaker slowdown,

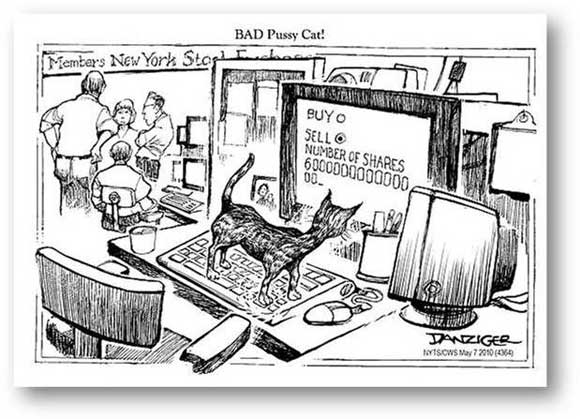

When the NYSE went into a circuit-breaker slowdown, You could do a pretty funny treatment on this, when the dust settles: see what happens when you turn the market over to HFT ‘bots gaming each other! Maybe this is how we can get to Dow 36,000!

Maybe instead this fall will scare the H (as in HFT) out of us. Read Sy Harding’s morning rant: program trading used to arbitrage inter-market divergences, but that is below 1% of their activity. The other 99% is gaming the system for no useful value. Ever wonder why we get magic runs up near the close? Did you know that ‘bots are now 50-70% of all trading? And where was their supposed liquidity when we needed it?

How did our rudderless SEC let it come to this? HFT is designed to skim the margin between bid & ask, scamming the real traders who are trying to take or lay off a real position in a real market. The machines trade back and forth, gaming each other, and not taking real positions. Now that we know the purported “liquidity” justification is bogus, why wouldn’t the SEC ban HFT Monday morning?

The fault lies not in our machines, but in our saves – our reckless attempts to paper over real problems with gobs of debt and heaps of hope.

Economists talk of “moral hazard” and people’s eyes glaze over. Let me try this:

We live in the Era of Entitlement where:

- Greece can live beyond its means

- Greek public workers can retire young

- California public workers deserve above-market salaries

- It is ok to fake an injury to get better retirement benefits

- People who cannot afford a house should be able to buy one anyway

- Liar loans are ok as long as fees get paid and someone else bears the risk

- Katrina may have been a problem, but it was somebody else’s problem, so we didn’t need to stock fire-booms to prepare for an oil spill

… and on and on across all sectors of responsibility.

There is feverish activity this weekend between the IMF, central banks, European governments and investment banks to come up with a better bailout of Greece: a Wolfpack Fund. The first solution ran into the Creditanstalt Problem that I warned about two weeks ago: instead of calming markets, creditors took it as their last chance to run for the doors before the rest of the PIIGS-in-Poo failed.

The Wolfpack solution is based on the false premise that the problems are coming from the pack of wolves (shorts) trying to drive down the Euro and the bonds of the PIIGS. The wolves are simply calling the bluff of papering over the problem without fixing it (which means getting the PIIGS debt back in alignment with their income). The Wolfpack fund is larger (€500B) than the last fix (€110B), but rather than ameliorate the run is likely to embolden it: it gives liquidity when the problem is insolvency. The PIIGS are still insolvent with no way to cover the debt nor the will to take tough measures other than to rely on the generosity of strangers to push the can down the street a little farther.

The whisper this weekend is Wolfpack will be further backstopped by €1T from the Fed and ECB, financed by quantitative easing (QE). Since no one believes the Greeks are serious about solving their problems, what if this backstop fails? There is no other bullet left in the gun.

The crash last week may have finally begun to change minds: Tom Friedman in the Sunday NYT talks of taking a root canal to the problem rather than painkillers. Andy Kessler in the WSJ suggests that the cornerstone of confidence in the Euro has broken, and the Euroland entitlement problem has to be faced. Papering over the problems and continuing the Era of Entitlement with false promises fueled by debt is not the path of serious people. Maybe it is time to take the problems seriously. I fear, however, the blue pill of the Keynesian dreamworld will require the final $1T backstop to be tried, and fail, before we can finally take the red pill and deal with the reality.

Until then, party on! A Wolfpack Bailout will likely bolster the Euro and spark a 300-400 pt rally in the Dow.

Leave a Reply