Of course the headline number is the 271,000 payroll jobs created last month. But the real reason the Fed is likely to raise rates in December (barring some unforeseen shock in the November jobs report, or international crisis) is the wage number:

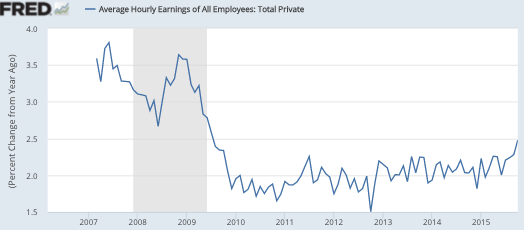

With the October figures, year-over-year wage growth has risen to 2.5% (actually 2.48%). It does look like we are finally getting some faster wage growth.

Of course you also see lots of zigzagging. Nonetheless, I think the October data makes it likely that the underlying trend has finally moved above the roughly 2% rut we’d been in since 2009. Perhaps 2.4% is a reasonable guesstimate. That’s still less than the pre-recession wage trend line (around 3.5%), but I don’t expect us to get back to that rate of growth in wages. My hunch is that 2.5% to 3.0% will be the new normal, over the next 5 years.

Right now I’m a bit puzzled by the TIPS spreads. They’ve moved up slightly in recent weeks, but the 5-year spread (1.32%) still seems somewhat inconsistent with the underlying trend wage data, which suggests 1.5% to 2.0% inflation.

I seem to recall that Yellen is very interested in the wage data, which is why I think the Fed will raise rates in December. Rising wage growth suggests we are back at the natural rate of unemployment. The rising wage growth also makes it slightly more likely that the Fed is on target for 2% trend inflation, although the TIPS spread suggest otherwise. I can’t reconcile those two numbers, unless the TIPS market is pricing in another recession in the next 5 or 10 years, during which time inflation would slow once again.

If there is no recession in the next 5 years, then the current TIPS spread of 1.32% seems implausibly low, given rising trend wage growth. Perhaps some of the mystery is explained by a liquidity premium on conventional bonds, depressing TIPS prices and raising yields closer to conventional bond yields. Or maybe October’s wage growth was a fluke.

To conclude in my typical wishy-washy way, I still don’t see a compelling case for a rate increase in December, but I also don’t see much evidence that it would do significant harm to the economy. The recent data makes it a close call. The Fed’s real problem now is not next month’s fed funds target, it’s that it lacks a long run strategy for monetary policy. It still has not learned how to operate in a low NGDP growth environment—and better come up with a plan before the next recession.

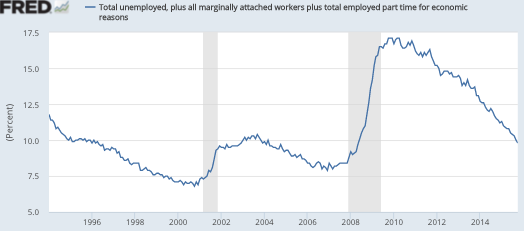

PS. No, the U6 unemployment rate (9.8%) is not horrible. It was 9.7% in October 2004, 15 months before the housing boom peaked. In was 9.7% in July 1996, almost half way through the Clinton boom. It’s not a great number, but it’s not horrible.

In other news, China’s bear market in stocks is officially over, as shares have risen more than 20% from August lows. There are lots of reports that the consumer sector in China is red hot:

More than 1m Chinese will go on a cruise holiday this year — nearly five times as many as in 2012 — a statistic that has whipped the global industry into a record expansion of ship orders and a collective decision to sail the world’s largest and most luxurious mega-vessels eastward.

The government also announced that the Hong Kong and Shenzhen markets will be linked later this year. The RGDP growth target for 2015 to 2020 was just announced at 6.5%. Apocalypse later?

Leave a Reply