“Much better than expected.”

That’s how John Derrick, Director of Research here at U.S. Global Investors, summed up his trip to Greece, the beleaguered country that hopes to put its financial woes behind it and rise again like the phoenix from the Mediterranean culture’s ancient mythology.

Last week I spoke with John about his trip, which took place following his visit to Turkey to meet with companies held in our Emerging Europe Fund (EUROX). Here are the highlights of our conversation.

So why do you say “better than expected”?

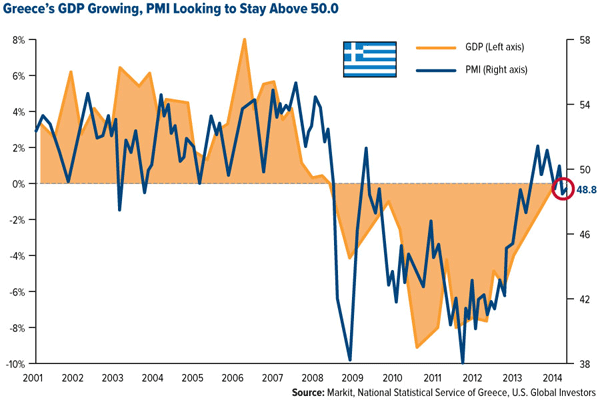

Greece has been in recession for six years now but it’s finally on track to turn things around. Its economy has stabilized and is beginning to improve since the crisis. It has a balanced budget. The projected GDP growth rate for this year is 0.6 percent, which doesn’t sound great, but it would be the first time since the end of 2008 that it’s been above zero. We’d like to see the purchasing manager’s index improve, though—it’s been below 50.0 for four of the past five months, indicating that the country’s manufacturing sector is still in contraction mode.

Greek citizens are fed up with austerity measures that were set in place to secure a multibillion-dollar bailout, and their egos were bruised after their country was downgraded last year from a developed market to an emerging market. But as the saying goes, the darkest hour is just before the dawn, and we’re now beginning to see a glimpse of the sunrise, so to speak. The painful adjustments have already been made, they’re behind Greece now, and the worst appears to be over.

Prime Minister Antonis Samaras, in fact, plans to ease out of the European Union’s bailout by the end of this year, which would be a whole calendar year ahead of schedule. In doing so, he might also siphon support away from anti-austerity candidates in the far-left Syriza party.

The mostly positive results from the European bank stress test seem to confirm that things are better than expected.

They do. There was a lot of anxiety going into the results, and there was this collective sigh of relief after they came back better than expected. Markets responded positively. Of the 25 banks that the European Central Bank (BCB) failed, only two were Greek: Eurobank and the National Bank of Greece. This shows that the Greek financial sector is trying to stabilize in a time when it’s predicted that the eurozone might face its third recession in six years.

The slump in the Greek shipping industry, very important to Greece’s economy, is partially to blame for the country’s current troubles. Has it improved any?

The slump in the Greek shipping industry, very important to Greece’s economy, is partially to blame for the country’s current troubles. Has it improved any?

Not by much, unfortunately. I met with two shipping companies, Goldenport and Tsakos Energy Navigation. What I took away from these meetings is that dry bulk shipping rates are not recovering as expected. The industry is washed out, with many companies having been put out of business over the last three years.

The good news is that this is probably the time to accumulate these types of companies, as many of them are trading at attractive discounts to net asset values (NAVs). But it’s still a waiting game until rates head higher.

On the crude and product transport side, lots of boat supply companies are hitting the market in the next two years, and rates have recovered some. They might move modestly higher in the short term. Tsakos has talked about a master limited partnership (MLP) structure before, but that sounds like a 2016 event if it ever gets done.

Talk a little about the Greek retailing industry.

This was the best part of my visit to Greece. I met with two retailers, Jumbo and Fourlis, both of which are seen as survivors in a down economy, with very strong market share.

Jumbo, kind of like a low-end Target, has 40-percent market share in its category. I visited the store and its layout resembles an IKEA—there aren’t any traditional aisles, and you basically have to walk through the whole store to get out. Its key products are toys, seasonal items and stationery. One of the most popular retailers in Greece, Jumbo plays its cards pretty close to the chest. Its management team doesn’t go to or hold conferences—they don’t even do conference calls, actually. This hurts valuation, but the financials have been very strong.

As for Fourlis, it holds the IKEA franchise for the region and also owns a sporting goods franchise, Intersport, which is seeing positive year-over-year same-store sales. Besides home furnishings and sporting goods, it’s also involved in fashion and electronic appliances. The company’s been operating since 1950 and has locations not just in Greece but also Romania, Bulgaria, Turkey and Cyprus. With the recent Greek equity selloff, this is likely an opportunity.

Leave a Reply