The economic consequences of financial crises have been systematically explored. Their political consequences haven’t. This column argues that without paying attention to politics, crises will remain poorly understood. After all, politics shapes policy choices, market sentiment and, ultimately, economic outcomes. Evidence from the effects of banking crises over the past century show that crises have a dramatic impact on the survival prospects of governments.

The wave of banking and sovereign-debt crises that began in 2007 has had powerful and continuing economic consequences (IMF 2013a; 2013b). Economists have used long run historical data to investigate the economic aftermaths of financial crises, but we lack any equivalent panoramic analysis of the impact of crises on politics. This is an important gap because these political effects, especially the survival prospects of incumbent governments, can shape governments’ post-Crisis policy choices, market sentiment, and thus economic outcomes. The manner in which citizens have reacted to financial crises has changed significantly over the past century, with ongoing consequences for how governments have responded to crises. This has helped to foster political-economy cycles of financial stabilisation and renewed instability.

Aftermaths of financial crises? Analyse the political consequences

Most economic analyses have focused on the impact of financial crises on economic outcomes such as growth, employment, and inequality (e.g. Koo 2009, Reinhart and Rogoff 2009, Perri and Steinberg 2012, Kose, Loungani, and Terrones 2013). But the recent financial crises in Europe and the US have also had significant political consequences, in turn affecting governments’ policy choices, market responses, and thus economic outcomes. Existing work by political scientists in this area remains patchy: qualitative investigations have focused on particular periods, countries and regions (e.g. Barreyre 2011, Eichengreen 1992, Frieden 1987, Gourevitch 1986, Haggard 2000, MacIntyre 2002, MacIntyre, Pempel and Ravenhill 2008, Simmons 1994), whereas statistical analyses have used relatively narrow and recent time windows (Bernhard and Leblang 2008, 2012; Crespo-Tenorio, Jensen and Rosas 2012; Hellwig and Coffey 2011; Pepinsky 2012). A fuller understanding of the aftermaths of financial crises thus requires more systematic analysis of their political impact, including a more comprehensive analysis of how this has varied over time and space, as well as through various institutional types.

Financial crises as bad news for political incumbents

The political science literature on ‘economic voting’ is divided on questions of the extent of voter rationality and whether voters are retrospectively or prospectively oriented (see Anderson 2007). But most agree that financial crises are unusually bad economic news for political incumbents. Others argue that the propensity of citizens to punish governments will also depend on whether they can easily identify who is responsible: the greater the ‘clarity of policy responsibility’, the greater the propensity to punish (Powell and Whitten 1993). Thus, more personalised, ‘executive-dominated’ political systems are commonly seen as more vulnerable to punishment than parliamentary systems, particularly when power is shared in the latter between different parties in a coalition. This should apply particularly strongly in democracies, where ease of leader replacement is greater than in autocracies. However, financial openness may blur responsibility by enabling governments to deflect blame for instability on to external factors (Crespo-Tenorio, Jensen and Rosas 2012; Hellwig and Coffey 2011).

Taking time and changing societal expectations seriously

These standard political science propositions are forms of comparative statics, but we believe that the propensity of citizens to punish political incumbents might also vary substantially over time in response to changing social conditions, economic knowledge and policy expectations. Our research shows how the political impact of banking crises on political turnover has changed dramatically over the past century due to the emergence of ‘great expectations’ on the part of modern citizens (Chwieroth and Walter 2013). Before the mid-20th century, although interest groups sometimes mobilised along distributional lines on matters of economic policy, citizens did not generally hold clear and strong expectations that governments were broadly responsible for macroeconomic stabilisation, including preventing major financial crises and mitigating their overall consequences. As economic knowledge grew substantially in the first half of the twentieth century and as political parties increasingly competed in terms of their ability to manage the economy in the wake of the Great Depression and World War II, citizens’ expectations of government policy responsibilities became far more extensive (Blyth 2002, Krugman 2007, Milward 1984, Romer and Romer 2002).

We examine how this has had important implications for the political economy of financial crises and policy responses. One implication is what we call a ‘rising bar’ hypothesis: as citizen expectations of government stabilisation responsibilities rise, crises will have a higher negative impact on incumbent survival prospects after the interwar period (controlling for other factors). A second implication is that the ‘clarity of responsibility effect’ mentioned above will be contingent upon the emergence of great societal expectations, so that crises will have a higher negative impact on incumbent survival prospects in executive-dominated democracies after the interwar period. A third implication is that more informed citizens will become increasingly attentive to the perceived effectiveness of incumbent governments’ policy responses to crises – that is, they become more prospective over time as well as more demanding of governments. Thus, citizens should become more likely over time to punish incumbents in political systems subject to gridlock due to the presence of significant numbers of distinctive partisan veto players.

New panoramic data

To test these propositions, we utilise a new dataset for 20 developed and developing countries since the early 19th century. We follow Reinhart and Rogoff (2009) in the definition and timing of banking crises. As for political turnover, we build on Crespo-Tenorio, Jensen, and Rosas (2012) in constructing a yearly indicator of ‘incumbent partisan spells’ based on the partisan affiliation of the government. This partisan spells indicator, which takes into account differences within and across democratic and authoritarian regimes, measures when incumbent government parties, not individual leaders, lose office. It allows us to compare outcomes across systems with different institutional characteristics, such as term limits and fixed vs endogenous electoral cycles. The data set contains 428 partisan spells, of which 81 experienced a banking crisis (18.9%).

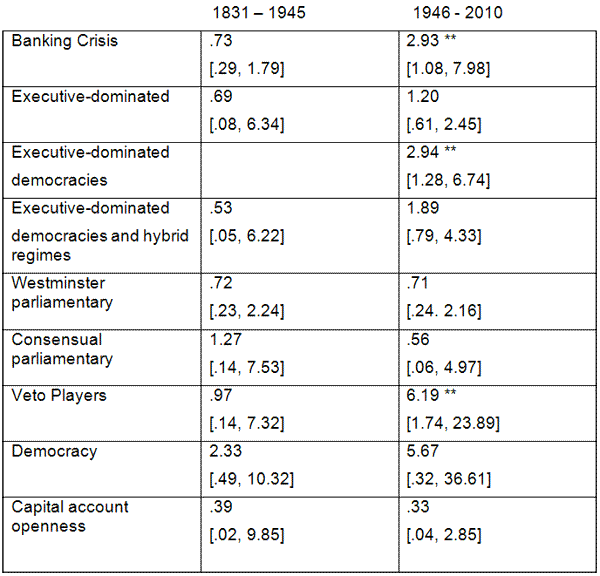

Table 1 summarises our findings. The results in the first row of the table below indicate the risk of incumbent turnover given a banking crisis alone. The results provided in rows two to eight are estimates of the risk of incumbent government termination given a banking crisis under a variety of different institutional and economic conditions. To test our argument that there is a threshold effect after the Great Depression we segmented the data into two periods, 1831-1945 and 1946-2010, and estimated risk ratios for both periods using survival analysis.1 Risk ratios greater than one suggest the incumbent political party faces greater risk of losing office. Values less than one imply the reverse. A value of one indicates no effect. Confidence intervals are in brackets.

Table 1. Comparison of government termination risk ratios under different configurations

The cells for row one report the risk ratio for the presence and absence of a banking crisis alone. All other cells report risk ratios that compare a government facing a banking crisis and high values of the covariates against a government facing a banking crisis and low values of the covariates. ‘High’ values for executive-dominated and Westminster and consensual parliamentary systems correspond to their presence, while ‘low’ values correspond to their absence. ‘High’ and ‘low’ values for all other variables correspond to one standard deviation above and below the mean respectively (** p < .05). No estimates are provided for executive dominated democracies in the earlier period due to insufficient data.

The evidence provides strong support for our argument that there is a powerful threshold effect. Before 1946, banking crises do not heighten the risk of partisan spell termination. Everything changes after 1945, however, when banking crises sharply and significantly raise the risk of government loss of office for all countries. Moreover, it is in executive-dominated democracies where this effect is most significant – in such cases, the risk of losing office given a banking crisis is about three times higher than non-executive-dominated democracies. But the risks are greatest after 1945 in cases where there is a relatively high degree of diffusion of political power: governments in countries with relatively high numbers of veto players suffer risks of losing office given a banking crisis about six times higher than in countries where political power is more concentrated.2 Our results also suggest that citizens are generally unforgiving of incumbent governments in financially open economies.

Implications

History and politics matter. Citizens have become both much more demanding of governments and more prospectively oriented since 1945. Governments perceived as unable to respond effectively to mitigate the consequences of crises for income, employment and wealth are by far the most likely to suffer political punishment.

A number of paradoxes arise from our analysis:

- First, rising societal expectations regarding crisis prevention and mitigation have more than cancelled out the political benefits accruing to incumbent governments that might have followed from the diffusion of improved macroeconomic and financial stabilisation policy techniques.

- Second, as expectations of post-crisis mitigation have diffused and become entrenched, governments seen as unable to respond effectively are likely to suffer exceptional levels of punishment.

- Third, no doubt governments have responded to these expectational constraints by attempting to deflect blame to others, by trying to reshape the institutional and policy environment in which they govern, and by trying to lower societal expectations about the possibilities of government stabilisation policy.

But the evidence suggests that great expectations persist regardless of formal policy constraints or attempts to shift blame.

- Finally, great expectations may themselves be destabilising;

Our findings suggest a socio-political origin for Minskian cycles (Minsky 1982): society expects crisis mitigation policies, governments intervene at growing cost and with increasingly large distributional consequences, and these interventions in turn produce moral hazard and may reduce long-run financial stability (IMF 2013a).

References

•Anderson, Christopher J (2007), “The End of Economic Voting? Contingency Dilemmas and the Limits of Democratic Accountability”, Annual Review of Political Science 19, 271-96.

•Barreyre, Nicolas (2011), “The Politics of Economic Crises: The Panic of 1873, the End of Reconstruction, and the Realignment of American Politics”, The Journal of the Gilded Age and Progressive Era 10(4), 403-423.

•Beck, Thorsten, George Clarke, Alberto Groff, Philip Keefer, and Patrick Walsh. (2001), “New Tools in Comparative Political Economy: The Database of Political Institutions”, World Bank Economic Review 15(1), 165-76.

•Bernhard, William, and David Leblang (2008), “Cabinet Collapses and Currency Crashes”, Political Research Quarterly 61(3), 517-531.

•Bernhard, William, and David Leblang (2012 ), “Bank Crises and Political Survival”.

•Bolt, Jutta, and Jan Luiten van Zanden (2013), “The First Update of the Maddison Project; Re-Estimating Growth Before 1820”, Maddison Project Working Paper 4.

•Blyth, Mark (2002), Great Transformations: Economic Ideas and Institutional Change in the Twentieth Century, Cambridge, Cambridge University Press.

•Chwieroth, Jeffrey M. and Andrew Walter (2013), “From Low to Great Expectations: Banking Crises and Partisan Survival Over the Long Run”.

•Crespo-Tenorio, Adriana, Nathan M Jensen and Guillermo Rosas (2012), “Political Liabilities: Surviving Banking Crises”, Comparative Political Studies (forthcoming).

•Elkins, Zachary, Tom Ginsburg, and James Melton (2012), Comparative Constitutions Project.

•Frieden, Jeffry A (1987), Banking on the World: The Politics of American International Finance, New York, Harper and Row.

•Geddes, Barbara, Joseph Wright, and Erica Frantz (2012), “New Data on Autocratic Regimes”.

•Gourevitch, Peter (1986), Politics in Hard Times: Comparative Responses to International Economic Crises, Ithaca, Cornell University Press.

•Haggard, Stephan (2000), The Political Economy of the Asian Financial Crisis, Washington, DC, Institute for International Economics.

•Hellwig, Timothy, and Eva Coffey (2011), “Who’s to Blame? The Distribution of Responsibility in Developing Democracies”, British Journal of Political Science 41 (2), 389-411.

•Henisz, Witold Jerzy (2010), Political Constraints Index Dataset.

•IMF (2013a), Global Financial Stability Report, April 2013, Washington, DC: IMF.

•IMF (2013b), World Economic Outlook, April 2013, Washington, DC: IMF.

•Koo, Richard C (2009), The Holy Grail of Macroeconomics: Lessons from Japan’s Great Recession, New York, Wiley, revised edition.

•Krugman, Paul (2007), The Conscience of a Liberal, New York, WW Norton.

•MacIntyre, Andrew (2002), “Institutions and Investors: The Politics of the Financial Crisis in Southeast Asia”, International Organization 55(1), 81-122.

•MacIntyre, Andrew, TJ Pempel, and John Ravenhill (2008), Crisis as Catalyst: Asia’s Dynamic Political Economy, Ithaca, Cornell University Press.

•Milward, Alan S (1984), Reconstruction of Western Europe, 1945-1951, Berkeley, University of California Press.

•Pepinsky, Thomas B (2012), “The Global Economic Crisis and the Politics of Non-Transitions”, Government and Opposition 47(2), 135-161.

•Powell, G Bingham, and Guy D Whitten (1993), “A Cross-National Analysis of Economic Voting Taking Account of the Political Context”, American Journal of Political Science 37(2), 391-414.

•Quinn, Dennis P, and A Maria Toyoda (2007), “Ideology and Voter Preferences as Determinants of Financial Globalization”, American Journal of Political Science 51(2) 344-63.

•Reinhart, Carmen, and Kenneth Rogoff (2009), This Time is Different: Eight Centuries of Financial Folly, Princeton, Princeton University Press.

•Christina D Romer and David H Romer (2002), “The evolution of economic understanding and postwar stabilization policy”, Proceedings, Federal Reserve Bank of Kansas City, 11-78.

•Simmons, Beth A (1994), Who Adjusts? Domestic Sources of Foreign Economic Policy during the Interwar Years, Princeton, Princeton University Press.

__________

1 We include a number of control variables, including a measure of capital account openness from Quinn (2008), annual economic growth (Bolt and Van Zanden 2013), and the cumulative number of previous banking crises.

2 The measure of veto players is from the Political Constraints Index Dataset (Henisz 2010). In our paper, we investigate the robustness of these findings through a variety of techniques, including by addressing the possibility of endogeneity (that higher rates of political turnover might raise the risk of suffering a banking crisis). The threshold effect for the veto player result holds under a variety of different specifications.

Leave a Reply