When a banks’ loans begin to non-perform, they begin to eat into their capital reserves. Each banks’ Board of Directors is responsible to assess their reserves and make certain that they comply with legal and accounting requirements and, of course, they are certainly free to maintain standards that are higher than minimums.

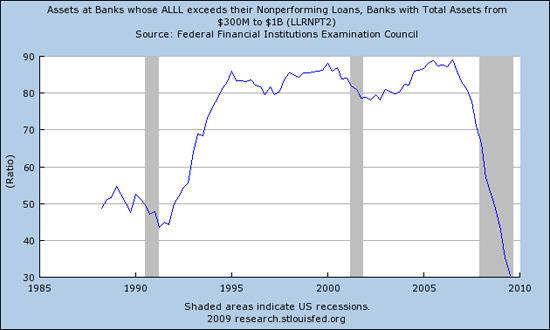

The Fed tracks the banks’ Allowance for Loan and Lease Losses (ALLL) and produces charts showing ALLL versus NONPERFORMING loans. A ratio of 100 would mean that all the banks in that size have ALLLs that exceed their nonperforming loans – a condition of health. The lower the ratio number, the less healthy the banks are for that size stratum. The banks are complaining about arbitrary rules regarding ALLL, to learn more here is an article from July of this year; Banks’ loan loss reserves are lagging behind delinquent loans (site will only let you view article once w/o login).

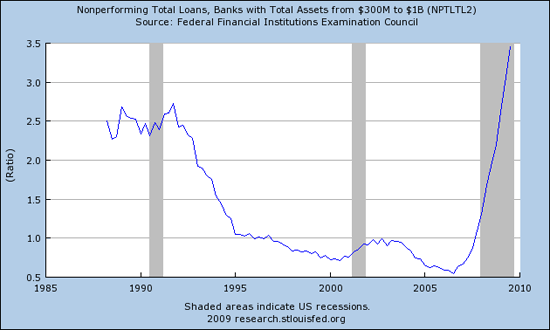

The Fed groups banks into those with ASSETS less than $300 million, those with assets $300M to $1B, those $1B to $20B, and those $20B and Higher. Of course, you and I don’t know how those “assets” are valued or by who. That’s where Enron accounting mark-to-model accounting standards come in – thus the charts below are likely indicating a false sense of health, if you can call them healthy at all. Also keep in mind that there are now millions of home owners underwater on their loans, and many commercial real estate loans are facing the same fate. As asset deflation drives prices lower, any hiccup in income drives those loans into the nonperforming category. Let’s examine the small to medium size ($300M to $1B) and the large banks above $20B…

BANKS $300M to $1B:

Nonperforming loans:

ALLL Ratio:

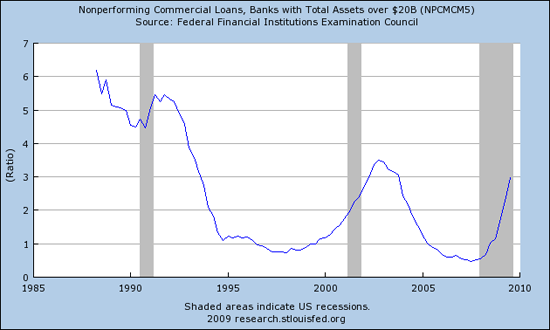

BANKS over $20B:

Nonperforming loans:

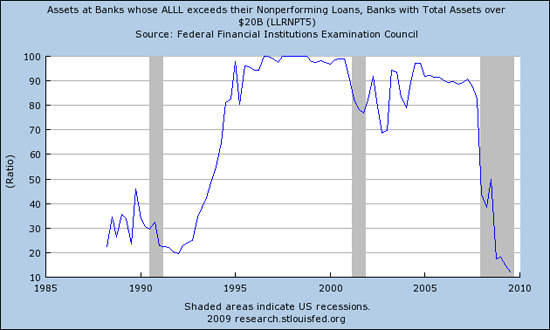

ALLL Ratio:

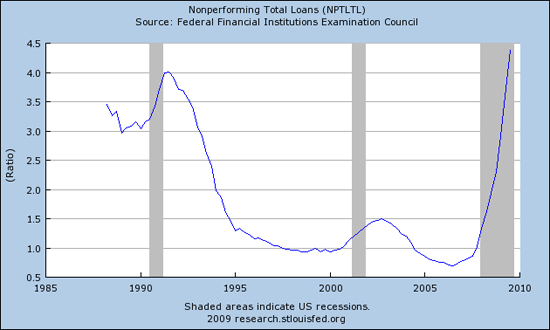

Here’s the chart of TOTAL nonperforming loans:

So, the big banks would appear to have fewer nonperforming loans, but their ALLL ratio is running around 12 while the smaller banks are up around 30. Again, I’m betting that the REAL ALLL is much, much lower due to mark-to-model, but what you’re seeing here regardless is NOT a picture of health, that’s for sure.

For more on bank capital requirements, you may want to start your research with a visit to Wikipedia – Capital Requirements.

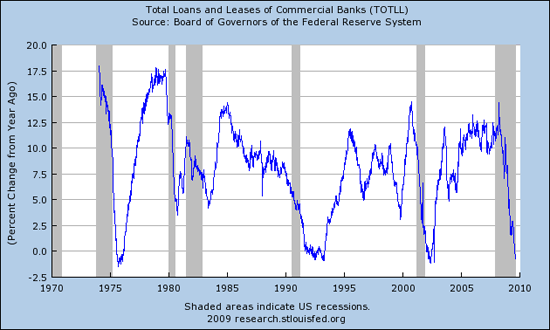

Note that the total loans and leases at all commercial banks are now negative:

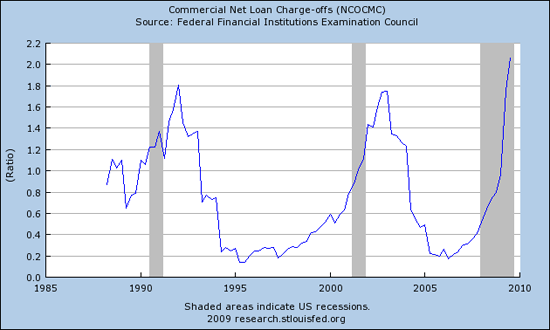

And that net commercial loan charge offs are continuing to skyrocket:

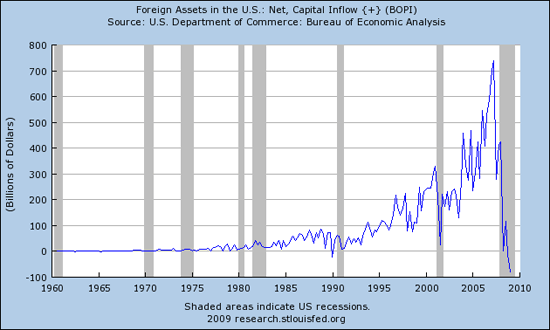

And I think the chart of the week is the chart showing net capital inflows. Is that what a loss of confidence looks like?

Here’s the St. Louis Fed’s most recent Monetary Trends Update. Note the dates in the top margin on each page to see the latest. Not a lot of change from the last couple of weeks, but I still think these charts have deflation written all over them…

—

—

So, do banks really have “excess reserves?” It seems to me that at least in relation to nonperforming loans, reserves are free fallin’…

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Wanna make alot of easy money?-own a bank!

Here is a actual bank operating in USA–$51 million capital required to open a bank–Once approved can loan 10 times= $510 million. But here is the dirty scam, Owner of the Bank gets the $51 mils from a depositor who insists on a 18% annual return.Once the bank is in operation, he demands a loan of $153 million at 7% anf I guess you can figure where the loaned money is heade–another bank. When the FDiC says not enough capital–no problem–merry go around. It is a mess folks.

The latest report from NAR is that the shadow inventory is approx. 2.4 mil. which might be low in my opinion as there are over 130 mil. households in the country. If this figure is accurate it might not be as horrible as it is only about 2% of the nations homes.