The dollar was actually up overnight… why? This would be why:

BOE More Likely to Expand Bond Purchases on GDP Slump

Oct. 23 (Bloomberg) — Britain’s failure to escape the worst recession since World War II may force the Bank of England to increase its bond-purchase plan next month, economists said.Seven months after Governor Mervyn King’s central bank started a 175 billion-pound ($287 billion) program to rescue the economy, the Office for National Statistics said today gross domestic product unexpectedly shrank 0.4 percent in the third quarter. None of the 33 economists surveyed by Bloomberg predicted a contraction.

“Having pumped in so much money and still seeing a decline in GDP is damaging from a perspective of confidence and expectations for recovery,” said Stephen King, chief global economist at HSBC Holdings Plc, in an interview with Bloomberg Television today. “They’ll be thinking very hard about whether to extend quantitative easing. They need to do something to show they care about the economy.”

That’s the problem with stimulus and printing in a nutshell. It gets bigger and bigger until doing it more hurts the economy. The world has reached that point. The sane thing to do is to stop the printing and reign in government by shrinking it dramatically. The odds of that are low, so look for QE to accelerate and for the world’s economic problems to accelerate right along with.

As I watch earnings season unfold, I am astounded at the disconnect I see from the media and the games being played with company’s reports. A never ending parade of estimate “beats” and yet all I see are HISTORIC collapses in revenue. Yes, I do see a lot of ONE TIME cost cutting measures and that is great, but it is not repeatable, and the consumer is NOT recovering. I read my former Airline’s report yesterday and see yet more and more HUGE “one time” write downs. Each and every quarter these huge write downs appear yet they do not affect “operating earnings,” LOL! This is like my family never planning on having any non-recurring expenses, you know, like having to call a plumber or fix a broken car – nope, never happens and boy do I wish that I could report that those “one time” expenses don’t affect the bottom line – they do. And yet as the size and number of these “one time” expenses grow, a pure accounting gimmick, more and more analysts are buying into the “operating” P/E numbers that are now so disconnected from reality as to be a complete and total joke.

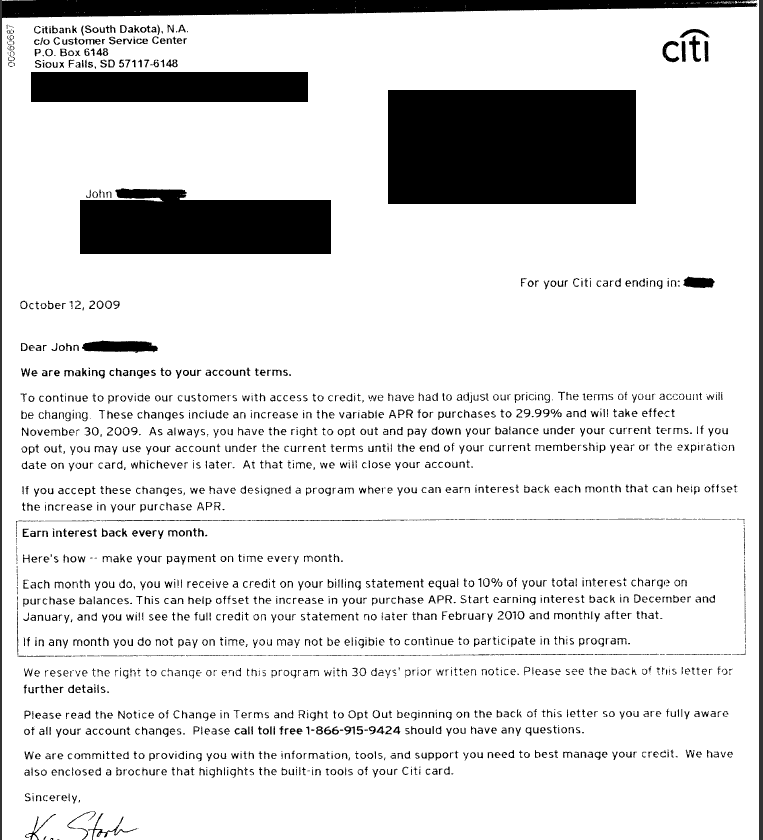

And as Wall Street complains and whines that they “won’t be able to keep their best people with pay cuts forced upon them,” WHAAAA, they turn around and RAPE the consumer, the very same ones, who through no choice of their own, were forced to bail out these bankrupt bastards. Denninger posted a notice one of his readers received from Citi Bank (C) raising their interest rate to 30%!! The Mafioso would blush at 30%! And yet, our government is bailing out firms who do this instead of rewriting USURY laws that absolutely should prevent that type of abuse. Your government is not just asleep at the switch, they are complicit in a crime against humanity, right here in our own country:

(click to enlarge)

Denninger in his article, Recovery? How, Given THIS? does the math and shows the impact on consumer spending that actions like this have.

Again, I restate my call to boycott the large banks – all of them. This country can certainly survive, and in fact THRIVE, without these big banks, they are not too big to fail, they are too big to allow them to control our money system and to control our entire political structure.

The media, on occasion, lets out little hints at the crimes being perpetrated, they are failing to do the job, again conflicts of interest are everywhere, they have permeated the fabric of our culture. What follows is a link to a story from CNN showing how little pieces of reality sneak out on occasion:

5 evil things credit card companies can (still) do

Credit card companies are socking it to consumers left and right.

They’re hiking interest rates to as much as 36% and doubling minimum monthly payments, frustrating customers who are already cash-strapped and credit-crunched.

In an effort to curb these abusive practices, President Obama signed into law a credit card reform act in May that’s rolling out in three parts over 12 months.

At the same time, credit card companies have been hard at work coming up with new ways to boost profits while sidestepping the reforms.

“Card issuers are making sure they can make up the lost money in new ways,” said Bill Hardekopf of Lowcards.com, a research company funded by a commercial debt collector.

The first part of the law, which took effect in August, requires banks to give customers more notice ahead of major changes to their accounts, like rate hikes. Starting in February, limits will be imposed on when issuers can raise rates on existing card balances, and on new cards. In August 2010 some credit card penalty fees will be will reined in.

But no legislation can fully shield consumers from the credit card industry’s ongoing efforts to boost the bottom line.

The worst part? “All of these hikes are taking place simply because they can,” Hardekopf said.

Did you see that? 36%!

Oh really? “…no legislation can fully shield consumers…” BULL, usury laws and limits on leverage can definitely protect the consumer and our entire system. The law recently passed does NOTHING. Of course those prior protections were killed by the industry who has taken over our money system.

Killing the concept of usury back in the early ‘80s allowed rates higher than 12% and that GREATLY accelerated the bad math of debt. It never should have happened and we desperately need to replace those laws as well as the Glass-Stiegel limits on leverage. Of course doing those two things would be a great start, but I must admit there is a side of me that doesn’t want to see them as I would rather see the entire system implode (it’s well on its way) so that we can properly start over, and properly identify the real roots of the problems – so far the media and the politicians are STILL not discussing the ROOTS.

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply