Uncovered interest rate parity suggests that currency returns should relate to interest rates in a pretty straightforward way. For example, the short-term interest rate in American dollars is about 0.25% and the comparable rate in Australia is 3.0%. According to the uncovered interest rate parity, the Australian dollar should depreciate against the American dollar by approximately 2.8%. Put another way, to convince an investor to invest in Australia when its currency depreciates an expected 2.8%, the Australian dollar interest rate would have to be about 2.8% higher than the American dollar interest rate.

On average, however, the high interest rate currencies actually appreciated. If you borrow in low interest rate countries, invest in high interest rate countries, you simply make more money and no one has found a risk metric that might explain this. It’s another example of the failure of the risk premium to appear where it should. Here’s Marty Eichenbaum in a short interview talking about his NBER paper on this subject.

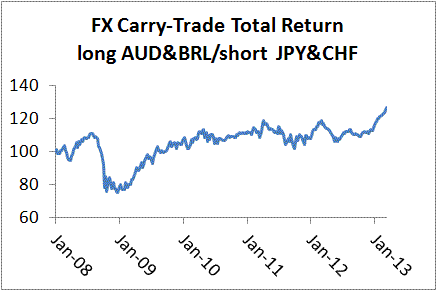

Here I’m simulating the total return to going long the Australian Dollar and Brazilian Real, short the Japanese Yen and Swiss Franc, classic high and low interest rate economies.

As one can see, this trade took a really big hit in 2008, but rebounded within a year unlike many other assets. However, since then it’s been a boring trade. This year, however, it’s been going gangbusters,so perhaps we are back to old times.

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply