Another first Friday, another employment report. Is this what our lives are meant to amount to? Sitting glassy eyed in front of a screen, clutching a cup of coffee like a life preserver, waiting for the internet to spit up some numbers that are only going to be changed next month? And to do this day, after day, after day?

Apparently, yes. And apparently I need some more coffee to drown any philosophical urges.

This is an intriguing employment report. Calculated Risk describes it as:

This was another sluggish growth employment report, but with strong upward revisions to prior months.

Mark Thoma agrees, and adds:

And “another sluggish report” ought to bring some soul-searching in Congress, followed by action to try to help with job creation (even with the prior revisions recovery is far too slow to be acceptable).

Brad DeLong adds it to his “Soft Bigotry of Low Expectations Department.” Cardiff Carcia at FT Alphaville is a bit more (modestly) optimistic:

Overall the report is (modestly) good news, showing that the economy was adding jobs at a faster rate than we thought in the final quarter of last year.

On the other hand, Wall Street cheered, sending stocks and bonds both higher. I can see that. Right now, one can imagine two threats to the current happy state of affairs on Wall Street. One is some accident, fiscal, European, war in the Middle East or whatever, take your pick, that plunges the global economy back into recession. The other is that activity accelerates such that the Fed removes accommodation earlier and faster than currently anticipated. Outcomes in between – ones that suggest the Federal Reserve will stay on its current path while at the same time growth is set to continue – seem then most likely to leave that current state of affairs in tact. And this report delivers exactly that message. Nothing here to suggest the Fed needs to accelerate its time table. Well, almost nothing.

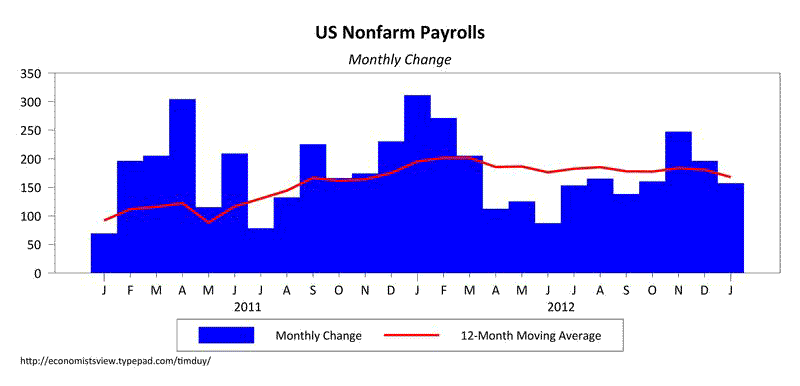

Nonfarm payrolls grew by 157k in January, a little below consensus expectations, but upward revisions pushed the November and December numbers to 247k and 196k, respectively. The twelve-month moving average is now 168k:

(click to enlarge)

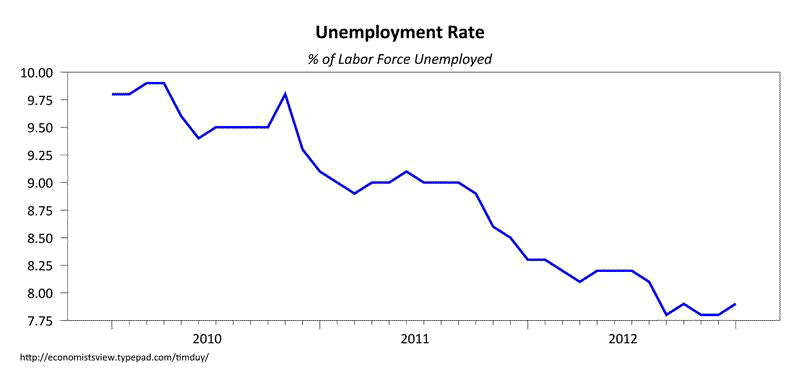

The unemployment rate edged up, even after adjusting for the population control effect:

(click to enlarge)

Consider the combination – solid if not spectacular job growth plus a stagnant unemployment rates equals a growing economy and the Fed on hold. At least, that is the message of the Evan’s rule with regards to the federal funds rate. Moreover, it is anticipated that some version of the Evan’s rule will also apply to the tapering off of asset purchases. So not only is the lift-off from the zero bound delayed, but so too is the end of asset purchases. Something for both equity and bond traders. What’s not to like?

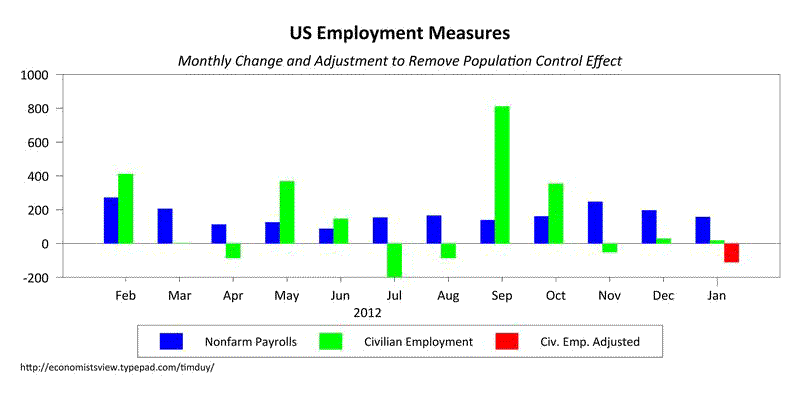

On a softer note, the employment numbers in the household report are not as rosy as those of the establishment report:

(click to enlarge)

Something to keep an eye on as a possible precursor to softening in the establishment numbers in future months.

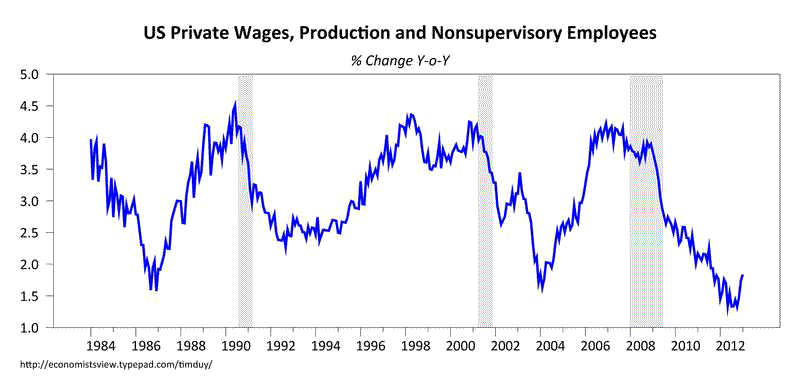

Was there anything here that might prompt the Fed to rethink policy? It’s a bit of a stretch at this point, but note that wage growth continued to accelerate:

(click to enlarge)

Like I said, a bit of a stretch. Wage growth can accelerate quite a bit (at least, in my opinion) before it becomes an inflation concern. Indeed, as Mark Thoma points out, the real problem continues to be too little inflation to begin with. For many of us, accelerating wage growth is a good thing. But look for more hawkish policymakers to point to rising wages as evidence that a.) the economy has made a solid turn such that asset purchases are no longer necessary and that b.) the Evan’s rule is faulty because one cannot adequately summarize the state of the economy in just two variables. That said, I don’t think any such noise would be enough to shift the path of policy. Just another little thing to think about.

On a final note, the ISM report came in better than expected:

(click to enlarge)

Good enough to signal the economy is not collapsing, not good enough to indicate the Fed needs to change course.

Bottom Line: To be sure, I would prefer stronger employment numbers. And I would prefer the support for those numbers came from a little more fiscal policy relative to monetary policy. But I can also see that, from the point of view of financial market participants, this can be described as a Goldilocks data day. Not too warm, not too cold. Just right.

Leave a Reply