The bottom has clearly fallen out for Apple’s (AAPL) stock price. After last week’s earnings report, the stock that had already dropped 30% from its high of $705 set in September to $500/share, dropped another 15% to finish at $440/share. The company that could do no wrong a few months ago now is viewed as incapable of doing anything right. Has the stock fallen too much or is this just the beginning of a longer term drop in value? Is it time to buy, time to sell or time to sit on your hands?

Looking at the landscape, I would categorize Apple investors and potential investors into three groups right now, based on their views of its value and the current price.

- The Pricers: As I see it, the bulk of the investors in Apple have no idea what the value of the stock is and do not care that they don’t know its value. They are intent on playing the pricing game, where the key becomes gauging what the rest of the crowd thinks about the stock and trying to get ahead of them. At any stock price, the question they ask is not whether Apple is under or over valued, but whether the price will go up or down in the near term. I have never been good at this game and it must be exhausting, being at the mercy of market sentiment, moods and fancy.

- The Value Skeptics: This group has always viewed Apple’s rapid rise to the top of the market cap heap with suspicion, convinced that its value could not have risen that fast. Some of this group belong to the hardcore value camp, where no technology company, especially one with intangible assets and an elusive “cool” factor, would be a good value, at any price. Some, though, have reasonable doubts about the capacity of technology companies to maintain earnings in an volatile environment and believe that those of us who assume long term growth prospects for these companies are under estimating the risk of the disruption from new technologies. Just as Apple undercut RIMM and Nokia, they believe that some other company will undercut Apple in the future. Many in this group are feeling self-righteous, arguing the price drop was long overdue but not enough to make the company an attractive investment yet.

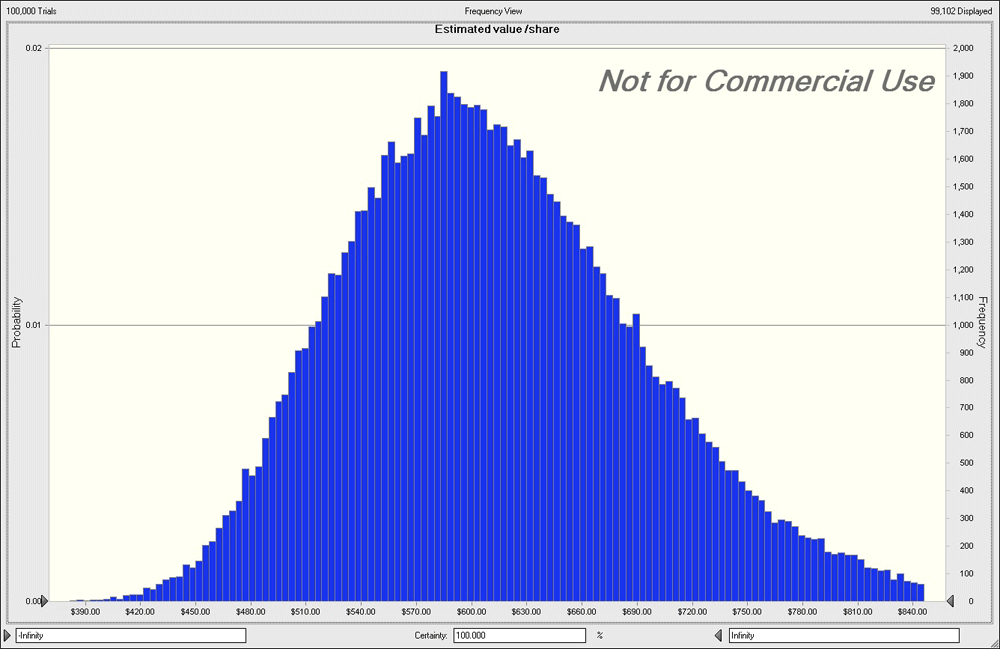

- The Value Optimists: This group believes that Apple is a bargain at $440 and that its true value is much higher. Some, in this group, base this judgment on simple comparisons. At a market cap of $413 billion, with a cash balance of $120 billion and net income of $42 billion, they note that Apple is trading at roughly seven times earnings, cheap in a market where the median PE ratio is about 16. Some are basing their views on cash flow based valuations and I am one of that group, as you probably already know from my post at the end of 2012. In that post, I valued Apple at $609/share and the latest earnings report barely changes that estimate. I did a follow up simulation, bringing in the uncertainty about my estimates about revenue growth(-2% to +14%), margins (25% to 35%) and cost of capital (11%-14%) into the mix, with the following outcomes:

(click to enlarge)

Based on my estimates, and they could be skewed by my Apple bias, at its current stock price of $440, there is a 90% chance that the stock is under valued.

If, like me, you are in this last group, you are being tested mightily now, torn between a belief that the stock is under valued and a market that does not seem to care. It is a good test of whether you are a value investor and what you do will depend upon two assessments:

- The Gut Check: Are you really a value investor or do you just like talking like one? It is easy being a contrarian value investor, in the abstract, but much more difficult to be one in practice, since you are taking a position at odds with the rest of the market. Not all investors have the stomach for that, and if you don’t, it is a good time to find out.

- The Confidence Check: How confident are you in your assessment of value? That confidence will stem from your comfort with the valuation metric/model that you used and the inputs that you used in that model, as well as from your prior experience in investing based on your valuations. Again, you cannot talk yourself into being confident, and if you are not, it is best not to take a stand.

If you pass the value investing test and feel confident in your assessment of value, I think you should take the leap. If you do, as I did (albeit at $500/share), keep the following cautionary notes in mind:

- Don’t bet the house: No matter how confident you are in your value assessment, don’t go overboard and invest a disproportionate amount of your portfolio in Apple. This is not just about you being right on the value but also about the market coming around to your point of view, and that is not in your control or mine; betting more than 10% of your portfolio on this stock strikes me as foolhardy.

- Don’t double down (Dollar averaging): I have never been a fan of dollar averaging, which not only muddies the water about when/how much you invested in a stock but results in increasing your bets as the market goes against you. Take a stand against the market but do not make this an ego trip, where admitting that you are wrong becomes impossible to do. Thus, while I feel more confident now that the stock is under valued than I was a week ago when I bought the stock for $500, I don’t plan to buy more shares.

- Think of buying the business, not the stock: The old adage that you are buying a piece of a company, not a share of stock, is particularly relevant when you make a bet like this one. My intrinsic valuation is determined by Apple’s capacity to generate profits and cash flows and is not dependent upon whether portfolio managers are investing with me or analysts are lowering their price estimates. If I buy Apple at $440 today and I can hold the stock, I will get a share of a cash that is paid out and a share of ownership in the cash that is withheld. I have to keep reminding myself of that truth, even if the market moves against me.

- Do not track the day to day stories: In an increasingly connected world, I know that this is really difficult to do, but there is no harm trying. Turn off your financial news channel, don’t read opinion stories about Apple and avoid equity research reports like the plague.

- Be willing to wait… even if you are not sure what you are waiting for: The big question that those of us who chose to make this bet face is what the catalyst will be that brings the market back to its senses (at least as we see it…). From my experience, it is almost impossible to tell. For instance, how did Netflix, which was a tailspin, a year ago, turn itself around? There was no single precipitating event but a collection of small news stories and solid earnings reports that seemed to settle the fears that investors had about the company’s future direction. With Apple, it could be a new product, a couple of healthy earnings reports or a stock buyback.

Let me close by saying that I will go to bed tonight, not thinking about what Apple’s stock price will do tomorrow or the day after. I have made my choice and I am at peace with it. If you lie awake at night thinking about the stocks you have bought or sold, you just failed the final test of value investing.

Leave a Reply