An integrated banking system saved Nevada after a local real estate boom turned to bust. Without an integrated banking system, the same wasn’t true of Ireland. This column argues that comparing Ireland and Nevada shows that banking union is far more important for Europe than current proposals of fiscal union. And, in the absence of a proper banking union that covers losses, it seems ever more likely that Europe will be pushed back towards nationally segmented financial markets.

The Eurozone crisis has demonstrated how an insolvent sovereign can destroy a national banking system, Greece, but also how an insolvent banking system can almost sink the sovereign – Ireland and Spain (Wyplosz 2012).

Localised real estate boom and bust

Local real estate booms and busts are a recurring phenomenon. The US has had its fair share, and its experience provides a useful lesson for Europe. Real booms of the last decade were very localised on both sides of the Atlantic. In the Eurozone, the overbuilding of houses on a large scale really only occurred in Spain and Ireland. Similarly, in the US, a handful of states accounted for a very large share of the subsequent losses on mortgage lending. One of these states, Nevada, is rather similar in size to Ireland.

A natural experiment

Thus, we have, by coincidence, something close to a natural experiment; two similar regions which both experience a local real estate boom and bust, but within a very different federal system.

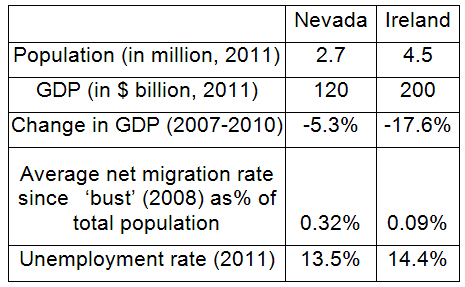

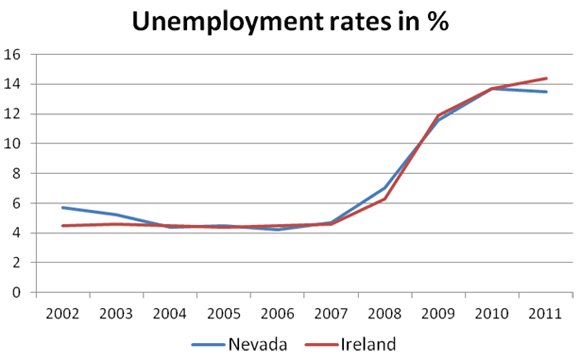

Ireland and Nevada are rather similar in several important respects (cf. Table 1). They have similar populations (2.7 to 4.5 million) and similar levels of GDP ($120-200 billion). Most importantly, they both experienced an exceptionally strong housing boom and bust. The result of the same boom-bust cycle for the real economy can be seen in the unemployment rate, which followed an almost identical pattern, as shown in Figure 1.

Table 1. Ireland and Nevada compared

Sources: Eurostat and BEA, US Census Bureau.

No bail out in Nevada

However, there is one fundamental difference between the two. When the boom turned to bust, Nevada did not experience any local financial crisis and the state government did not have to be bailed out. This might the key reason behind the large difference in the evolution of GDP, which fell much more in Ireland.

The key difference between Nevada and Ireland is that banking problems in the US are taken care of at the federal level – remember, the US is a banking union – whereas in the Eurozone, responsibility for banking losses remains national.

Local banks in Nevada experienced huge losses, just like in Ireland, and many of them became insolvent, but this did not lead to any disruption of the local banking system as these banks were seized by the Federal Deposit Insurance Corporation (FDIC), which covered the losses and transferred the operations to other, stronger banks. In 2008-09, the FDIC thus closed 11 banks headquartered in the state, with assets of over $40 billion, or about 30% of state GDP. The losses for the FDIC in these rescue/restructuring operations amounted to about $4 billion.

Figure 1. The boom/bust cycle in unemployment: Ireland vs Nevada

Sources: Eurostat and US Bureau of Labour Statistics (BLS).

Other losses were borne at the federal level when residents of Nevada defaulted in large numbers on their home mortgages. The two federal institutions that re-finance mortgages have lost between them about $8 billion in the state since 2008.

The federal institutions of the US banking union thus provided Nevada with a ‘shock absorber’ of about 10% of GDP, not in the form of loans, but in the form of an ex-post transfer. That is, losses of this magnitude were borne at the federal level. Against this transfer one would of course have to set the insurance premiums paid by banks in Nevada prior to the bust. But they are likely to have been an order of magnitude smaller.

The significance of ‘foreign banks’ in Nevada

Moreover, a lot of the banking business in Nevada was (and still is) conducted by ‘foreign’ banks, i.e. by out-of-state banks, which just took the losses from their Nevada operations on their books and could set them against profits made elsewhere1. This is another way in which an integrated banking market can provide insurance against local financial shocks. One might call this a ‘private’ banking union, or a truly integrated banking market. It is impossible to estimate the size of this additional shock absorber, but the losses absorbed by out-of-state banks might very well have been at least as large again as the ones borne by the federal institutions. The total write downs of the large US banks which operate across the entire US were about $440 billion, twice as much as the $220 billion of losses of the three official institutions (FDIC, Fannie and Freddie).

The significance of foreign banks in Europe?

In Europe, this ‘private’ banking union operates only in some cases. It is of paramount importance only for the smaller Baltic EU countries, whose banks are owned to a large extent in foreign hands. Estonia, Lithuania and, to a lesser extent, Latvia thus benefited from a similar protection against losses provided by the Scandinavian headquarters of their local banks. By contrast, most of the real estate lending in Ireland (and in Spain) had been extended mostly by local banks so that most of the losses remained local, and without any federal institution to provide insurance2.

In need of shock absorbers

The comparison between Nevada and Ireland thus illustrates the shock-absorbing capacity of an integrated banking system and a banking union. For Nevada, the banking union resulted in a transfer worth over 10%, possibly up to 20%, of its GDP.

Nevada is admittedly an extreme example of the housing boom and bust. Nevertheless, this example illustrates the general point that a banking union can provide more shock-absorbing capacity than could ever be provided by any ‘fiscal capacity’ that is currently being contemplated for the Eurozone.

‘Banking union’ is more important than a ‘fiscal union’

A first lesson is that ‘banking union’ is more important than ‘fiscal union’ in Europe. Another lesson is that the current state of integration in the Eurozone represents the worst imaginable combination:

- Any losses in the banking sector fall on the national government, which are overwhelmed when a strong local boom turns into bust.

- The euro made the wholesale liquidity and funding market cross-border, so a system-wide liquidity crisis arises whenever a local banking system becomes insolvent.

The system cannot stay as it is. Europe must either move forward to a full banking union, or it will be pushed backwards into nationally segmented financial markets. At this present moment, the tendency towards the latter is clear. Unless a more integrated system is put in place, financial integration will have to move backwards.

References

Wyplosz, Charles (2012), “The Eurozone’s May 2010 strategy is a disaster: Time to pay up and end this crisis”, VoxEU.org, 20 June.

______

1 The experience of Washington Mutual (WaMu) constitutes a somewhat special case. The biggest bank to have failed in US history, a mortgage specialist, WaMu had its headquarters in Nevada (although the name suggests otherwise) and some small operations there. However, its failure did not lead to any local losses as Washington Mutual was seized by the FDIC and its banking operations were sold for a very low sum to another large US bank (JP Morgan Chase) – but without any loss for the FDIC. Such an ‘overnight’ operation would have been impossible in Europe where no euro area wide institution would have carried through a cross border takeover of this size. Moreover, WaMu received about $80 billion in low-cost financing from the US Federal Home Loan Bank. Irish banks received massive amounts of low-cost emergency liquidity assistance from the European Central Bank, but the Central Bank of Ireland had to guarantee these loans, which was not the case for the State of Nevada for with respect to any bank in Nevada.

2 It appears, however, that the larger UK banks, like RBS had also substantial operations in Ireland where they had to write off of about 8 billion £. Unfortunately it is not possible how much resulted in actual losses and what part of any losses was incurred in the Republic of Ireland and what part in Northern Ireland.

Leave a Reply