Lat month I identified this error in the logic of St. Louis Federal Reserve President James Bullard:

Bullard also dismisses financial market distress as an artifact of the European crisis:

The global problems are clearly being driven by continued turmoil in Europe.

China might be a bigger driver than we realize, but I digress. Given that this is a European problem, the Fed is helpless:

A change in U.S. monetary policy at this juncture will not alter the situation in Europe.

This is one of those things that makes you shake your head in the wonder of it all. The point of further easing would not be to alter the situation in Europe – THE POINT IS TO PREVENT THE SITUATION IN EUROPE FROM WASHING UP ON US SHORES.

Via today’s Wall Street Journal:

Europe’s deepening economic crisis is cutting into corporate earnings, with the continent’s woes threatening to exert a drag on multinational corporations around the world into next year…

…The corporate alarm bells highlight how the miserable economic conditions in much of Europe are spilling onto the global stage. With much of Europe in recession and unemployment soaring, spending is sliding on everything from big-ticket items like cars to everyday staples like yogurt…

…Companies also are growing concerned about 2013 as government austerity measures eat into sales. The Ifo Institute survey of business sentiment released on Wednesday shows business confidence in Germany, Europe’s largest economy, falling to its lowest level in over two years.

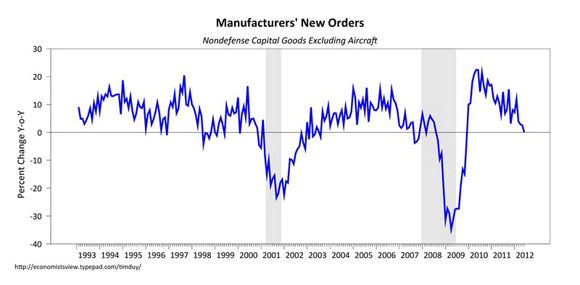

And note the trend in capital goods orders:

Flat growth year-over-year. Not necessarily a recession, but a clear warning sign as well. It is starting to look like firms satisfied their pent-up demand and don’t see the underlying growth that justifies further spending. And clearly Europe is only aggravating that situation.

The recent softness in manufacturing is a warning sign that usually prompts Fed easing. That might be next week, or next month – there remains considerable uncertainty on the timing of their next move. But one thing is looking more certain day by day: The Fed should have been hitting their own panic button six weeks ago when it became clear their forecasts were well off the mark.

Leave a Reply