Instead of the definitive report we were hoping for, we got a remarkably unhelpful report. On the margin, it points to additional easing. But I can’t say it strongly points in that direction. It simply was neither bad enough or good enough to clear up any uncertainty about the impact of seasonal distortions in the data. And thus, it really should be generally neutral, at least on the basis of where the Fed appears to be sitting. Of course, I would argue that the Fed is sitting in the wrong place to begin with, and should already be easing further. But that is another story for another time.

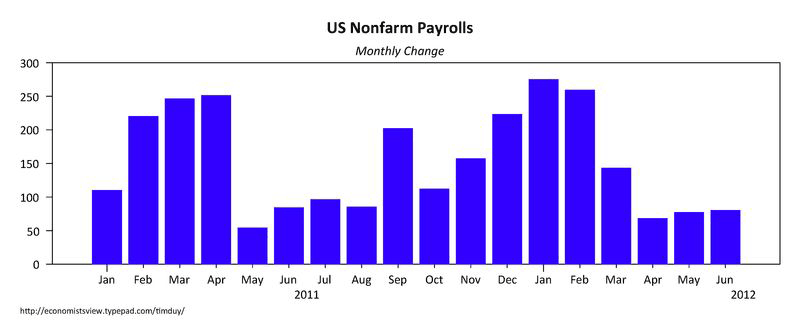

The basics of the report are well known at this point. Nonfarm payrolls eked out a meager gain of just 80k while the unemployment rate held steady at 8.2%. The nonfarm payroll numbers continued to exhibit the trends we saw last year:

(click to enlarge)

I think Cardiff Garcia is on the right track when he says:

… we find the relationship between the seasonal shifts the past three years in these economic surprise readings to be a little too close to be all coincidence.

The Federal Reserve is struggling with this same question. While the average gain over the past 3 months is just 75k, the average over the past 6 and 12 months is about 150k. Arguably, 150k is not enough given the depth of the recession, and thus in and of itself calls for further action. But the Fed doesn’t seem to think so, otherwise they would have engaged in more easing already. Which leads me to believe that while on the margin the headline numbers in this report suggest additional Fed easing, if the Fed choose to look through the possible seasonal distortions and see the longer term moving averages, they will not be inclined to act on this report.

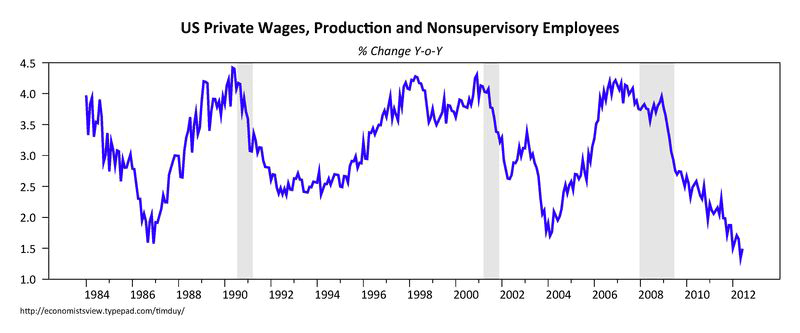

If I look for good news in the employment report, I see a hint in the 5 cent/hour wage gain. That said, the long term trend looks pretty dismal still:

(click to enlarge)

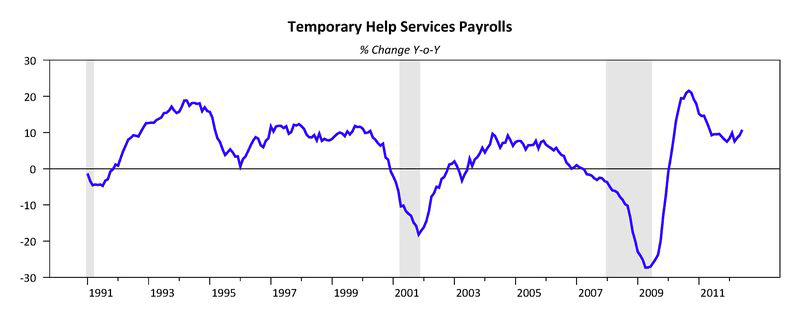

I know I should be hoping for wages growth to accelerate, but I worry the Fed will turn hawkish at the first hint of higher wages. I guess we will cross that bridge when we get to it. The uptick in temporary hiring is also a plus:

(click to enlarge)

Still, I admit that I am putting a little lipstick on the pig by looking for the good news. Maybe a lot of lipstick. This was a pretty weak report.

In other news, MarketWatch reports that retail spending softened in June:

Total June sales at stores open at least a year — a key performance metric that strips out the impact of new and closed stores — rose 0.1%, missing the 0.5% gain Wall Street was looking for. That was the smallest pace since sales declined in August 2009, according to Thomson Reuters. Sales rose 6.7% a year earlier.

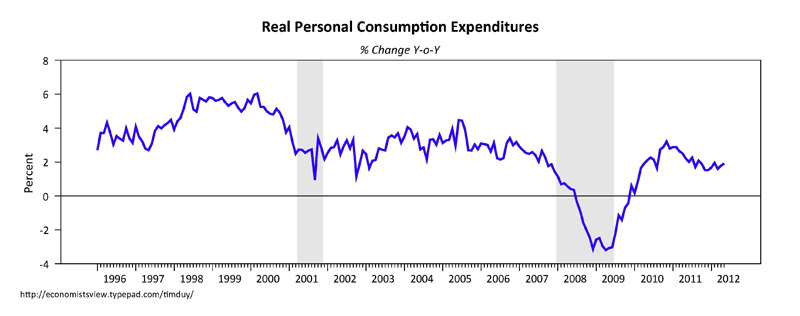

Which fits with the relative deceleration in the real consumer spending over the past year:

(click to enlarge)

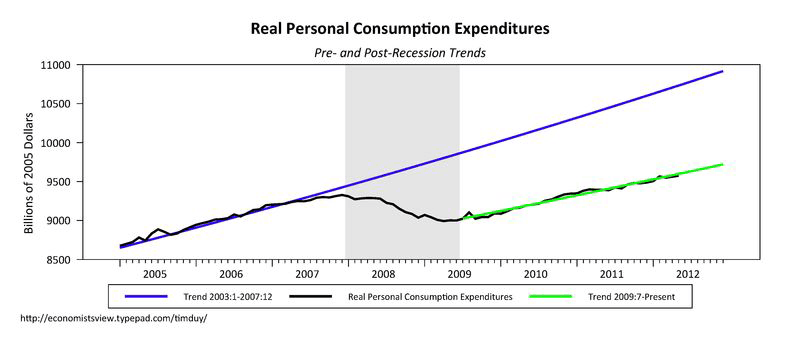

Looking at the the path in levels, it is obvious that consumer spending remains in a whole different world compared to the pre-recession period:

(click to enlarge)

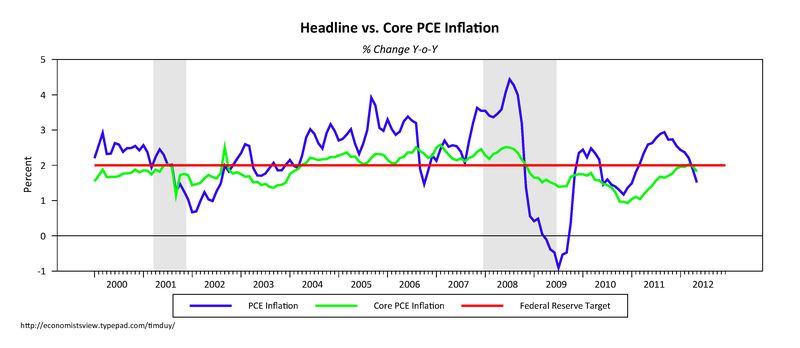

Not exactly a bullish trend, but one that is not new either. As such, it is challenging to expect the Fed will react. A trend that should change Fed thinking, however, is the direction of inflation:

(click to enlarge)

Headline inflation clearly rolled over, and we are seeing the first hints falling core inflation will confirm this move. This should be critical. Even if the Fed concludes that the employment report is inconclusive, a deteriorating inflation outlook should be a clear signal that the Fed has more work to do. After all, what is the point of setting an inflation target if you have no intention of trying to hit it?

Bottom Line: I continue to believe that neither an optimist not a pessimism should one be when assessing the path of economic activity in the US. Sticking by this rule would lead you to discount the last three employment reports as seasonally distorted, while also discounting the string of positive reports we saw earlier this year. That still leaves an underlying jobs growth rate that is uninspiring in comparison to the job market damage done by the recession. Combine that with a deteriorating inflation outlook, add in a dash of supposed dual-mandate, and you should have the recipe for an additional dose of quantitative easing. Yet I still fear such expectations are premature given what appears to be a relatively high bar for QE3. Yes, I see clear reason for Fed action given Fed forecasts, the evolution, and the Fedspeak of supposedly key members. But I have seen this for months, and the Fed has consistently failed to meet expectations. With the employment report failing to provide a conclusive policy direction, it is increasingly likely the next meeting is another nailbiter. Outcome still in flux.

Leave a Reply