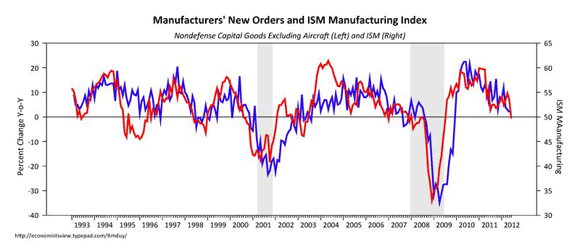

Josh Lehner and Bill McBride note that the manufacturing slowdown does not necessarily indicate recession, something I noted as well. Another version of that story is seen by comparing the ISM headline number with the new orders data:

Again, manufacturing slowdowns in 1995 and 1998 did not presage recessions (albeit possibly due to offsetting monetary policy). McBride reiterates that housing is a better leading indicator than manufacturing, and Lehner discusses a “tradeoff” from manufacturing to housing.

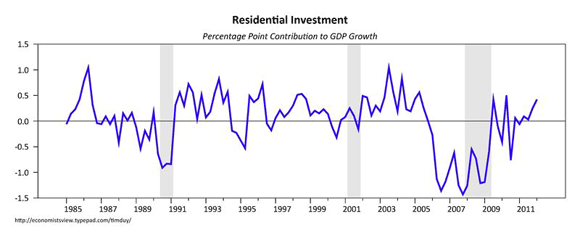

For my part, I am wondering what people expect when they talk about a housing recovery. I tend to break the housing story into two parts. One is the residential construction story, the activity that amounts to screwing sticks of wood onto slabs of concrete. The related contribution to GDP growth since 1985:

During the 2002-2005 period, arguably the height of the housing bubble, residential construction contributed an average of 0.4 percentage points to GDP growth each quarter. In the first quarter of this year, the contribution was 0.42 percentage points. So, barring the occasional pop in the data, housing is already contributing to GDP growth about what we would expect.

Presumably, we would be hoping that as the housing rebound deepens, there will be secondary impacts. For this reason I am hesitant to embrace the “tradeoff” terminology. Certainly we can envision accelerated home building triggering an increase in both manufacturing (capital equipment) and consumer (job/income growth) activity as well; these tend to be interconnected activities. So maybe the overall impact is a bit higher.

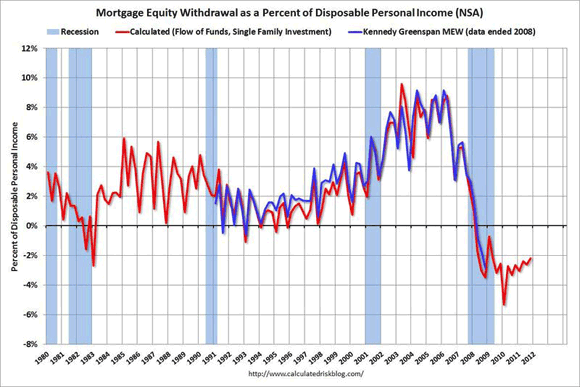

That said, there is another element to the housing story – the household balance sheet issue. Arguably, as Karl Smith has said, the housing bubble was less about a construction bubble (again, note the relatively limited contribution to GDP growth; we didn’t necessarily build too many units, especially given the subsequent construction drought), and more about a price bubble. And that price bubble fueled spending activity via mortgage equity withdrawal. The chart via Bill McBride:

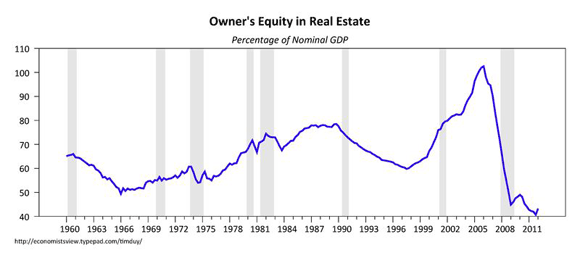

Of course, equity withdrawal has collapsed because equity as collapsed:

So here is the question: What was more important in holding the economy close to potential output, residential construction itself, or the housing price bubble? I tend to believe the price-driven balance sheet effects were driving dynamics over this past business cycle. Absent a healing of household balance sheets (or, relatedly, monetary policy that supported such healing via somewhat higher inflation expectations to reduce debt in real terms), I would expect overall growth to remain subdued, despite a rebound in residential construction. The latter is helpful and important, but not by itself a magic bullet.

Leave a Reply