Finding reliable indicators that predict the likelihood and severity of crises across countries has been a frustrating quest for economists. This column suggests that countries with better creditor protection suffer less when a crisis hits.

The effects of the current financial crisis were felt unevenly around the globe and it is time for us to think about the reasons why some countries were hit harder than others.

In their most recent paper, Spiegel and Rose (2009) show that most commonly used factors do not help explain the incidence of crises across countries. We look, therefore, for institutional causes.

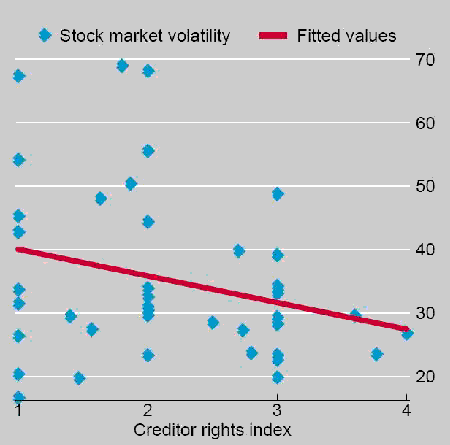

In recent research (Hale, Razin, and Tong 2009), we show that stock market volatility has been historically correlated with the degree of creditor protection – the better creditor protection, the lower the stock market volatility. Specifically, using the time-varying creditor rights index compiled by Djankov et al. (2007) for 49 countries over the 27 years preceding the current crisis, we find that on average the volatility of annual real stock returns is 24% lower in countries with better creditor protection. This relationship is illustrated in Figure 1.

Figure 1. Stock market volatility and creditor protection

In order to understand the mechanism behind this relationship, we propose a Tobin’s q model with collateral constraints and liquidity shocks. The intuition is that creditor protection relaxes collateral constraints because it makes it easier for creditors to recover their investment in case of borrower failure. As a result, countries with strong creditor protection will find themselves in a situation with constrained credit only if relatively large liquidity shocks hit their economies, while countries with weak creditor protection will find themselves in a credit-constrained situation, where equity demand falls sharply, even when hit by smaller liquidity shocks.

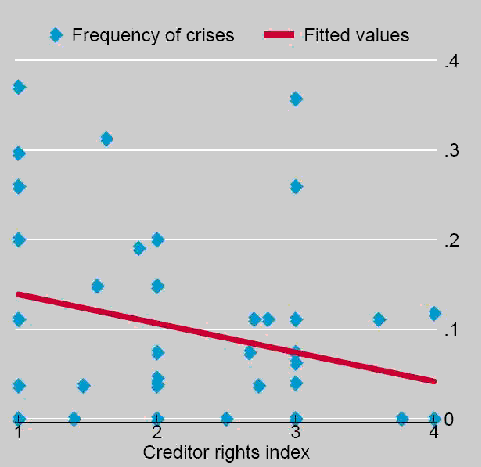

Consistent with the model’s predictions, we find that countries with higher level of creditor rights protection are less likely to experience liquidity crises (defined as a sharp decline in bank lending to the private sector), as illustrated in Figure 2. Notably, this relationship also holds in the subsets of OECD and non-OECD countries. In addition, as the model predicts, the decline in stock market returns tends to be larger during liquidity crises in countries with lower creditor rights protection.

Figure 2. Crisis and creditor protection

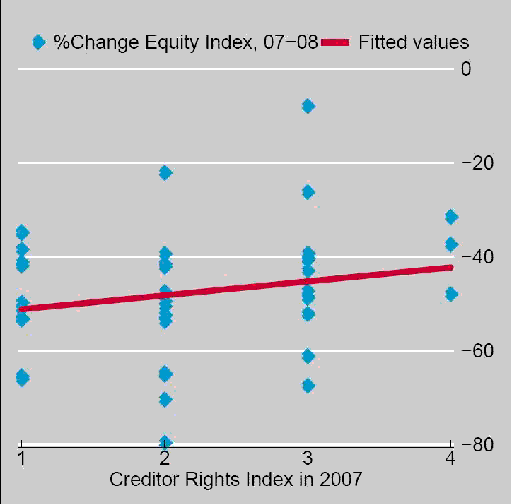

The mechanism described above has a stark implication for the effects of a current crisis. Supposing that all countries were hit by the same liquidity shock, we should expect countries with strong creditor protection to experience smaller declines in their stock indices during the crisis. Indeed, as Figure 3 shows, we find that average decline in the stock market index between December 31, 2007 and December 31, 2008 was less in countries that had a higher value of creditor rights index in 2007.

Figure 3. The current crisis and creditor protection

We do not claim that creditor protection alone can ultimately prevent or lessen the impact of liquidity crises. Nevertheless, we are convinced that its shielding effect on the stock prices is an important argument for stronger creditor protection. As the current crisis has demonstrated, countries with strong creditor rights protection fared better, at least in terms of their stock market performance, than countries with weak creditor.

References

•Djankov, Simeon, Caralee McLiesh, and Andrei Shleifer (2007), “Private Credit in 129 countries,” Journal of Financial Economics, 84(2), 299-329.

•Hale, Galina, Assaf Razin, and Hui Tong (2009), “The Impact of Creditor Protection on Stock Prices in the Presence of Credit Crunch,” CEPR Discussion Paper No. DP7357.

•Rose, Andrew K. and Mark M. Spiegel, (2009), “Cross-Country Causes and Consequences of the 2008 Crisis: Early Warning,” CEPR Discussion Paper 7354, and “Could an early warning system have predicted the crisis?” VoxEU.org, 3 Aug.

![]()

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply