I stole the title of this post from a PowerPoint slide that Lars Christensen sent me. Perhaps there’s a bit of hyperbole there, but it reminded me of my research on the Great Depression. During 1931 all the Very Serious People were obsessed with the debt crisis. In some mysterious way they believed this was a major cause of the Depression itself. I’m not sure why, I think it had something to do with “confidence.” Interestingly, the debt crisis never really got resolved. Instead it just gradually faded away as an issue, as by late 1932 it was becoming increasingly clear that intergovernmental debts were not going to be repaid. And as the debt crisis receded, people discovered that the Great Depression was still there.

Of course you all know the rest of the story. One by one countries discovered that the real problem was monetary, and recovery didn’t start in a country until it had abandoned the gold peg and started boosting NGDP rapidly.

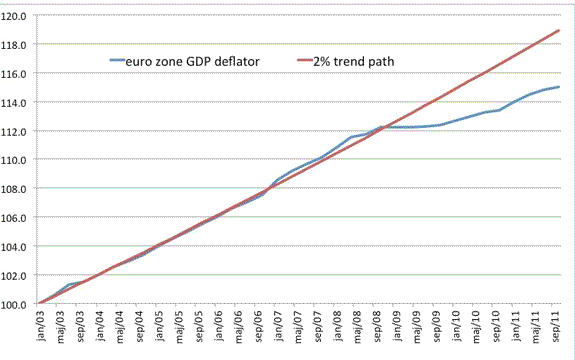

Some argue that the ECB cannot inflate, that it must keep targeting inflation at 2%, or else lose credibility. But they aren’t even doing a very good job in targeting inflation. You’d think that a central bank would be interested in the overall rate of inflation, not just those goods in the CPI. After all, no matter how dumb central bankers may seem, they certainly don’t believe that low and stable inflation is good because it holds down the cost of living to consumers. They actually do know about the circular flow of income/expenditure. The standard view among economists is that low and stable inflation reduces menu costs and helps stabilize output. Of course in both cases you’d do better with a price index that covered all goods, not just those in the CPI. And as Lars showed in this new post, they aren’t even coming close to hitting their 2% target for inflation, if we define inflation to include all goods. Indeed since September 2008 they aren’t even hitting a 1% inflation target.

Some might argue that the ECB is targeting a different index, and that they must stick with this failed policy in order to avoid losing credibility. It reminds me of how in the Vietnam War the US military would sometimes claim that they had to destroy a village in order to save it. The ECB will destroy much of the eurozone economy in order to save it. And in the end they’ll lose anyway, as politics always gets the last word.

PS. Just to be clear, there are debt problems in Europe. But Wall Street isn’t falling on Greek news because of the debt issue, rather it reflects a lack of confidence in the Fed’s willingness to keep NGDP growing at a healthy rate.

Leave a Reply