The minutes of the most recent Federal Reserve meeting were not exactly what one would call a page turner. Much of the contents had already been covered in recent speeches to varying degrees, culminating with an unexpectedly sanguine view of the economy:

With respect to the economic outlook, participants generally saw the intermeeting news as suggesting that economic growth over coming quarters would continue to be moderate and that the unemployment rate would decline gradually toward levels that the Committee judges to be consistent with its dual mandate. While a few participants indicated that their expectations for real GDP growth for 2012 had risen somewhat, most participants did not interpret the recent economic and financial information as pointing to a material revision to the outlook for 2013 and 2014.

The recent flow of data has done little to alter the Fed’s basic outlook that the recovery will continue to grind along at a pace slower than hoped for but fast enough such that no additional easing is required. And on the prices side of the equation, inflation expectations remain anchored, and any pass-through from higher oil and gas prices will be temporary. As expected, some participants were concerned about inflation prospects:

One participant pointed to inflation readings and a high rate of long-duration unemployment as signs that the current level of output may be much closer to potential than had been thought, and a few others cited a weaker path of potential output as a characteristic of the present expansion.

These concerns, however, were largely dismissed by the rest of the committee:

However, a number of participants judged that the labor market currently featured substantial slack. In support of that view, various indicators were cited, including aggregate hours, which during the recession had exhibited a decline that was particularly severe by historical standards and remained well below the series’ pre-recession peak; the high number of persons working part time for economic reasons; and low ratios of job openings to unemployment and of employment to population.

Not to be deterred so easily, the hawks come back later with:

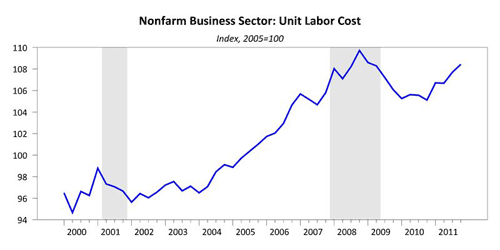

A couple of participants noted that recent readings on unit labor costs had shown a larger increase than earlier…

That picture looks like this:

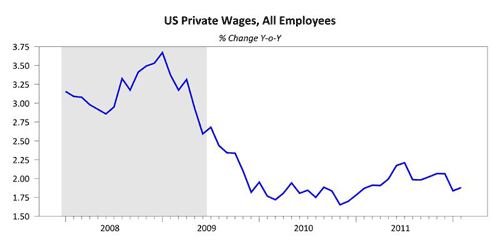

Heaven forbid we allow any catch-up in unit labor costs. In any event, I would be cautious about reading too much into the most recent data given weak wage growth:

Which is the same conclusion other the participates in the meeting:

…but other participants pointed to other measures of labor compensation that continued to show modest increases.

The hawks do make one last effort:

Other participants, however, were worried that inflation pressures could increase as the expansion continued; these participants argued that, particularly in light of the recent rise in oil and gasoline prices, maintaining the current highly accommodative stance of monetary policy over the medium run could erode the stability of inflation expectations and risk higher inflation.

This despite the experience of last year where the same arguments were made and ultimately proved wrong.

Finally, if you were looking for signs that another round of QE, your hopes were dashed:

A couple of members indicated that the initiation of additional stimulus could become necessary if the economy lost momentum or if inflation seemed likely to remain below its mandate-consistent rate of 2 percent over the medium run.

A half-hearted call for additional easing at best. The Fed is simply not inclined to overshoot. As Mark Thoma points outs, the best we get is a signal that the Fed is not ready to pull the trigger on tighter policy.

Bottom Line: The Fed remains in a holding pattern; more QE is dependent upon a meaningful deterioration in the outlook and/or a flattening out of the unemployment rate. Otherwise, it remains a debate about when the first tightening will occur, and for the moment that event is still far in the future.

Leave a Reply