In his July 13 testimony to Congress, Federal Reserve Chairman Ben Bernanke discussed the large-scale asset purchase program to buy $600 billion of longer-term Treasury securities that started in November 2010 and was completed in June 2011. The chairman noted:

“The Federal Reserve’s acquisition of longer-term Treasury securities boosted the prices of such securities and caused longer-term Treasury yields to be lower than they would have been otherwise. In addition, by removing substantial quantities of longer-term Treasury securities from the market, the Fed’s purchases induced private investors to acquire other assets that serve as substitutes for Treasury securities in the financial marketplace, such as corporate bonds and mortgage-backed securities. By this means, the Fed’s asset purchase program—like more conventional monetary policy—has served to reduce the yields and increase the prices of those other assets as well. The net result of these actions is lower borrowing costs and easier financial conditions throughout the economy.”

Chairman Bernanke went on to observe in a footnote in his prepared remarks from that testimony:

“The Federal Reserve’s recently completed securities purchase program has changed the average maturity of Treasury securities held by the public only modestly, suggesting that such an effect likely did not contribute substantially to the reduction in Treasury yields. Rather, the more important channel of effect was the removal of Treasury securities from the market, which reduced Treasury yields generally while inducing private investors to hold alternative assets (the portfolio reallocation effect). The substitution into alternative assets raised their prices and lowered their yields, easing overall financial conditions.”

In a similar way, the maturity extension program—dubbed “Operation Twist” by some—announced by the Federal Open Market Committee last week is designed to further remove longer-term Treasury securities from the market, a move that, other things being equal, should put downward pressure on longer-term rates. Jim Hamilton at Econbrowser has taken a stab at estimating the effects and concludes that it is likely to be modest. Atlanta Fed President Dennis Lockhart shared a similar sentiment, described in more detail later in this posting, in a speech earlier this week.

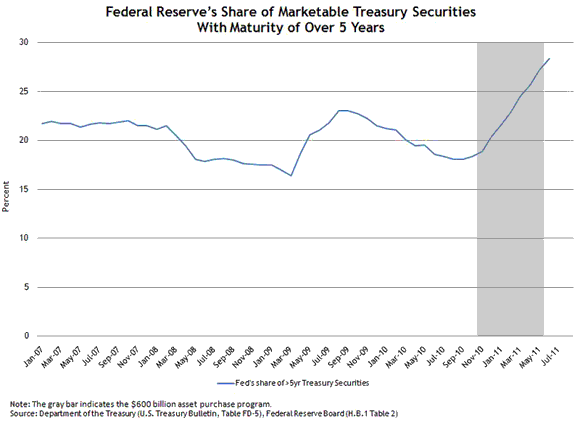

So what share of outstanding marketable long-term Treasury securities (excluding those held to maturity on government accounts) does the Federal Reserve hold? The following chart shows that the Fed’s share of marketable long-term securities with more than five years to maturity increased substantially as a result of the $600 billion asset purchase program between November 2010 and June 2011 (see the chart). This large run-up confirms the point made by Chairman Bernanke that this program removed a considerable supply of longer-term securities from the market (relative to what it would have been otherwise).

The new maturity extension program will replace $400 billion of shorter-dated Treasury securities that the Fed holds with an equal face-value amount of longer-term securities, and this move will further increase the Fed’s relative holdings of marketable longer-term Treasury securities. As President Lockhart noted in his speech, the impact of this program cannot be known precisely, but he expects it to have a modest, positive influence:

“The Fed’s maturity extension program and additional mortgage-backed securities purchases are meant to further ease financial conditions ceteris paribus, other things being equal. Of course, other things almost certainly will not stay equal, and other factors will influence what really happens to rates and spreads as policy intent encounters the real world….

“In my view, the maturity extension program along with the MBS purchases represents a measured, incremental attempt to add more support to the recovery. It’s not a fix for everything that ails the economy, but it should help.”

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply