The blogoshpere witnessed some additional contributions to the output gap debate this weekend. Greg Ip offers up the possibility that potential output, both level and trend, are much lower than previously imagined. Karl Smith responds with what I believe is an important point:

I’d, however, encourage everyone, as well, to think of the disaggregated story that we are telling here. If trend GDP is overstated, then we are arguing that one or more sectors of the US economy will is less capable of producing output over the next decade or so, than we would have otherwise thought.

Smith suggests we focus on the construction of housing, hospitals and medical facilities, public infrastructure, and transportation equipment. He concludes:

So, if we think these things will repair themselves then we have an obvious path back to trend.

and then extends:

I don’t want to get too invested in this but a cursory look at the data suggests that GDP is likely to grow above trend in the coming years because two very high productivity export sectors are expanding – computers and gasoline and distillates.

What I like in Smith is the more careful consideration of the structural change story. If we claim the economic potential of the nation has declined – that in aggregate, we can not make as much stuff as we did a few years ago – we need to identify what stuff isn’t being made, why it isn’t being made, why we don’t think it should be made, and why no other sectors are growing to compensate for those in decline.

Mark Thoma makes an important contribution to the debate by identifying a short-run path for potential output:

Even a standard business cycle type AD shock will temporarily depress capacity and produce similar effects. Suppose that interest rates go up, taxes go up, government spending goes down, investment falls –pick your story — causing aggregate demand to fall. When, as a result, businesses lay people off, idle equipment, etc., productive capacity will fall. It can be cranked up again, and will be when the economy recovers, but rehiring labor and taking equipment out of mothballs takes time. In the interim the natural rate of output falls and, just as with a change in the preference for good A versus good B, a negative aggregate demand shock can cause “frictions” on the supply side that temporarily increase the natural rate of unemployment. And there are many other ways this can happen as well.

Mark notes, however, that policy makers should not focus too intensely on short-run potential output because capacity will grow as the economy recovers. In other, don’t confuse a temporary decline in potential with a permanent decline. Mark extends this to an explanation for relatively stable inflation during the recession.

That said, Ip does note that a permanent – or at least very persistent – drop in labor force participation rates could cause at least some downward shift in potential output, with a story that in aggregate we cannot make as much as before because we lack sufficient labor, although here too there should be sector specific impacts similar to Smith’s critique (unless all sectors lost access to a more or less proportionate share of labor). And Ip also raises the somewhat different issue of the path of potential output going forward – a decline in both productivity and labor force growth implies a lower path forward, although would not explain a sharp drop in the past.

Finally, I find Felix Salmon’s explanation for fall in potential GDP less compelling:

In other words, in order to keep up a steady rate of GDP growth, we had to saddle ourselves with ever more cheap and dangerous debt.

Then, suddenly, the growth of the credit markets screeched to a halt, and we had a major recession. And since then, the size of the credit market has been roughly flat.

It makes sense that if we needed ever-increasing amounts of debt to keep up that long-term GDP growth rate, then when the growth of the debt market stops, our potential growth rate might fall significantly.

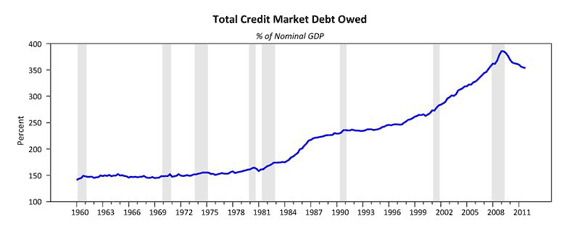

Salmon is telling a story about this chart (although he actually uses what I believe is a more difficult chart):

Smith responds by noting this is really a story about mortgage debt, with the first run-up being a natural consequence of the Volker Disinflation and the second being the housing bubble, which Smith views as largely an internal transfer of wealth.

My additional criticisms of Salmon approach is that is seems primarily a demand side story to a supply-side question. Presumably, all of the productive resources (or nearly all of them, allowing for some hysteresis effects) still exist. The debt is just plumbing in the background that helps support the demand for those resources. So Salmon’s story just collapses down to an aggregate demand shortfall that really has nothing to do with potential output.

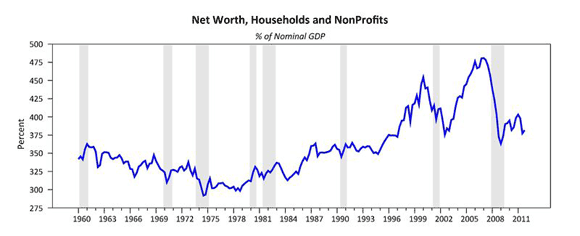

Moreover, Salmon ignores the assets on the other side of the debt. We really need to look at some story about net worth:

Here again I think you are fundamentally telling a demand side story to explain the past two business cycles – both were dependent on asset price bubbles to hold output at potential (or even slightly above at the peaks). Why did the US become dependent on these bubbles? Here I tend to find the global saving glut story compelling. A combination of aging developed economies combined with the high savings propensities of primarily Asian central banks has pushed the equilibrium real rate into negative territory, below that attainable given the zero bound and low inflation expectations. Absent an asset bubble to compensate by adding wealth-effect induced aggregate demand, we are left with a savings-investment imbalance that becomes evident as a subpar equilibrium level of output.

I still believe that primarily we are looking at an aggregate demand shortfall rather than a collapse of potential output, but would agree that only one thing is for sure: That we haven’t seen the end of this debate.

Leave a Reply