Here is a follow up to my previous blog entry on the meaning of gross debt. Paul Krugman thinks that I went too far when I argued that there is no need to worry about gross debt. Correct. But my goal was not to argue that gross debt is completely irrelevant but to raise my concerns about those who only look at the liability side of a balance sheet or ignore the fact that what constitute a liability for some it is an asset for someone else (a point that Paul Krugman has made earlier when referring to government debt).

This does not mean that gross debt does not contain any important information. For example, if we think about the world, a consolidation of all balance sheets leads to an always perfectly match between revenues and spending, the world cannot accumulate any debt. But when we look at a disaggregated level, individual countries run deficits and this can be a source of concern and instability. Same is true for a country. Japan runs a surplus on the current account (accumulates assets, not debt) but its government keeps increasing its debt. The country as a whole does not need to deleverage and looking at the gross debt of the country is a meaningless exercise (the point I made in my previous entry). But the government needs to find a way to reduce or stabilize their debt so looking a disaggregated data is necessary as well.

Back to the US, Paul Krugman has a new post on the behavior of debt over the last two bubbles. Comparing the Clinton years where there was a stock bubble and the Bush years where there was a real estate bubble he concludes that there are large differences between the two. Not only the economy did much better during the Clinton years, but also the accumulation of debt was much worse during the Bush years. He is completely right on his assessment. But just to understand better what happened during those years, what was the behavior of net wealth (and not just debt) during each of the two episodes?

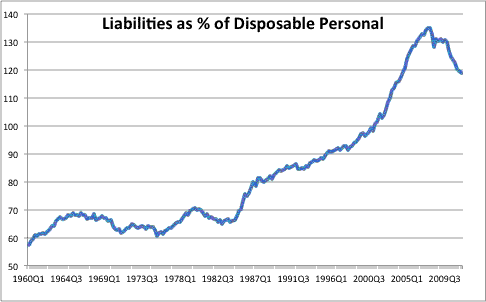

Using data from the Flow of Funds accounts (US Federal Reserve) I have plotted below the liabilities of US households as a % of their personal disposable income. I went back to 1960 to get a better historical perspective.

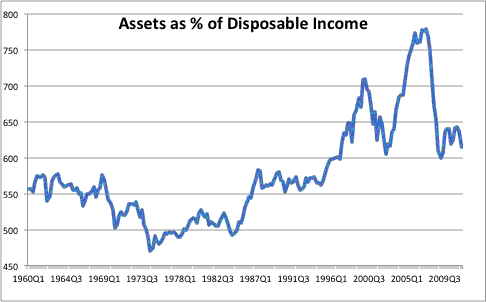

This first chart confirms Krugman’s assessment that the increase in debt was significantly faster during the second bubble (post 2001). But what was going on at the same time with the value of the assets that the households were buying? The value of assets increased during those episodes and it increased much faster during the second bubble.

This is not a surprise given how widespread the bubble in housing prices was and how relevant housing is in terms of the wealth of US households.

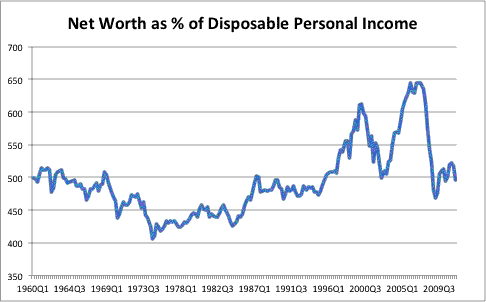

Here comes the most interesting chart (from my point of view), the one that combines assets and liabilities and looks at the net wealth (again measured as % of personal disposable income).

First lessons is how remarkably stable this ratio has been over the last 50 years. It was around 500% in the 60s, was depressed during the 70s (around 450%) as these were years with very weak stock and housing markets. It went back to 500% during the 80s and then we see very clearly the two bubbles bringing this ratio to 600 or 650% before it collapses back to 500%.

When we look at the two bubbles from this lens we see that in both cases the accumulation of debt during the good years of the bubble was happening while the balance sheets of households were getting stronger and stronger. The valuation of assets always grew faster than the accumulation of debt (and this made the bubble look “reasonable” to some). When the bubble bursts, assets go back to normal but what it is interesting is that net wealth does not collapse; it simply returns to the pre-bubble levels. This means that despite the increase in debt if you compare post- to pre-bubble years (first chart), households are back to the level of wealth they had before the bubble started. Yes, my mortgage is much bigger than it used to be but I also own my house and stocks that are worth more than they use to. To be clear, relative to the peak of the bubble I am of course much worse off, but relative to the day the bubble started, I am in a similar position.

If we look at the balance sheet of households in the US through this lens we might reach the conclusion that there is not much need to deleverage. The consolidated balance sheet looks the same as it looked during early decades (the 60s or the 80s). Higher debt simply matches the assets the have been bought with it. We can think of scenarios where the health of the balance sheet looked much worse than before: Supposed all the borrowing during the boom years had used to pay for additional vacations or expensive meals. Then the picture today would look very different, net wealth would look so much lower than in the pre-bubble years and we would be talking about a much weaker situation as seen by the balance sheet of households.

Some caveats to what it might sound like a too optimistic look at the financial health of US households. The 500% ratio that has been stable over time might not be the right level. I am just claiming that we are at a level that is similar to what we have seen in “normal” years. I cannot claim that this is good or optimal or that there should not be a positive trend in this ratio. The second caveat is that the picture above ignores distributional issues. The fact that the aggregate looks good does no mean that we do not have a significant proportion of the population with balance sheets that look much weaker and this is a concern. Finally, the valuation of assets might still fall further (housing prices) and could send net wealth to lower levels.

Leave a Reply