Lots of people have argued that easy money contributed to the housing bubble. I mostly disagree, as money wasn’t particularly easy. Just to be clear, I’m not denying that a couple points of the increase might have been caused by faster than 5% NGDP growth around 2004-06, but growth in NGDP wasn’t that unusual, and we didn’t see national housing bubbles in other decades.

But almost no one argues that tight money caused the bubble. Indeed you could probably remove “almost” from the previous sentence. Since I like nothing more than a challenge, I’ll make that argument. More precisely, I’ll argue that it caused a portion of the bubble, perhaps one half.

Next we have to discuss what we mean by ‘bubble.’ Most people mean a sharp rise in prices, followed by a big decline. I agree with most people. More sophisticated people define ‘bubbles’ in terms of market inefficiency, deviation from the EMH. Since I believe markets are efficient, that’s obviously not my definition, or else I’d have to argue that bubbles don’t exist. So let’s stick with the conventional definition.

In my view there is too much focus on the upswing part of bubbles. Housing prices also soared in the 1970s, but no one called that a bubble. The price of Microsoft stock soared in the 1990s, but that wasn’t a bubble either (except perhaps in 2000). Why not? Because prices didn’t collapse afterward. Housing prices kept rising in the 1980s, and while Microsoft stock has bounced around, it’s always maintained a pretty high market cap. To have a bubble you need a big rise followed by a big fall.

By now you know where I’m going with this. I believe the second half of the decline in housing prices was due to the very tight money policy of late 2008, which depressed NGDP growth about 9% below trend between mid-2008 and mid-2009. The first half of the decline was due to “other factors,” which might have included the immigration crackdown and/or mistakes in forecasting by housing market participants.

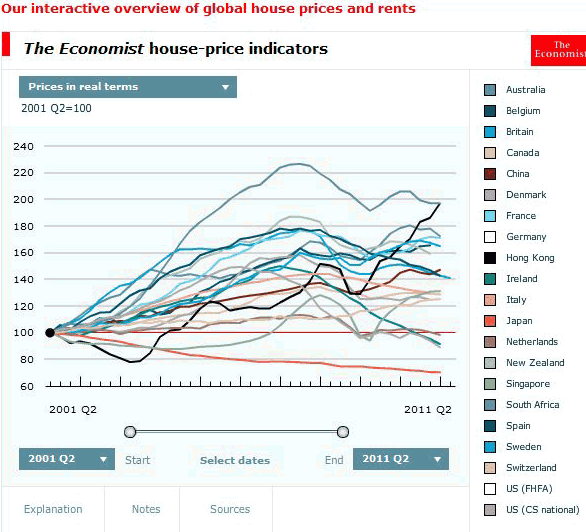

To better understand this argument it might help to look at global home price trends:

This is a graph showing real home prices in many countries. It is hard to read so I’ll just tell you that the gray line shows US prices rising about 50%, peaking in early 2006, and then falling back to their original levels. (The peak is earlier than in other countries.) Many people wrongly think that the big increase in real home prices shows that housing was too expensive in mid-2006. That “what goes up must come back down.” Not so, as you can see real home prices in most countries went sideways after 2006.

But if you take a close look at the pattern, you will see that foreign real home prices tended to continue rising after 2006 and then fell in 2009, when world NGDP plunged. Thus foreign markets (excluding possibly Ireland and Spain) didn’t seem to be affected by the problems that hit the US in 2006. The modest declines you see in the other markets occurred for the same reason that the US market kept falling in 2008-09. Falling NGDP.

If NGDP hadn’t declined in the US, prices would still have fallen modestly in 2006-07, but not enough to be such an obvious bubble.

If prices had leveled off at the peak, no one would call it a bubble. Because they fell all the way back down, everyone except Eugene Fama calls it a bubble. If they fall modestly then it would have been a “borderline bubble.” (This happened in my hometown of Newton.)

Tight money in 2008-09 turned a borderline bubble into a gigantic bubble. The beautiful symmetrical shape we actually observe for US prices, like that classic volcano in the Philippines, is half due to real factors and half due to tight money.

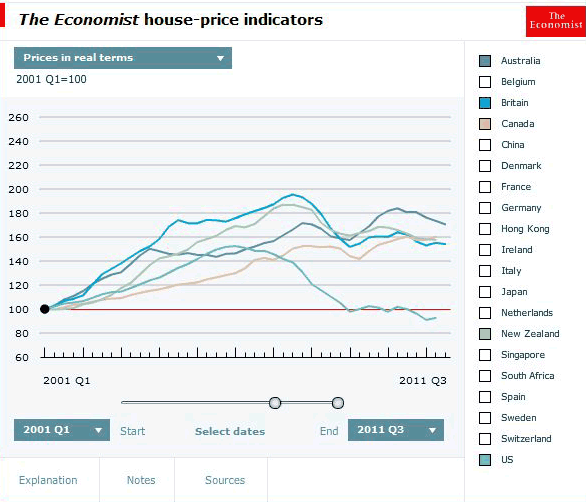

Here’s an easier to read graph with 4 other English-speaking economies.

Notice that since the US peaked in early 2006 those countries have mostly seen prices go sideways (up a bit in two and down a bit in two.) Prices move around all the time, no one would consider those examples of “bubbles.” Real prices are still quite high in all 4 countries.

I don’t see why it was “obviously irrational” for American home purchasers in 2006 to expect future real homes prices in America to follow the same sort of pattern as future home prices in Canada, Britain, Australia and New Zealand. But Fama and I seem to be about the only people on Earth who feel that way. Everyone else is convinced that everyone around them is completely irrational about home prices. But if “everyone” is completely irrational about home prices, why should I accept “everyone’s” view that markets are obviously irrational? Would you poll residents of a lunatic asylum to ask which inmates were insane?

PS. Matt Yglesias has a great post that is loosely related to this one. He discusses the sort of crisis we should have had. The one that would have occurred had NGDP not plunged in 2008-09.

Leave a Reply