Equities are down sharply this morning with the dollar higher, bonds higher, oil back below $100, gold & silver lower, and food commodities tumbling (thank goodness).

First I want to comment that there are many indicators suggesting that a pretty major top in equities is either in or approaching. I posted comments from McHugh inside of today’s Daily thread for those who are interested, keep in mind that the markets are NOT real, they are a manipulated illusion with the rule of law no longer enforced.

JPMorgan met earnings expectations but income was down 23%, poor bastards, they “only” “earned” (stole) $3.7 Billion! Not enough, their stock is down sharply, LOL. What a screwed up game.

More talk about downgrades coming, that is also pressuring sentiment. Of course that’s all just a racket of self-interest too, completely devoid of reality.

The Trade Deficit for November came in larger than expected. That will drag on GDP calculations, and notably it was our exports that were weak… tie that piece of information with Export Prices which just fell by .5%, and you can see that there’s trouble brewing, not that Econodream can see it:

Highlights

In November, the U.S. trade deficit widened sharply in November due largely to a jump in oil imports but also due to a dip in exports. The trade gap grew to $47.8 billion from $43.3 billion in October (originally $43.5 billion). The latest shortfall was much more negative than the consensus forecast for $45.0 billion. Exports declined 0.9 percent after dipping 0.7 percent in October. Imports rebounded 1.3 percent in November, following a 1.0 percent decline the prior month.The worsening in the trade gap was led by the petroleum gap which expanded to $27.6 billion from $24.2 billion in October. The nonpetroleum goods deficit widened to $34.8 billion from $33.2 billion the month before. Several factors were behind this, including a drop in exports of nonmonetary gold and a boost in automotive imports. The services surplus was slightly improved at $15.4 billion from $15.3 billion in September.

On a not seasonally adjusted basis, the November figures show surpluses, in billions of dollars, in part with Hong Kong $3.2 ($3.0 for October), Australia $1.5 ($2.1), and Singapore $1.0 ($1.0). Deficits were recorded, in billions of dollars, in part with China $26.9 ($28.1), the European Union $9.7 ($8.0),OPEC $9.1 ($8.3), Japan $6.2 ($6.2), Mexico $5.5 ($5.3), Germany $4.7 ($4.3), and Canada $3.0 ($2.2).

Today’s report is moderately complex. You cannot attribute the huge worsening to any one fact. Due to special factors, it is very likely that the November number will be partially reversed soon and significantly. Exports of nonmonetary gold have been volatile recently. The surge in oil imports cannot continue at that pace. And the jump in auto imports probably was just American auto companies taking delivery of production in Canadian facilities outside of Detroit. So, economists will be shaving their forecasts for fourth quarter GDP but underlying trends appear to be changed only very slightly with weakness in exports to Europe likely real but not that significant.

Import and Export Prices for December are both negative, and the year over year figures are still high but coming down. Here’s Econoclueno:

Highlights

A monthly dip in petroleum prices helped pull down import prices by 0.1 percent in December. Excluding petroleum which helps smooth out monthly distortions, import prices rose a very mild 0.1 percent following 0.2 percent declines in the prior two months. Price pressures of imported finished goods rose but only slightly to still subdued monthly rates of 0.2 percent for both imported capital and imported consumer goods. Prices for imported vehicles rose only 0.1 percent.There’s also no trouble on the export where prices fell a steep 0.5 percent in the month following a 0.1 percent gain in November and a 2.0 percent fall in October. Prices of agricultural exports swung lower in December after swinging higher in November and lower in October.

The strengthening dollar, strength tied to investor demand for safety, is helping to subdue import price inflation. Today’s report points to mild readings for next week’s producer and consumer price reports.

Waves of inflation, waves of deflation, but the overall trend is inflation. We may see another bought of deflation here, but yes, it will be met with more… bigger numbers, more frequent and significant other events.

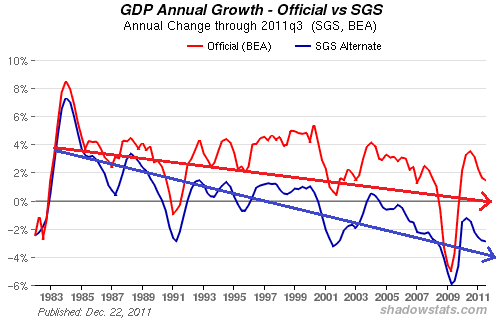

Again, let’s look at the Shadowstats “Growth” chart… this time I want to point out the waves – waves of inflation, waves of deflation. In this case, however, the trend is for lower growth, that is due to macroeconomic debt saturation:

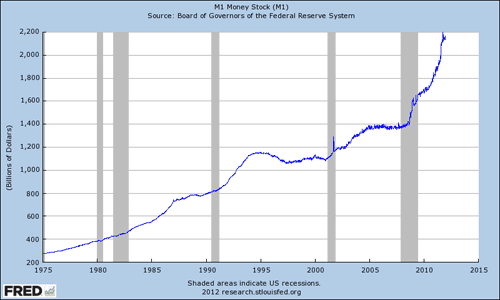

Again, I will post a chart of M1 – just exponential math creating a parabola of increasing numbers, this is what cements the power for those who wrongly are allowed to produce money from nothing:

…And I know, it’s been coming for some time…

Leave a Reply