Menzie Chinn at Econbrowser looks at the OECD data and concludes the world is close to stall speed. Alcoa is an early victim, as the impact of the European financial crisis becomes evident. Via Reuters:

[Alcoa] CEO Klaus Kleinfeld warned of weak economic conditions through the year, particularly in Europe, “as confidence in the global recovery faded.”That sapped aluminum demand from the automotive, industrial products, construction and packaging sectors since the second quarter, with only the aerospace and transport sectors growing.

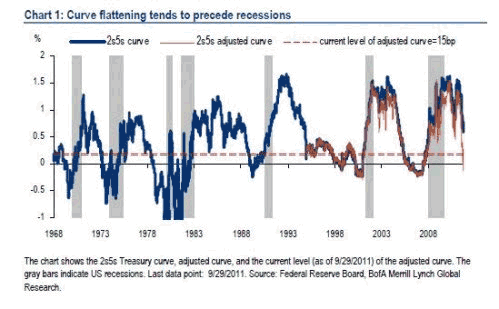

Can the global economy recovery? WIll the damage be limited to Europe? With growth teetering on an edge, it would be nice to have one old US recession indicator back in the tool kit – the yield curve. With short-term interest rates at zero, it is impossible for the yield curve to invert, a traditional indication of recession. Bloomberg reports on an effort to overcome this challenge and regain that tool:

The bond market indicator that has predicted every U.S. recession since 1970 shows that the economy has about a 60 percent chance of contracting within 12 months.

The so-called Treasury yield curve, adjusted for distortions caused by the Federal Reserve’s record low zero to 0.25 percent target interest rate for overnight loans between banks, shows that two-year notes yield 20 basis points, or 0.20 percentage point, less than five-year notes, according to Bank of America Corp. research. The unadjusted gap of 79 basis points at the end of last week indicates the chance of recession at about 15 percent…

…“The adjusted curve is giving a powerful signal for an upcoming U.S. recession,” said Ruslan Bikbov, a fixed-income strategist in New York at Bank of America, one of the 22 primary dealers of U.S. government securities that trade with the Fed. “If that happens, the Fed’s target rate could remain near zero beyond 2014,” more than a year longer than the central bank has indicated, he said in an interview on Oct. 3.

More on the topic can be found at the FT Alphaville blog, including this chart:

Alas, still not the defining indicator we could hope for. While 60% is better than even, it is still a call that lacks conviction. As are the other outlooks reported by Bloomberg. First:

Goldman Sachs Group Inc., another primary dealer, puts the odds of another recession at 40 percent, the firm’s economists wrote in an Oct. 3 report.

Next:

JPMorgan Chase & Co. economists said in an Oct. 7 report that they see “a soft growth picture, but one that is not falling into recession at the moment.” The firm, also a primary dealer, forecasts the 10-year note yield will end the year at 2.25 percent.

Then:

“Markets these days give mild signs of a collapse,” Gross said in an Oct. 4 Bloomberg Television interview with Lisa Murphy. The odds of recession in developed economies is about 50 percent, with the U.S. on the “brink,” he said. “This is one of those times where you are worried about the return of your money.”

60%, 40%, 50%. Still seems to be only one firm with a strong conviction:

A “contagion” of economic indicators have come together to signal the economy is tipping into a contraction, according to Lakshman Achuthan, co-founder of ECRI, a research firm that predicts changes in the economic cycle.

“You have wildfire among the leading indicators across the board,” Achuthan said in a radio interview on Sept. 30 on “Bloomberg Surveillance” with Tom Keene and Ken Prewitt. “It’s a vicious cycle that is going to get quite a bit worse.”

Truth be told, I can’t admit to being much better. I am seduced by the logic that room for recession is limited given the failure of many sectors, notably autos and housing, to fully or even begin to recover from the last recession. That said, the near-term policy picture in the US looks dismal and I am extremely wary to dismiss the European financial crisis as something easily resolved. Moreover, while some attributed Monday’s rally on Wall Street to a positive reaction to the news that China was moving to support their banks, I saw only an indication the Chinese economy is on a very weak footing. Combining these thoughts with the memory that the safe bet over the past three years has been on the weak side of the coin, I too am pushed over the edge with better than even odds of recession. And while I will be searching for clues about the Fed’s intentions in the release of the FOMC meeting minutes, I suspect that if the seeds of recession are already planted, policymakers are already too far behind the curve to engineer a timely rebound.

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply