Peter Wallison of the American Enterprise writing in today’s WSJ, explains that the Wall Street protesters have been grossly misled because it was “Reckless government policies, and not private greed, that brought about the housing bubble and resulting financial crisis.” Here’s an excerpt:

“Beginning in 1992, the government required Fannie Mae and Freddie Mac to direct a substantial portion of their mortgage financing to borrowers who were at or below the median income in their communities. The original legislative quota was 30%. But the Department of Housing and Urban Development was given authority to adjust it, and through the Bill Clinton and George W. Bush administrations HUD raised the quota to 50% by 2000 and 55% by 2007.

It is certainly possible to find prime borrowers among people with incomes below the median. But when more than half of the mortgages Fannie and Freddie were required to buy were required to have that characteristic, these two government-sponsored enterprises had to significantly reduce their underwriting standards.

Research by Edward Pinto, a former chief credit officer of Fannie Mae (now at the American Enterprise Institute) has shown that 27 million loans—half of all mortgages in the U.S.—were subprime or otherwise weak by 2008. That is, the loans were made to borrowers with blemished credit, or were loans with no or low down payments, no documentation, or required only interest payments.

Of these, over 70% were held or guaranteed by Fannie and Freddie or some other government agency or government-regulated institution. Thus it is clear where the demand for these deficient mortgages came from.

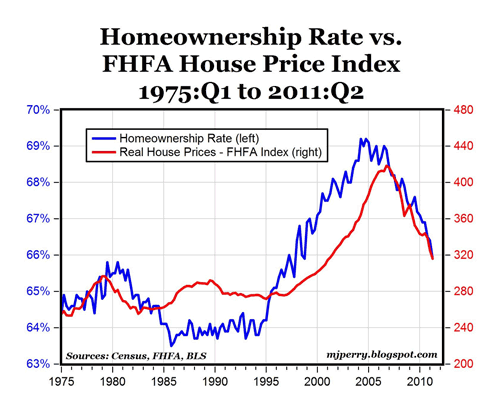

The huge government investment in subprime mortgages achieved its purpose. Home ownership in the U.S. increased to 69% from 65% (where it had been for 30 years). But it also led to the biggest housing bubble in American history (see chart above). This bubble, which lasted from 1997 to 2007, also created a huge private market for mortgage-backed securities (MBS) based on pools of subprime loans.

As housing bubbles grow, rising prices suppress delinquencies and defaults. People who could not meet their mortgage obligations could refinance or sell, because their houses were now worth more.

When the bubble deflated in 2007, an unprecedented number of weak mortgages went into default, driving down housing prices throughout the U.S. and throwing Fannie and Freddie into insolvency. Seeing these sudden losses, investors fled from the market for privately issued MBS, and mark-to-market accounting required banks and others to write down the value of their mortgage-backed assets to the distress levels in a market that now had few buyers. This raised questions about the solvency and liquidity of the largest financial institutions and began a period of great investor anxiety.

The narrative that came out of these events—largely propagated by government officials and accepted by a credulous media—was that the private sector’s greed and risk-taking caused the financial crisis and the government’s policies were not responsible. This narrative stimulated the punitive Dodd-Frank Act—fittingly named after Congress’s two key supporters of the government’s destructive housing policies. It also gave us the occupiers of Wall Street.”

MP: The chart above shows how the weakening of underwriting standards did boost the homeownership to rate to an historically unprecedented level above 69% by the end of 2004, but in the process created an unsustainable housing bubble that started unraveling in early 2007. Now real home prices (measured by the FHFA index) are back to 2001 levels and homeownership rates are back to the levels of the late 1990s.

The FHFA filed a lawsuit with FRAUD against 18 financial institutions on behalf of Fannie and Freddie.

The FHFA is also negotiating a settlement with other institutions not sued (Wells Fargo, PHH, etc…).

Also there are many “putbacks” demands on mortgages sold to Fannie and Freddie.

Private banks have been sued for selling fraudulent information, get it?

Big banks-lobbysts can’t rewrite history, that’s a reckless endangerment.