The Swiss National Bank released its 8/30 balance sheet the other day. Zero Hedge did a report (link). The link (PDF) to the SNB data.

The bottom line is that in August Swiss reserves rose by CHF 115b. A monthly increasing of 50% (Staggering). Domestic liquidity (sight deposits) rose an (unbelievable) 390% (CHF 49b to CHF 191B). This information covers the period when SNB bet the farm in an effort to stabilize/weaken the CHF. I’ve been looking at these results for days. Some very dramatic steps have been taken.

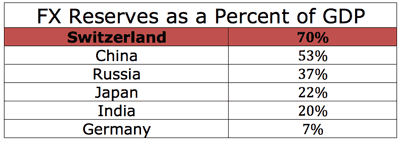

To provide some perspective consider where Switzerland sits on the rankings of foreign currency reserves to GDP.

This is not a list that Switzerland really wants to be on top of. There is very little reward that can be realized, there is a great deal of risk.

The increase in SNB sight deposits is somewhat analogous to the QE actions by the Federal Reserve. Both central banks have taken steps to electronically print money. The consequence is a sharp increase in the Balance Sheet of the CB. In both cases there is a huge pile of money created in the form of bank reserves (sight deposits).

In the USA the Fed has done (so far) $1.35T of QE. That comes to 9%% of GDP. The SNB, on the other hand, has done an amount equal to 25% of GDP in just one month.

I make these comparisons in an effort to demonstrate that what the SNB is doing is over the top. The steps the SNB has taken are without precedent.

So far, the actions by the SNB have been successful. The key EURCHF rate has been steadily above the 1.20 level. The folks in Zurich/Basel are touting the SNB action as a big success. It might be a bit early to celebrate.

It’s impossible to look into the future with any clarity these days. There are a myriad of possible outcomes in front of us. It’s possible that a soft landing for the global economy (and the SNB) is in our future. On the other hand, there are several scenarios where the actions by the SNB could blow up in their face. You tell me if any of these are possible outcomes:

The dollar gets much stronger vs. the Euro

I’ve been arguing for a big jump in FX volatility. It’s happening. There is a distinct possibility that the EURDLR could make a mad dash to 1.0 – 1.05. All the pieces are on the table for a significant adjustment. One factor in favor of this outcome is that it would be a very big boost for the EU exporters/economy. With energy getting cheap, there are plenty of “deciders” that would love to see the Euro make a big retreat. It would blunt the deflation that is staring them in the face.

Should this happen, you get USDCHF at 1.15-1.20. That’s a very interesting exchange rate.

Up to now the money going into CHF has been a Euro phenomenon. The Swiss really don’t care about the dollar rate. But holders of dollars will care very much if the SNB is going to create such a lovely effort to get short the USDCHF. Consider this chart for some perspective.

At some point the CHF will become attractive to global holders of dollars. It doesn’t matter that the CHF interest rates are at zero. US rates are also zero.

Should things go in this direction the SNB would be forced to absorb a potentially huge supply of dollars. The 1.2 link to Euro would force their hand. Are there dollar holders who would line up for the opportunity to diversify reserves and investment funds into CHF at the right price? You bet there are. A half-trillion ++ would love to make a move on these terms.

In this environment reserves at the SNB would be exploding. They could easily double from current levels and exceed 200% of GDP.

Germany abandons the Euro

This may seem like a far-fetched outcome. It’s not. 75% of adults in Germany are saying “No” to more EU bailouts. The possibility that Germany “Opts out” and re-established the Deutche Mark is a very possible outcome.

In this scenario the Euro (sans Germany) would be worth (overnight) 75 cents on the dollar. This would be the nuclear winter for the SNB. Losses on devalued Euros could top CHF 100 billion.

A two-tiered Euro is established

The SNB has a policy in place where they invest excess Euro reserves in debt obligations of France and Germany. If there were to be a two tiered Euro the SNB would be the owner of the “good” Euros. But should the Swiss be beaten into submission they might end up with some of those “Bad” Euros. See following.

The “Beggar My Neighbor” factor

The SNB has taken the position that their decision to devalue the Franc by 15% was defensive. I’m waiting for the arguments to come forward that say it was a decidedly offensive move. What has happened to the Swiss Currency is not that much different than the Yen. Think what the global response would be if the BOJ engineered a 15% devaluation. Universal condemnation would be the result. Tim Geithner would hit the roof. Congress would rapidly brand Japan as a currency manipulator. So why haven’t Switzerland’s neighbor made a stink? I think it’s just a matter of time.

If we wander down the road where the SNB is forced to absorb more Euros, the issue of what they are doing with the money is going to come into question. We have a situation where China and Russia have indicated their willingness to absorb more Euro sovereign paper (non German/French). Could Switzerland continue to hold it’s nose on Spanish and Italian paper under these conditions? Possibly, but they will look awfully stupid, a very bad neighbor indeed.

To me, it’s not possible that the Swiss government will allow this to happen. When the European papers start running the story, “The Cheap Swiss” the pressure will build. In the end, the SNB will be forced to buy EU peripheral sovereign paper. That would open the door to losses on the sovereign debt due to restructuring. It also opens up the risk of the SNB receiving those “bad” Euros if a two-tiered option is the end game.

I actually don’t think any of these possibilities is all that far-fetched. I’m sure that the folks at the SNB are looking at the same things I am. I wonder if they are crapping in their pants at any of these prospects.

The SNB has a long history of bad market timing and improper policy responses. (They sold tons of gold at $450 and bought boatloads of Euros at 1.50 per Franc). I think the steps they took in August were ill timed and the actions they took were inappropriate. But now they are pregnant. This will be a very high-risk baby.

Notes:

What is the SNB is doing with all the Euros they acquired in August?? I suspect they may have diversified a portion of that into Sterling and Yen. Those crosses have been heavy on the offer for the past month.

Should we get confirmation of this in a few months there will be hell to pay. The BOJ and BOE will be pissed that Switzerland is passing the trash back in their direction. It’s at about that time that the first “Cheap Swiss” article will appear.

****

There is an alternative that is available to the SNB. They could sterilize all of the unwanted reserves (And all the problems they create) by converting those lousy reserves into gold. I guaranty you that this option is under consideration. It’s the only choice that makes sense.

Leave a Reply