But first, what a difference a phone call makes.

- Germany and France put in a “catch up” to their pal Papa in Greece and tell the world that they told him that they are right behind him. Is that Little Timmy G’s voice we can hear in the background?

- The Letch makes a “tell it like it is” call that mentions Mangler is overheard.

- A UBS trader makes a couple of calls which result in a final one to his imminently ex-boss involving the words “HOW MUCH?????” being screamed a lot.

To which the market is replying:

- “Oh good, that’s all sorted then. Can I now buy Greek debt yielding over 100%?”.

- “Ooohh… he’s a one isn’t he!”.

- “Jeez, that’s not good. I’d better shut down my risk just in case I haven’t dotted an ‘i’. Wish I was a forensic auditor, demand is about to go through the roof again. Oh gawd, we are going to have Vince Cable on every media outlet crowing his ‘told-you-so-evil-bankers-turn-them-all-into-village-post-offices-staffed-by-sweet-old-ladies’ mantra”.

But TMM is thinking:

- Is that Timmy G’s voice in the background? This should be enough to divert the attention of the attack dogs long enough to focus on other market things. Isn’t Aussie looking sick!

- Its always been hard to prove that Berlusconi has lied.

- Rogue trader announcements have uncannily marked market turns (Leeson and Kerviel). There is no hint as to where the UBS losses came from just yet but how absolutely ironic it would be IF the losses came about through the dramatic actions of the SNB.

There has, however, been one phone call made that makes no difference at all:

“Hello Mr Osborne. This is Dr King. Mervynflation and our expectations thereof are running like Usain Bolt on speed, but as policy bias appears to be moving from monetary to fiscal, it’s not my problem and I suggest you raise taxes”.

Now then, on to something that has been sticking in the craw of TMM for some time and has them jumping up and down in frustration every time a headline on European finding is waved in front of them as example of “the massive US$ funding crisis that European banks are suffering”. The sheer frenzy that journos and punters whip themselves into reminds them of this scene.

TMM reply “there isn’t a funding crisis – there are more dollars floating around than you can imagine” and here we put our case as to why and try to debunk some of the recent hysteria over “funding” headlines, messages, emails and cut n pastes from the “Hero Zedgers” that appear to confuse simple issues. We want to clear a few things up.

Forgive us for starting with old material, but for completeness, in the early days of the crisis, as USD funding markets shut down, leveraged institutions in Europe and elsewhere were forced to use the FX Forward market to borrow Dollars in significant size, driving the Cross-Currency Basis sharply negative. In the case of EURUSD, this basis is the difference between exchanging a stream of US 3m Libor coupons and a stream of EUR 3m Euribor coupons, and is quoted as the number of basis points deducted from the 3m Euribor stream. If 3m Libor and 3m Euribor were both riskless and there were no relative liquidity preference for USD over EUR, then this difference would be ZERO and the FX Forward would be priced as the difference between the two deposit rates. However, that is the world of textbooks, academics and arbitrage, something TMM have rarely found to be useful in their careers. But we digress, the point here is that the more negative the basis moves, the more people are willing to pay for USD through the FX Forward market.

Since 2008/9, cross-currency based funding has reduced significantly as banks and hedge funds de-levered their balance sheets, and the advent of QE led to the explosion of the Fed’s balance sheet and a sharp increase in the excess reserves of foreign banks’ US subsidiaries accounts with the Fed. This means that cheap and abundant USD funding has been available to those large international banks lucky enough to have an account with the Fed, but smaller ( and usually peripheral European banks) in need, have usually had to utilise the FX Forward market to borrow dollars.

With the European situation deteriorating, the 3m Cross-Currency Basis (see chart below) has once again moved sharply negative, but in contrast to 2007-8, TMM’s mates in the forward market report more USDs than pieces of Lego in the overnight and tom/next markets, while term prices are moving largely on the back of broad-based risk aversion. This is an important point – early on in the crisis, FX Forward and basis markets were a leading indicator of trouble precisely for the reason that such large funding exposures had been built up in the 5years prior. This just isn’t the case anymore. By early-2009, the large part of bank cross-border funding exposures had been unwound as European banks sold EUR/USD in order to pay down the losses on those US assets. And, as above, central banks have provided significant amounts of liquidity and liquidity back stops in the form of FX Swap lines – simply put, the amounts traded in this market just aren’t that large anymore, because generally, banks do not need to tap it for USDs.

(click to enlarge)

Yesterday, TMM’s IBs lit up in excitement at the ECB’s USD Auction Allotment showing that two banks had borrowed the princely sum of $575m from the ECB. The below chart of the facility’s usage should put this into perspective. Today’s ECB marginal lending facility showed a jump to EUR 3.4bn borrowed, from the usual few hundred million a day. More excitement. I don’t think anyone would be particularly surprised that a few peripheral banks might be having a tiny(!) bit of problem funding, and were forced to go to the ECB facility to pay 2.25%. But let’s be realistic- versus assets earning yields of 5% or more, this is hardly going to force them to go bust. But that is a different point entirely. TMM’s main point here, is that this number often bobs up and down because of technical factors such as:

- A missed payment from a counterparty for a number of reasons ranging from human error to IT systems issues.

- Someone not accessing the ECB’s MRO in enough size and thus being forced to pay up for funds.

- Someone getting their funding calculations wrong (TMM have seen it happen first hand) and it being too late to rectify by the time they realised this.

- An unexpected late day payment.

This stuff just happens, it is not unusual. Of course, were the amount to move rapidly higher then it would certainly signal something more serious, but as of now, TMM are unconvinced.

(click to enlarge)

Next, while historical data for European CP issuance in the US is sketchy, due to the primary nature of the market, as a proxy, the below chart shows 30day Natixis Commercial Paper, which should be a reasonable approximation to the rates that European banks are paying directly on CP in the US. It has certainly moved higher over the past two months, but as a reality check, 0.45% for one month unsecured money is hardly a sign of severe funding stress.

(click to enlarge)

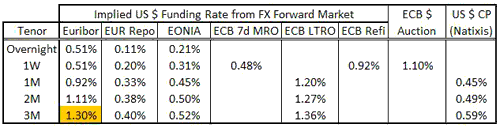

As a comparison, the below table shows the current implied US $ funding rates from the FX Forward Market vs the ECB $ Auction and the above direct US $ CP issue assuming different rates of Euro funding – unsecured (Euribor), EUR Repo market, EONIA, the ECB’s 7 day MRO, the LCB’s LTROs and the ECB’s main refinancing rate. The ECB $ Auction works out to be about 1.1% (1week US OIS +100bps), but in reality is a bit more expensive than that due to the need to post collateral for the 12% haircut. The point below is that generally, market Dollar funding costs are just not high enough for banks to need to tap the Fed/ECB swap lines, with only the 3m Euribor-based rate being really higher than the ECB auction rate.

Graphically, looking at the 1M implied funding rates, it’s not really obvious that these are particularly extraordinary, and only at the kind of levels seen last December. The Orange line shows the rate implied from Euribor, the yellow line implied from the ECB’s LTRO, the whte line implied from Eonia, the green line implied from Euro repo and the pink line the Natixis US CP rate. The chart makes clear the distinction between unsecured borrowing in Europe and swapping it (orange), and accessing the ECB’s LTRO and swapping it (yellow) and the secured repo-based borrowing (green) and the better-quality banks that are still able to access the Eonia market (white line) and US market direct (white line). As we have hit the level at which it is becoming attractive to access the ECB’s US $ Auction facility, TMM would not be surprised to see the allotment here move higher should current market rates prevail, but would not read anything into it other than the fact that it may well be cheaper to tap than the market itself…

(click to enlarge)

A slightly longer term chart:

(click to enlarge)

Unless the allotment spiked dramatically into tens of billions of Dollars TMM does not think there really is a Dollar funding crisis in Europe.

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply