Data has not been kind in recent weeks, sending second quarter forecasts tumbling below 2%. But that is not all; third quarter forecasts are heading lower as well. Ryan Avent questions this rush to judgment:

Meanwhile, early forecasts for third quarter output growth are being revised down. That seems premature to me; the third quarter has only just begun and it still seems likely that low petrol prices and a recovering Japan, among other things, may buoy American output.

This is a good question – do we have enough data to appreciably alter estimates of the third quarter? As Avent notes, the quarter is only two weeks old, and at least a few temporary factors are already in reversal. Once these factors clear, hesitancy to hire new employees should dissipate.

Alternatively, will the slowdown in the first half of the year trigger a cascade of weakness that will drag down the latter half as well? If so, it is appropriate to lower third quarter estimates.

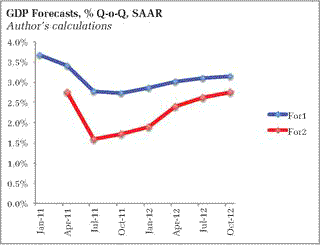

To get a sense of how a fairly simple model might be tell us, I dusted off the simple four variable vector autoregression (VAR) I used back in February to look at the impact of commodity prices. I updated the data and used the model for two forecasts, one with that sample ending in 4Q10 and a forecast starting in 1Q11, labeled For1. The second sample incorporates the next quarter of data, with the forecast beginning in 2Q11, labeled For2. The impact of the weaker than expected first quarter and the higher than expected gain in commodity prices has a significant impact on the forecast through 2012:

The model’s estimate for the second quarter shifted down to 2.7% – which, interestingly, was just about the 2.6% consensus forecast in the June 2011 Blue Chip release. The impact of the commodity price shock extends the growth decline into the third quarter of this year before activity slowly –very slowly – begins to recover.

One might wonder if the US economy could really linger at growth rates well below 2 percent for 3 or 4 quarters without tipping over into an actual recession. Moreover, it is worth considering that such a forecast leaves the US very vulnerable to negative demand shocks such as thought that might occur if the Europeans don’t get their act together. Not to mention the antics of their counterparts on this side of the Atlantic.

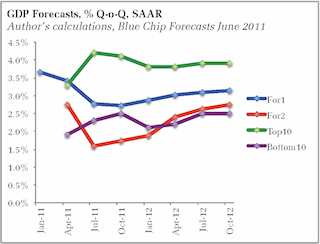

How do these forecasts compare with those of the June Blue Chip forecasts? I think it is interesting to look at the averages of the top and bottom ten forecasts:

In contrast to the simple VAR model, both the top and bottom forecasters expected first half weakness to be temporary, with growth rebounding in the second half. The “smart” forecasters knew what the “dumb” model didn’t – that temporary factors were dragging down the first half.

Now those same forecasters worry the model wasn’t so dumb after all, and thus need to bring down the third quarter. The commodity price hike was simply more severe, with more persistent impacts, than initially expected.

The bottom 10 forecasters see growth settling in at 2.5% by the end of 2012, not far below the simple VAR – they follow different paths to get to the same place. By contrast, the optimistic group is looking at growth rates of 3.9% at the end of 2012, apparently using models and judgment not dissimilar to our friends on Constitution Ave.

I suspect that if I continue this analysis, the simple VAR will almost always tend to be near the consensus (about the midpoint of the top and bottom averages) 4 to 8 quarters out, sliding between the top and bottom forecasters as the data evolves. Reconciling the model and forecasters in the near term, however, is a bit more of a challenge.

Bottom Line: My judgment is not too far from Avent’s – temporary factors are at play. My simple model, however, is telling me that those temporary factors have more persistent impacts than my judgment initially expected. Critically, although oil prices have eased, gasoline prices remain near recent highs, and this looks to be having a significant impact on consumer attitudes. Moreover, there are two big negative risks in the final half of this year, European debt crisis and US fiscal contraction. Overall, I would agree with forecasters leaning on the side of caution and shade down my expectations for the second half while hoping the error is in Avent’s favor.

Leave a Reply