Citigroup’s Semiconductor Equipment team is making a significant call on the space, turning bullish again after several months of being very bearish. Title of the call is “Samsung’s Gift to Semicon”.

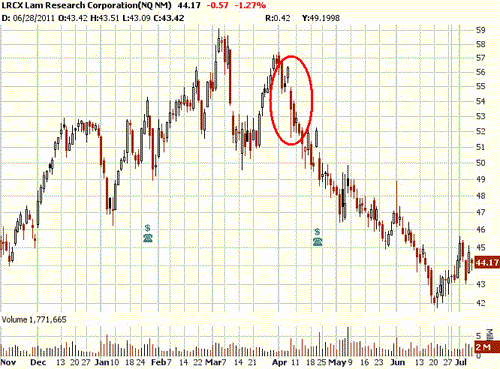

– Lam Research (NASDAQ:LRCX) is their new favourite pick in the space, after being on Citi Top Pick Live Sell list since April 6. They are upgrading LRCX to a Buy with $62 price target (prev. $43).

ASML and KLAC get upgraded to Hold from Sell. NVLS & AMAT remain at Hold.

Not only has LRCX meaningfully underpeformed the group in 2011 and back to historically attractive valuation levels, but should also be a significant near-term beneficiary from Samsung, according to Citi.

The details:

Samsung is finally coming back; increasing CQ3 from -10-15% to flattish — Citi’s most recent checks indicate that Samsung is finally coming back to the table to place many of the orders pushed out in April. Specifically, the firm now thinks Samsung will take 20k wsm capacity for Line 16 phase 2 NAND ramp and ~30k wsm tool upgrades for Line 15 DRAM shrink, both of which should now order and ship in CQ3. They estimate this is nearly $1B of the ~$1.5B previously pushed out – a swing factor of ~15% on a wafer fab equipment order run rate of ~$6.5-7B for CQ2.

Overall, we believe this amounts to nearly ~$1B that should come back into CQ3, which should provide ~10-15% of the upside for CQ3 orders/shipments for the major front-end names. This essentially “fills the gap” between what the firm thought was previously a down 10-15% CQ3 and now looks more flat.

Importantly, Citi believes this should start to come through this week at the Semicon/WEST tradeshow and be reflected in surprisingly good sentiment for CQ3 relative to current Street expectations.

– Orders now below normalized levels, baking in $27B WFE — Citi estimates CQ2 wafer fab equipment (WFE) orders were back to ~$27B/yr run-rate, down from >$40B in CQ4:10 (fueled largely by ASML) and below the ~$29B/yr they consider “normalized”. Not only is this decline consistent with the correction magnitude in ‘04/’05 (the last supply-driven correction, ’01 and ’08 were demand-driven where GDP slowed meaningfully), but $27B WFE would be down ~15% from the $32-33B still suggested by equipment companies and bottom-up capex analysis for 2011.

Citi’s sector view — While supply has ramped in face of end-market demand questions + IC inventory headwinds, the sudden and meaningful order pullback has mitigated risk while Street sentiment now very negative. Looking to 2012, it is hard to see a big down year given rising capital intensity, lack of memory over-spend, and INTC “changing the game” in the foundry segment. Their tgt increases are based on a new higher normalized mkt size due to higher capital intensity. LRCX/TER/FORM remain top ideas.

Notablecalls: Citi’s Timothy Arcuri caused 8% intraday drop in LRCX on April 6, when he issued a Top Picks Live Sell rating on the name, claiming Samsung decided to push out shipments with the company.

April 20 results & guidance by LRCX confirmed his suspicions sending the stock further down.

Goldman Semicap analyst upgraded LRCX on May 5 but the selling pressure was so intense the stock failed to hold gains even for the day.

– Now we have Arcuri coming out saying his uber-negative thesis is now reversed. Following recent underperformance & Samsung resuming orders LRCX is his favourite name in the group.

If that’s not a big call I don’t know what is.

Plus we have Semicon/WEST the biggest Semi event starting tomorrow July 12. Citi thinks this could ignite the group.

All in all, I suspect LRCX will trade up markedly in the n-t. It will almost certainly produce a 3-5% upside move from open but given the significance of the call this could push the stock up for several days. So buying the pull-back could work here as well.

Buying the other names in the sector may prove to be somewhat more tricky as we have UBS & Merrill both out with cautious pre-Semicon comments lowering their cap-ex growth rates for the space. They are obviously lagging behind Citi checks wise.

Tape’s drek so adjust your risk accordingly. It seems we’re in a state of panic this morning. Quite the change from Friday’s jolly bounce.

PS: I’m posting this at around 09:30 AM ET.

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply