Taxes reduce the payoff to entrepreneurship, investment, and work effort. If taxation is too heavy, these disincentives will weaken a nation’s economy. But at what point does the harmful impact kick in? And how large is it?

A puzzle

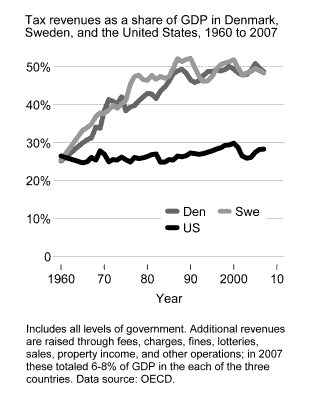

Half a century ago, in 1960, taxes totaled about a quarter of GDP in Denmark, Sweden, and the United States. The tax take then began to rise in Denmark and Sweden, reaching half of GDP by the mid-1980s, where it has remained. In America it has barely budged, hovering between 25% and 30% of GDP throughout the past five decades.

Has heavy taxation hurt the Danish and Swedish economies? If so, how much?

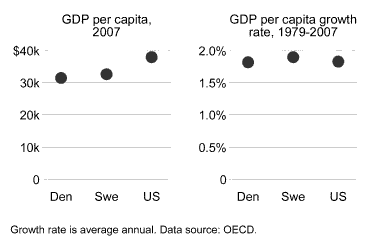

Begin with GDP per capita. America’s is higher than Denmark’s or Sweden’s. But that’s a legacy of the distant past. Growth of per capita GDP in the three countries has been virtually identical, both in the five decades since 1960 when the divergence in tax levels began and in the three decades since the 1970s (shown in the chart) when the tax difference has been most pronounced.

(Here and throughout I use 2007, the peak year of the pre-crash business cycle, as the end point. Adding the crash and its aftermath would improve the standing of Denmark and Sweden relative to the U.S.)

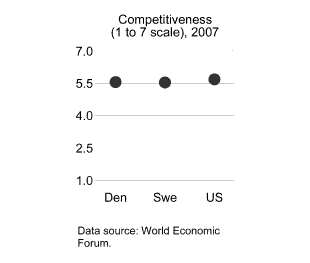

Each year since 2001 the World Economic Forum has scored most of the world’s countries on a “competitiveness” index. The index aims to assess the quality of twelve components of a nation’s economy: institutions, infrastructure, macroeconomic stability, health and primary education, higher education and training, goods market efficiency, labor market efficiency, financial market sophistication, technological readiness, market size, business sophistication, and innovation. In 2007 Denmark and Sweden were judged to be virtually identical to the United States in competitiveness. That was true throughout the decade. It also was true for the “innovation” components of the index in particular.

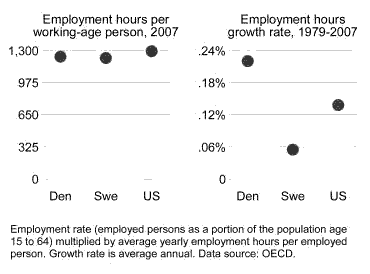

Employment, measured as average hours of paid work per working-age person, is a little lower in Denmark and Sweden (more here ). A larger share of working-age Danes and Swedes are employed — around 76%, compared to 72% in the U.S. But employed Danes and Swedes tend to work fewer hours than employed Americans — about 1,600 per year versus 1,800. This is due in large part to the fact that Danes and Swedes have more than five weeks of legally-mandated paid vacations and holidays, whereas Americans have none. This gap, in turn, is a function of historical differences in the strength of unions.

Employment hours increased between 1979 and 2007 in all three countries. The rate of growth was fastest in Denmark, followed by the U.S. and then Sweden.

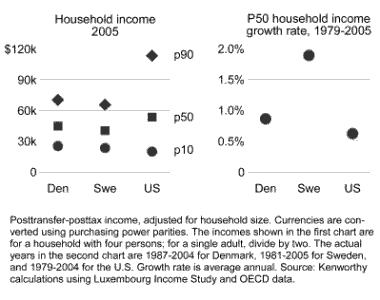

Household income (after taxes and transfers) is higher in the United States at the ninetieth percentile (p90) of the distribution and at the median (p50). This owes to differences in per capita GDP, in income inequality, and in the degree to which citizens receive their income in the form of (tax-financed) public services. Here too the U.S. has not gained ground in recent decades. Household incomes in the middle of the distribution have grown more rapidly in Denmark and Sweden than in the U.S. (shown in the chart), and at the ninetieth percentile they’ve increased at about the same pace.

At the tenth percentile (p10), incomes are higher in Denmark and Sweden. And they’ve increased more. (See here and here.)

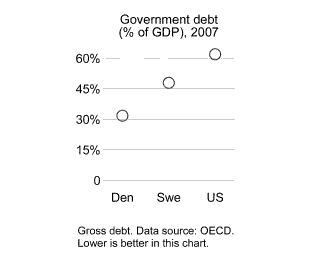

Denmark and Sweden have done better than the United States at keeping government debt in check.

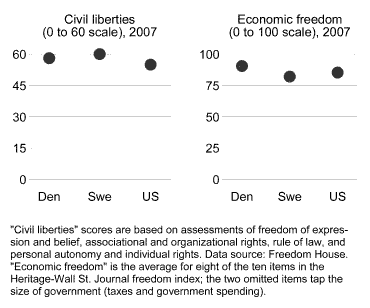

Have high taxes required a sacrifice of liberty? Not according to the Freedom House measure of civil liberties or the Heritage Foundation-Wall St. Journal measure of economic freedom.

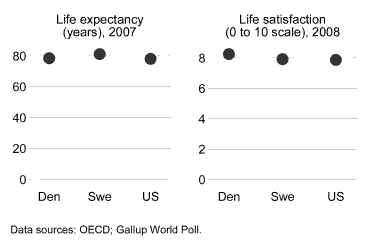

Finally, consider two social indicators of well-being: life expectancy and life satisfaction. On both counts, Danes and Swedes fare, on average, just as well as or better than their American counterparts.

If heavy taxation has harmful economic effects, why have Denmark and Sweden performed similarly to the United States during a period of several decades in which their taxes were much higher than America’s?

Three explanations that sidestep the puzzle

One common explanation is that small size facilitates administrative efficiency. The Danish and Swedish governments can function effectively because their scale is manageable. They are “big” governments, but in small countries. This might be true, but to say that heavy taxation isn’t a problem if government works well is to say that heavy taxation isn’t in and of itself a problem.

A second explanation looks to the mix of taxes countries use. The Nordic countries rely disproportionately on consumption taxes; in 2007 consumption taxes totaled 16% of GDP in Denmark and 13% in Sweden, compared to just 5% in the U.S. These are said to create less in the way of investment and work disincentives than do taxes on individual and corporate income.

Yet there is a sizeable difference in income taxation too. In the U.S. income taxes were 14% of GDP in 2007, versus 19% in Sweden and a whopping 29% in Denmark. More important, to suggest that heavy taxation isn’t harmful given an effective tax mix is to suggest that a high level of taxation per se is not necessarily harmful.

A third explanation points to tax compliance. Each April most Swedes receive a pre-prepared tax form. The relevant information about income, deductions, and the amount still owed or to be refunded has already been filled in by the Swedish Tax Agency. If the information is correct, the taxpayer simply confirms that by mail, telephone, or text message. Pre-prepared tax returns not only are more convenient for taxpayers; they also reduce cheating. Greater compliance, in turn, is likely to make heavy taxation more workable. If cheating is extensive, tax rates need to be higher in order to raise a given quantity of revenue, which increases the likelihood of disincentive effects on entrepreneurship, investment, and work effort. In a tax system with minimal cheating, more revenue can be raised at moderate tax rates.

This can’t be done in the United States, so the argument goes, because the American tax code (unlike its Swedish counterpart) has too many available deductions and rebates. But the U.S. could simplify its tax code to enable pre-preparation. Moreover, even with this advantage, income tax rates in Denmark and Sweden are a good bit higher than in the U.S. And a large portion of Danish and Swedish tax revenues come via payroll and/or consumption taxes, which are less vulnerable to evasion, in those countries and in the U.S. as well.

Two explanations that attempt to address the puzzle

Here are two accounts of Danish and Swedish economic performance that don’t sidestep the question of tax levels’ impact.

The first is hypothetical; I don’t know of anyone who’s offered this argument explicitly. It says that the adverse effect of taxation kicks in once a country passes 15% or 20% or 25% of GDP, and it doesn’t worsen the farther beyond that you go. Denmark, Sweden, and the United States each exceeded 25% already by 1960, so in this story we would expect the three countries to have experienced similar (poor) economic performance in subsequent years.

This hypothesis doesn’t strike me as especially compelling. None of the world’s rich nontiny democracies have had tax levels below 25% of GDP since the 1970s, and only a few have been below that level since 1960. Yet a number of these countries have had relatively good economic outcomes during this period.

A second explanation says the Danish and Swedish economies have performed similarly to America’s despite heavier taxes because they have some advantage(s) that I haven’t adjusted for. This certainly would be true if I had chosen Norway as one of the comparison countries. Norway’s economy has been boosted by extensive oil resources. Has Denmark or Sweden had any such advantage?

One possibility is catch-up. Laggard countries can get an economic growth boost by borrowing technology from the leaders. But this has become less relevant for Denmark and Sweden in recent decades, as they’ve invested heavily in education and R&D and become technological leaders in their own right (more here).

Ethnic and cultural homogeneity is sometimes mentioned as a key economic asset of the Nordic countries. This might help, though in rich nations diversity may have some benefits as well.

Corporatist policy making, which features institutionalized participation by business and labor representatives, is associated with faster economic growth in affluent countries in recent decades. This may have helped Denmark and Sweden. Yet both countries have made their share of policy mistakes.

Of course, the United States has some important advantages of its own, including a huge domestic market, excellent universities, a culture that prizes innovation and entrepreneurship, a well-developed venture capital system, bankruptcy laws that facilitate risk-taking, a tradition of regional mobility, and an attractiveness to talented immigrants. The question is: If taxation at Danish and Swedish levels has a significant negative economic effect, do Denmark and Sweden have advantages relative to the U.S. that are large enough to have fully offset that effect in recent decades? It’s a difficult question to answer with any certainty, but I think probably not.

A challenge

At what point does the harmful impact of taxes on the economy kick in? And how large is it? The Danish and Swedish experiences over the past generation pose a challenge for those who believe the answers to these two questions are “somewhere below 50% of GDP” and “large.” It’s a challenge that in my view has yet to be met.

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply