Analyst community appears to be somewhat mixed following blow-out earnings from Intel (NASDAQ:INTC) last night:

THE POSITIVE:

– J.P Morgan, a long term Semi Bear is upgrading INTC to Overweight from Neutral with a $25 tgt (prev. $20.25) noting they had previously been cautious on INTC primarily due to the company’s inventory being too high. However, inventory declined 10 days QoQ from 85 days in 4Q10 to 75 days in 1Q11, in line with the normalized level of 75 days due to higher than expected sales.

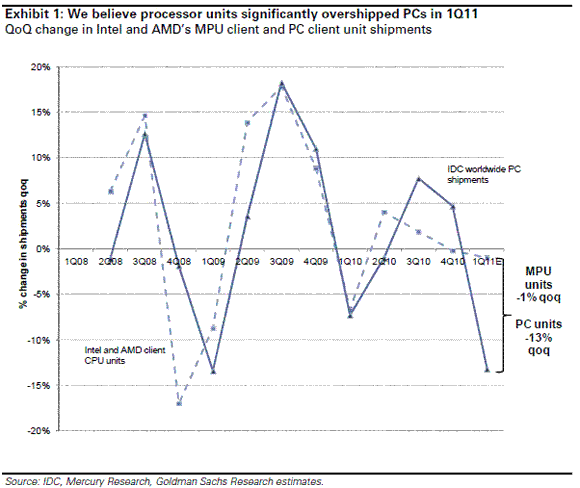

Inventory replenishment drove Intel’s rapid growth in 1Q11. Although Intel appears to have outgrown the PC industry substantially in 1Q11, JPM believes it is due to CPU inventory replenishment in the channel as PC units outgrew microprocessor units by over 10% during 2H10.

Raising estimates. They are raising their C11 revenue and EPS estimates from $48.3 billion and $1.74 to $54.7 billion and $2.35 due to higher revenue and margins. They are also raising their C12 revenue and EPS estimates from $49.5 billion and $1.81 to $59.0 billion and $2.32.

Upgrading to Overweight. JPM is upgrading INTC from Neutral to Overweight due to upside to Consensus as inventory has normalized at both Intel and the channel. They are raising their December 2011 price target from $20.50 to $25.00 or roughly 10.5X their new C11 EPS estimate of $2.35, in line with the historical multiple of its peer group such as IBM, HPQ and MSFT.

– Credit Suisse reits their Outperform & $28 target noting that consistent with their preview, and despite investor concerns, INTC significantly beat March Q and June Guide – Bears will argue overshipping, inventory and too much capex – and will also need to push out by yet another qtr the dreaded “miss” – They get the structural concerns: tablets, smartphones, ARM and power – They don’t get the underappreciation of ASP leverage in core PCs, developing market growth, corporate refresh, server, cloud, storage and routers. In addition, INTC’s manufacturing lead is growing, and manufacturing is a key point of differentiation relative to being successful in non-traditional markets. Firm still thinks this is at least a $30 stock, they hope it gets there before EPS goes to $3.00.

THE CAUTIOUS:

– Piper Jaffray notes Intel reported a strong Q1 and provided strong Q2 guidance. Q1 strength was driven by a quick recovery from its chipset flaw, Sandy Bridge channel fill, and an extra week. Backing out the extra week in Q1 and acquisitions, sequential organic revenue growth at the midpoint of guidance is up 7% vs. a more typical Q2 of flat to down 3%. They believe this growth is unsustainable and more a perturbation caused by chipset issues and double ordering. At a minimum, sell out of PCs is much weaker than Intel’s sell into the channel. Piper thinksk this drives a weak 2H:11, much like last year. While only one of several factors, Intel did acknowledge tablets were cannibalizing sales of PCs and they believe this impact will accelerate going forward. While they expect shares will be up today, they would not chase. Remain Neutral & $22.50 tgt.

Increase 2011 Capex to $10.2B from $9.0. Intel indicated it is positioning to accelerate the transition to 14nm by spending more now to turn its 14nm development fab into a high volume manufacturing site when the time comes. However, Intel may also be positioning to be Apple’s foundry at 22nm

– Goldman Sachs notes Intel returned $5 bn in cash to shareholders this quarter and is executing very well in servers. However, the firm sees significant cyclical risk given: 1) they believe Intel overshipped PC end demand by 12% in 1Q. As a result, they expect Intel’s revenues to correct relative to PC units over the course of the year. 2) Intel raised its 2011 capex guidance to $10.2 bn (+96% yoy). Five out of the last six times that Intel raised capex more than 25% yoy, gross margins were down nearly 800 bp the following year due to excess supply and higher depreciation. For example, in 2005 Intel raised capex 51% yoy. In 2006, MPU ASPs were down 14% yoy and Intel’s margins were down 825 bp despite 11% PC growth.

Goldman’s new $1.50 2012 EPS estimate is 31% below the Street. They are positive on Intel’s server business, which they believe will benefit from share gains as well as a higher-end mix. In addition, they believe Intel’s 3.6% dividend yield and buyback support a Neutral rating.

Notablecalls: While I expect INTC to trade up in the 21.25- 21.50 range in the veryn-t, I’m not overly confident there is much upside after that.

As the UBS analyst Uche Orji notes this morning, >50% of PC sales are now from emerging markets, making it inherently more difficult to track. That’s where the analysts got it at least partially wrong (he’s a bull, btw raising his target to $28.50 this morning, Reit Buy).

The other thing about emerging markets is that the whole Tablet craze hasn’t really arrived there yet. So there isn’t much PC cannibalization happening yet. But it will, it surely will.

Consensus ests for 2011 are moving up this morning but that may prove to be short-lived. So, buyer beware!

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply