I was chairing a pension board meeting for my denomination recently, when the representative from Morgan Stanley mentioned the positive change in the GDP figures. I winced, and said to myself, “Doesn’t sound right. How can the economy be doing well when energy and food are running up in price?”

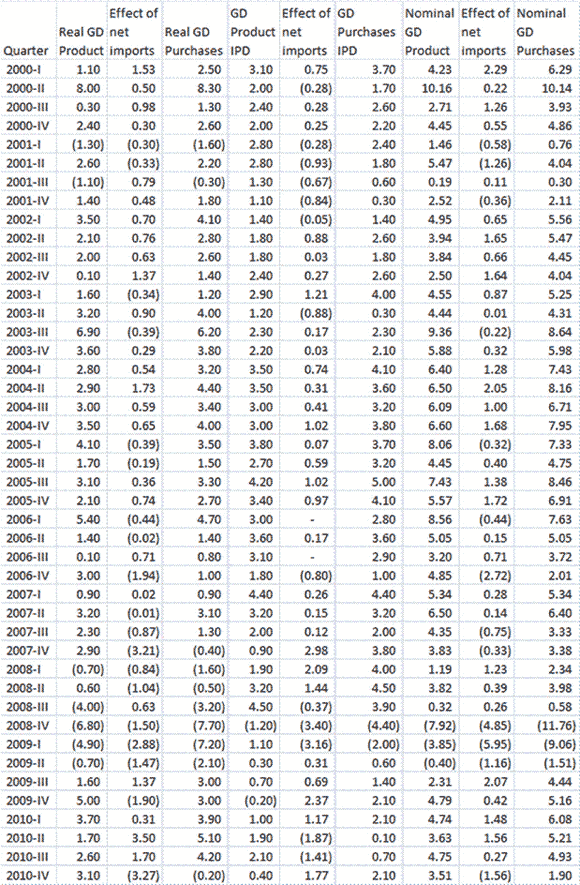

So, when I got home, I looked at the 4Q “Final” GDP figures. After a little while I realized that we are facing the same phenomenon as we did back in 2Q 2008, when I write the piece, Another Look at Preliminary Second Quarter GDP. Let’s start with the definition of Gross Domestic Purchases, which I think more closely tracks the way average Americans feel than Gross Domestic Product does.

Gross domestic purchases

The market value of goods and services purchased by U.S. residents, regardless of where those goods and services were produced. It is gross domestic product (GDP) minus net exports of goods and services. Equivalently, it is the sum of personal consumption expenditures (PCE), gross private domestic investment, and government consumption expenditures and gross investment.

Source: U.S. Bureau of Economic Analysis

Pretty simple — GDP minus net exports equals Gross Domestic Purchases. The trouble is that import price increases increase real GDP relative to real GD purchases.

Note well: IPD stands for implicit price deflator, which is a comprehensive measure of inflation. Also, figures may not add due to rounding, timing differences, and errors in revisions.

In 4Q 2010 real GDP rose 3.1%, while real Gross Domestic Purchases fell 0.2%. Why? Energy and other import costs rose which depressed the price indexes for GDP versus Gross Domestic Purchases.

Over the long haul, the two series are close to equal, but when they diverge, they tell a story. The current story is that average consumers in the US are doing badly, while those benefiting from high corporate profits, and increasing exports are doing well.

In general, I am not impressed with statistics collected by our government, or how they use them. But it’s useful to understand what they mean — to understand the limitations of the statistics, so that when naive/conniving politicians use them wrongly, one can see through the error.

Before I close for the evening, I’ll give one more example: the use of core CPI as a more reliable indicator of inflation than the unadjusted CPI. From first principles, I already know something is wrong here, because if you want a more stable estimate of central tendency than mean, one can use a trimmed mean (Dallas Fed), or a median (Cleveland Fed) — you don’t toss out a whole class of data inside your calculation simply because it is more volatile on average. and with respect to food and energy, yes, they are more volatile, but also over the last three, five, ten, and twenty years, inflation in food and energy has been higher than that of the core CPI. For those who want to paint the inflation picture as happy, it is more convenient to paint that picture using the core CPI, which is a bogus concept.

We could go on with other intellectual weaknesses of the CPI — substitution effects, owners equivalent rent and hedonics, none of which are theoretically wrong, but which are applied wrongly, and lead to an underestimate of inflation. If you have access to RealMoney, you can consult my article there. Also, statistics vary by income level — those that are poorer spend a greater proportion of their income on food and energy, making the concept of the core CPI even worse for those less-well-off. Or, as the guy shouted to William Dudley as Dudley misused the concept of hedonics — “I can’t eat an IPad!” Statistics, even if properly done, reflecting the average income, will not necessarily represent the median person, much less the lowest quartile.

Just be wary with statistics, and those who use them. Many have an axe to grind, including me, and will pick and choose their statistics at whim to suit their case. I try to be fair — these are gripes that I have developed with the statistics over the last decade — my tune has not changed here. They help to explain why goods and services price inflation has been restrained in the face of an exceedingly easy monetary policy. Or, look at the asset inflation engendered, which does not enter into the Fed’s inflation lexicon.

Be wary. Look at a broader range of statistics, and take apart the existing statistics. Don’t just take the pronouncements of our government at face value. They are experts in saying what is technically true, while implying what is false. Be wary.

Leave a Reply