On Changing Repo Haircuts

This week the Swiss National Bank announced publicly (FTalfaville link) that it has excluded Irish government bonds from being elligable as collateral for its repo operations. They did the same thing for sovereign bonds of Greece and Portugal. For the Swiss to start off the New Year with this offensive move is worthy of note. Did the Swiss slap their neighbors in the face?

SNB officials (with the assistance of both CNBC and WSJ) did their best to downplay the significance of these actions. From the Journal:

A spokesman for the SNB said, “Only securities that fulfill stringent requirements with regard to credit rating and liquidity are accepted as collateral by the National Bank.”

And that is correct. Generally speaking the SNB requires collateral with a AA- minus rating. The recent downgrades for Ireland, Portugal and Greece “necessitated” the actions by the SNB. This was “no big deal” as they were only following longstanding and pre-existing rules. I don’t buy that. From Risk.net:

The SNB states that “securities issued by sovereign countries and central banks can be exempted from this rating requirement“. A spokesperson for the SNB declined to comment on the specifics of the Irish case.

So the SNB didn’t have to do this, they chose to do it. That is a slap in the face that leaves a mark. In the scheme of things this is not a big deal. The repo market for peripheral sovereign bonds is still open. More a hiccup than an issue. But I am left wondering “why now?” At the SNB every action is taken after significant deliberation.

Bad Press for SNB

The Neu Zuricher Zeitung had an interesting article today. I consider the NZZ as the official organ of the SNB. The relationship is not unlike that which exists between the WSJ and the Fed. An article that is critical of the SNB is rare, and noteworthy.

The concentration risk of the SNB

High loss in 2010 eats dividend reservesThe exchange rate losses of the Swiss National Bank on their foreign currencies for 2010 should amount to around 30 billion francs. In politics, the foreign exchange purchases by the central bank will be extremely controversial.

30b CHF is a big deal to the SNB. As the article discusses, there are already political (and economic) issues that are arising as a result of SNB reserve management policy mistakes. The SNB has recently referred to the decision to acquire tens of billions of Euros in an effort weaken the Franc as, “with the benefit of hindsight….” In other words, they have acknowledged that they have erred.

The forgoing reconfirms an important point. The Swiss National Bank is out of the market. We are entering new uncharted waters on the CHF crosses. And the captains of the ship can’t use the steering wheel.

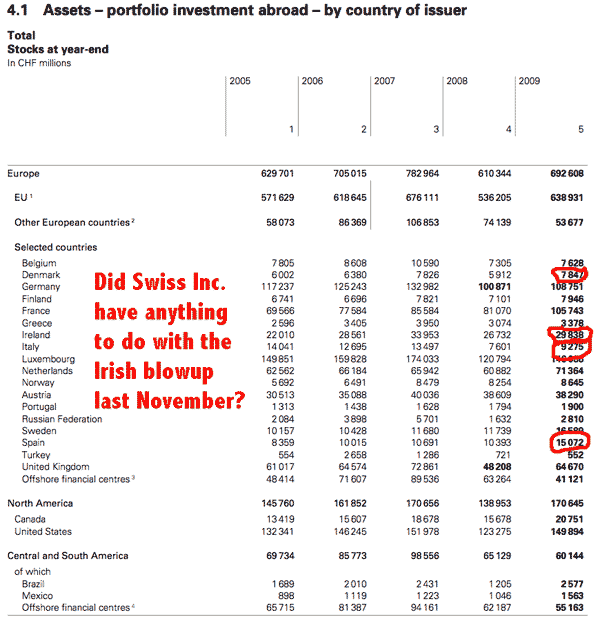

Switzerland attacks Ireland?

The following is a look at Swiss financial institutions portfolio holdings from a year ago. The one number that looks large to me in comparison is Ireland. Irish holdings are 3X’s that of nearby Italy. Surprising. 2X’s that of Spain. (Spain’s economy is seven times larger than that of Ireland). Norway’s economy is twice that of Ireland yet the Swiss held 4X’s as much paper. You get the picture.

The actual SNB announcement of the changes of Repo haircuts for Ireland was back on 12/21. The question I’m wondering about is when did all of those Swiss institutions that were holding these big slugs of Irish paper first hear about the upcoming changes in the Repo regs? Was it a day before? A week? A month?

I think the answer is at least a month. The SNB would give the big hometown institutions a heads up so that they could prepare in advance for the coming changes. What does that mean in real terms? That means that Swiss Inc. lightened its books on Irish exposure during the month of November.

Of course it was November that broke the back of the Irish bond market and forced a $120 billion bailout. Call me an old cynic. But I never, ever believe in coincidences. These dots are connected.

apparently on a posterior note the Swiss bank claimed it never accepted Portuguese bonds due to a previous settlement, so the news is a bit of a farse, at least in what relates to Portugal

http://online.wsj.com/article/BT-CO-20110107-709183.html

this is the news item