During the past several years I’ve repeatedly insisted that the huge increase in the monetary base of 2008 would not produce high inflation. I suppose I was naive in thinking that when it became clear that excessively low inflation was the real problem, the inflation hawks would admit they were wrong and re-evaluate their models. I don’t see much evidence of that happening.

One recent theme has been the supposedly unreliability of the core inflation rate, which is now below 1%. Critics (and cartoon bunnies) point to the fact that food and energy are an important part of the average American’s budget. When it’s noted that even headline inflation is barely over 1%, the attention turns to other prices. For instance, Congressman Ryan has recently argued that the Fed should focus on commodity prices. My initial reaction is to say “Yes! Let’s focus on commodity prices! Commodity prices are the best way to tell if money is too easy or too tight.” Think I’m being sarcastic? Then you are in for a surprise.

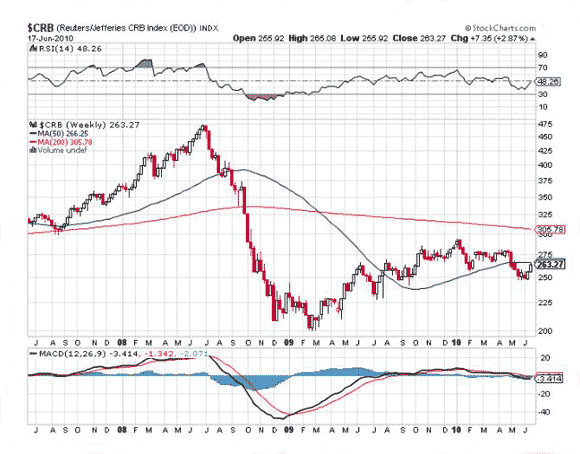

Before continuing, I’d like to remind readers that in late 2008 you could count on one hand the number of economists (in the entire world) claiming monetary policy was very tight. So let’s take a look at the change in commodity prices in late 2008:

That’s right, commodity price indices fell by more than 50%. That’s Great Depression-style deflation. And where was Congressman Ryan when the Fed was engineering one of the greatest deflations in world history? I don’t recall him or any of the other inflation hawks calling for easier money. But maybe I missed something. If so, I hope my readers will dig up all the stories of conservatives demanding easier money in the fall of 2008. In any case, it’s good to know that whereas back in late 2008 I was almost all alone in viewing money as being extremely tight, I now have the vast right wing conspiracy on my side. Money really was tight in late 2008. And if commodity prices are now the preferred metric of the right, then I’m half way to convincing the economics establishment that I was right all along. Now I just have to convince the left that money was way too tight in 2008. About those near-zero interest rates . . .

BTW, I don’t mean to bash Congressman Ryan, who is from my home state and is one of the best of a bad lot. If all 435 Congressmen and women were like him we’d probably end up with a much more economically sensible tax and spending regime. But I have to say that the conservative movement has recently been grasping for straws on monetary policy. All their predictions are coming in false, and they aren’t drawing the appropriate conclusions.

Leave a Reply