Stocks are down sharply this morning with the /ES just beneath but still close to the 935 pivot.

The next lower pivot is at 912 and the next higher is at 961. 955ish has capped the rally, yet support has moved up into the 925 area. A break beneath 912 would be required to start thinking about a trend change and that’s a distinct possibility as we are right in the middle of a Fibonacci turn window that began on June 9th and ends on June 17th.

I think it’s very significant that the Transports got close but refused to make a new minor high yesterday. There is a DOW Theory non-confirmation in place in that the DOW has been making new short term highs but the Transports have not. Those types of non-confirmations can definitely mark tops, so keep an eye on that.

Bonds are up slightly, remember that the long bond has reached long term support where I have mentioned that some basing action is likely. What happens in bonds over the next month or so will be important.

The dollar is up strongly overnight sending gold and other commodities down.

One of the reasons the dollar rose is that European Industrial Production PLUNGED by a record 21.6% year-over-year in April, much greater than forecast.

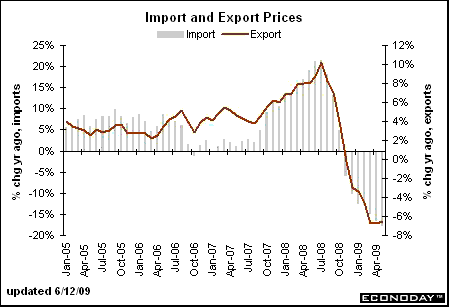

Data was also released this morning on import and export prices. The month over month numbers for May showed slight increases, but the year-over-year data showed that export prices DECLINED by 6.5% versus -6.8% last month, a slight uptick, but still a very sharp decline.

It is IMPORT prices that shows the greatest decline with yoy import prices DOWN 17.6%, which is much greater than last month’s -16.3%!! In other words price declines of imports is accelerating even with the global rally and positive seasonal influences. Minus 17.6%?! Yowzzaa! Sorry to those looking for signs of inflation in that data, you will not see it there.

Of course leave it to the media to spin inflation into those numbers!!! Oh yeah, gasoline went up on speculation… Here’s what Econoday has to say – sure wish I could find some realistic reporting! Oh yeah, that would mean there would be no need for this blog!

Import price data for May show early hints of inflation. Especially important are prices for non-petroleum imports which rose 0.2 percent to end a long string of declines. Pressure is appearing in ex-petroleum industrial supplies and, for a second month, in foods. Commodity prices have been on the rise in large part due to inflation hedging spurred by expectations of dollar-based inflation. Such expectations have also been a big factor behind the jump underway in crude oil, which in this report shows a long series of increases for petroleum imports including an 8.3 percent rise in May.

Overall rates show a 1.3 percent rise for imports following a 1.1 percent rise in April. Export prices also show pressure, up 0.6 percent in May on top of a 0.4 percent rise in April. Here again, commodity price pressures are to blame, this time in agricultural export prices which jumped 3.6 percent following a 3.7 percent rise in April.

A deflationary recession was the prior concern for policy makers which however, due to their stimulus efforts, may now switch over to the risk of an inflationary recession. Today’s report will raise concerns over next week’s much more closely watched producer and consumer price reports.

To whoever wrote that – DUDE, Import prices fell 17.6% year over year and it was a greater rate of fall than last month!! That is a HISTORIC collapse of prices!!! Stop with the damn “signs of inflation” already and wake the heck up!!!

Whew! The Economic Mass Psychosis is certainly a powerful thing to overcome.

Speaking of Mass Psychosis, the Consumer Sentiment readings come out a 9:55 Eastern.

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply